Free Cashflow - the ability to self-finance growth

In this article, we’re going to dive deep into cashflow - which is the fuel that ensures a company can self finance most of its growth. It’s a key component of the very best performing shares.

Understanding profits and cashflow

Let’s return to our basic company diagram introduced in the second article of the series.

Capital creates sales, creates profits, but what about cash flow? Not all profits are created equal. There's a saying that sales are vanity, profit is sanity, and cash is king (or cash flow is king). To find genuinely self-financing businesses, you need to look for profits that are converted into Free Cashflow. Now, what do we mean by that?

Well, If you haven't studied much accounting, I can understand that this can be a difficult concept. It’s understandable to assume that if a company is profitable, it's self-funding. Well, actually, companies can use aggressive accounting policies to inflate profits before they have actually received the cash.

How companies can inflate profits through aggressive accounting

They can do that by methods like recognising sales earlier than they receive the cash. Imagine you were considering subscribing to Stockopedia.com, but didn’t want to pay yet. Well I could sell you a subscription and ask you to pay in a year. From an accounting perspective, that would be registered immediately as a sale, and thus inflate the accounting profits today, but it won't actually do the business any good because the cash flow hasn’t been received.

Here’s a few aggressive accounting approaches that companies can take to inflate profits.

They may inflate their sales numbers by selling on generous credit terms, as in the example described.

They can also delay booking expenses which also inflates profits. For example, they might capitalise their R&D instead of booking as an expense. In reality, they have actually already paid out that cash. There’s often a lot of disagreement about what should be capitalised on the balance sheet and what should be booked as an expense. So it’s important to be wary here. A lot of R&D has to be written off!

You also find that companies often treat some expenses as “extraordinary” which may be accounted for in a way that obscures the true profit/loss of the business.

Compiling “Free Cashflow” from a cashflow statement

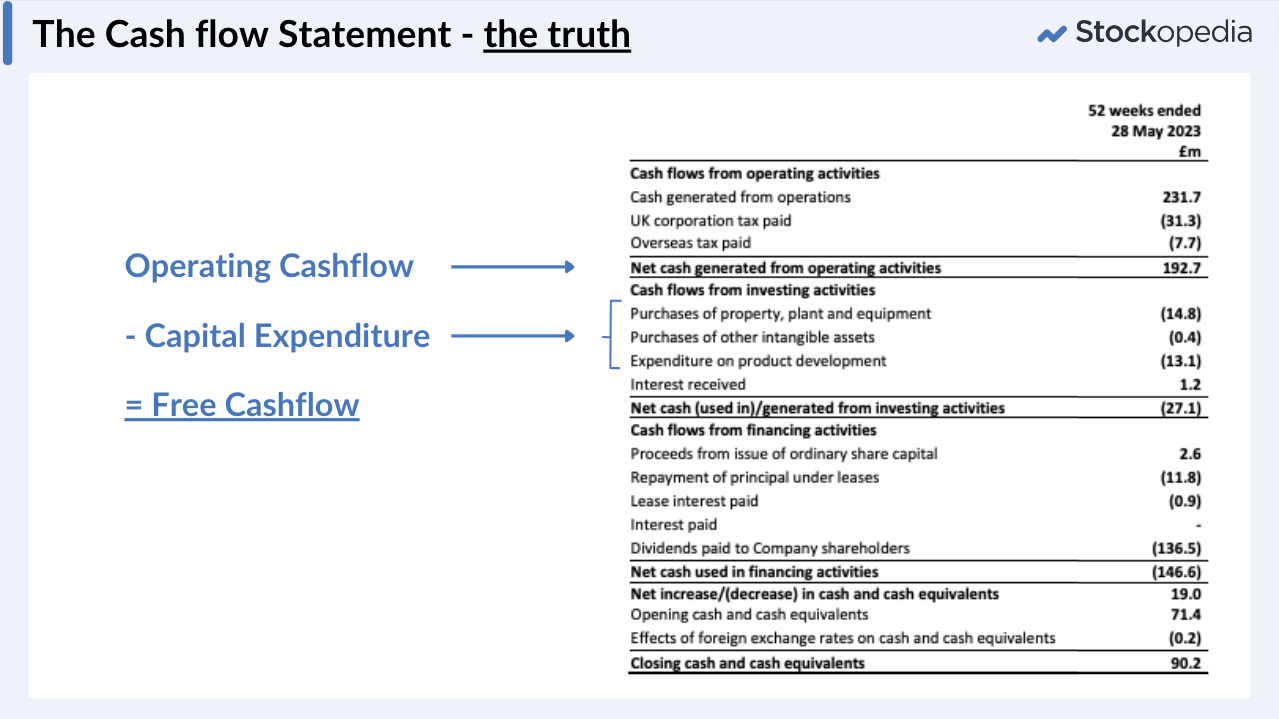

Now don't be overwhelmed by this, but here’s a quick screenshot of a real cash flow statement. The cashflow statement tells you the truth behind the cash situation in a business and it’s often far more important than the Income Statement (previously known as the Profit and Loss Account).

The Cashflow statement is split into three parts for every business.

Cash flows from operating activities

Cash flows from investing activities

Cash flows from financing activities.

It’s important to understand that you should start with the operating cash flow (Net Cash generated from Operating Activities), which is the cash generated by the business’s operations. But companies often have to use that cash to invest in what's called Capital Expenditures (“Capex”). They need to do this to invest back into their businesses for maintaining property and equipment, investing in new products and buying assets that might actually be needed in the business.

That capex needs subtracted from operating cash flow to give an indication of the Free Cashflow to the firm. This free cash flow can be used in lots of different ways. It can be used to pay dividends, to pay down debt, to fund acquisitions (all financing cashflow matters) - or be reinvested back into the business operation.

Reviewing free cashflow using StockReports

At Stockopedia we make this analysis easy in the financial summary of StockReports.

Firstly, the earnings per share is shown over the previous six years (profit and earnings are inter interchangeable terms), and you can see how this progresses over time. So for Games Workshop (GAW) this was growing nicely and