The Momentum Rank

One of the most remarkable truths in stock markets is that prices have a tendency to trend in the same direction. Indeed buying recent winners and selling losers is one of the most profitable habits that an investor can have. This 'momentum' is evident not only in share prices but also in company earnings.

When companies surprise to the upside in their earnings announcements, the share price tends to react similarly. The Stockopedia Momentum Rank blends several metrics that define share price momentum with several metrics that define earnings momentum to help you find the companies most likely to continue to outperform over a 3 to 6 month period.

How does Stockopedia calculate the Momentum Rank?

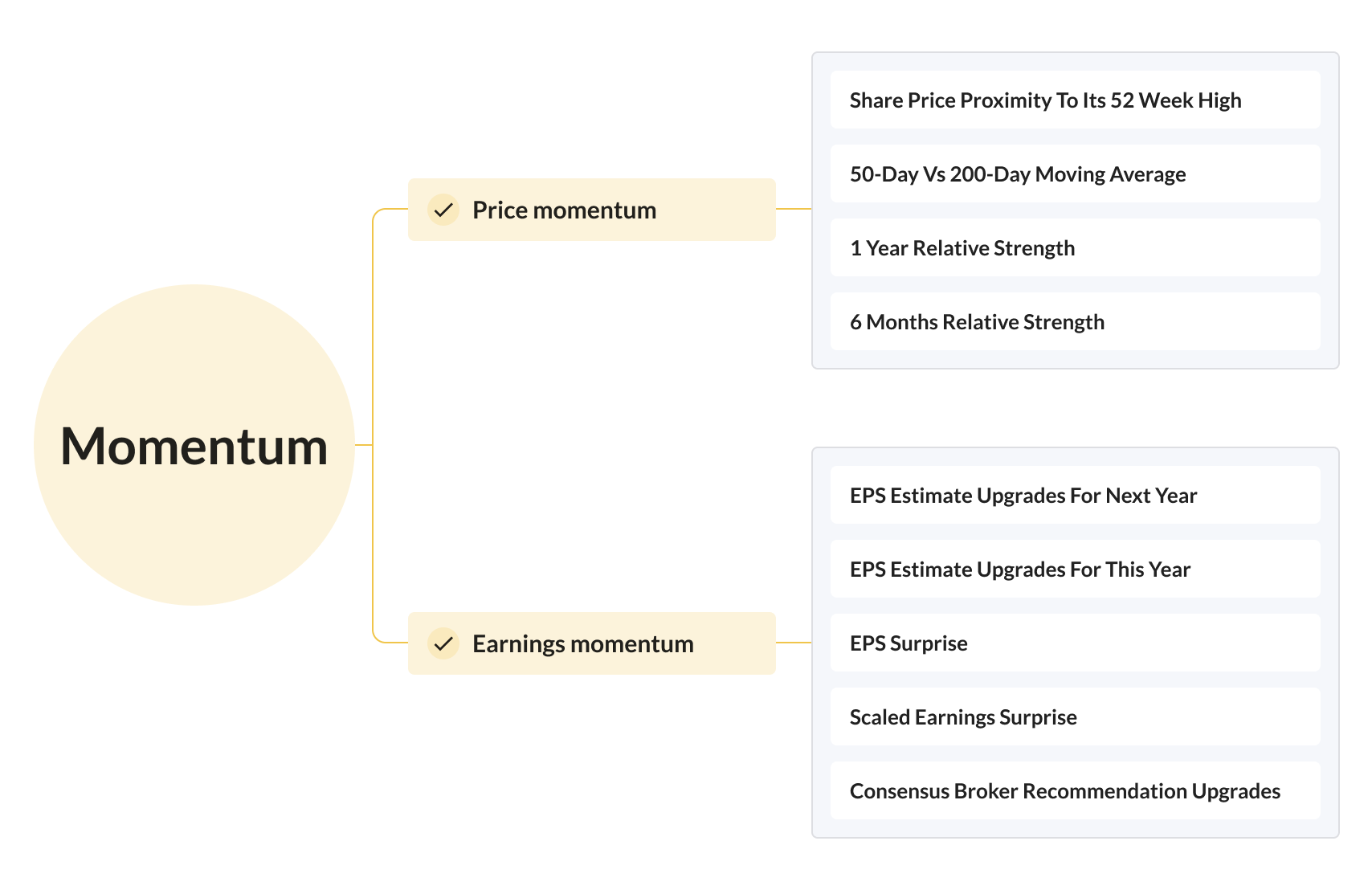

Our MomentumRank is inspired by the latest research into momentum (Jegadeesh and Titman, George and Hwang, Seung-Chan Park)and is based on a composite of the following Price and Estimate Momentum Factors:

Each company in the market is ranked from 1 to 100 for each of these momentum ratios and a composite score is calculated as a weighted average of all valid values. The MomentumRank™ is then calculated between zero and 100 for this composite score, where 100 is best and zero is worst.

NB - when a company has no broker coverage we cannot calculate earnings momentum. In these cases, the Momentum Rank is calculated using price momentum factors alone.

The momentum research suggests that relative strength is a negative signal in the very near-term (less than 1 month) and the very long-term (3 yrs +) but generally a positive indicator in the medium-term (3-12 months) - we focus on medium to long term factors in this momentum rank.

Work by US finance professor Seung-Chan Park in 2005 found that it was possible to predict the medium-term outperformance of a stock based on the ratio between its 50-day and 200-day MA. His research showed that stocks where the 50-day MA is much higher than the 200-day MA tend to perform better over the subsequent six months than stocks whose 50-day MA is much lower than the 200-day MA. He finds that a long/short momentum strategy sorted based on the 50 day / 200 day moving average ratio generates raw returns of 1.45% per month (1.81% for the top decile and 0.36% for the bottom decline), increasing to 1.64% when risk adjusted.

Work by researchers George and Hwang published in the Journal of Finance has shown that the closer a stock's current price is to its 52-week high, the stronger that stock's performance in the subsequent period. They surmise that investors use the 52- week high as an "anchor" against which they value stocks, thus they tend to be reluctant to buy a stock as it nears this point regardless of new positive information. As a result, investors under-react when stock prices approach the 52-week high, and consequently, contrary to most investors' expectations, stocks near their 52-week highs tend to be systematically undervalued. Academic research by De Bondt and Thaler illustrates that 3 year losers have a tendency to outperform 3y winners. This is the concept of mean reversion at work.

Performance of the Momentum Rank

As for the previous Quality and Value Ranks we have used annually rebalanced portfolios of UK stocks above £10m market capitalisation since April 2013 to create the performance chart below. It shows the great outperformance of strong 80+ ranked momentum stocks throughout this period of market history, and the underperformance of weak stocks.

Guide to using the Momentum Rank

The Momentum Rank has been the most powerful of all the basic StockRank components to date - outperforming in almost all major markets. It's worth reiterating that while the returns to value can take longer time periods to accrue (often over 3 years), the momentum effect is best captured over shorter time periods (3 to 12 months). Some of the best recent books about momentum strategies (by authors like Mark Minervini and Bill O'Neill) focus on these shorter time periods.

There are of course some risks to trading momentum. Daniel & Moskowitz in their paper Momentum Crashes[1] detailed the dark side of the momentum upside - that the strategy can have some very 'bad times'. While momentum is the most powerful of all the factors, it has the worst periods of underperformance.

These momentum crashes tend to happen at the bottom of bear markets, especially in long/short strategies (where you buy the winners, but simultaneously short the losers).

In these market periods, when there have been big declines, it's the recent loser stocks that tend to bounce back extremely quickly. One of the ways to avoid momentum crashes is not to short stocks, and stay on the long side of the trade.

The 'highest momentum' stocks by standard measures in these crashes will, by definition, be those that have declined the least - i.e. the safe, low risk, quality stocks. Ironically, those shares have the least ability to outperform strongly in a fast recovery, as they often have barely declined. This leads to another rule of thumb - don't buy the highest momentum stocks after big stock market declines. It's often a much better bet to buy the beaten down, deep value stocks at those moments !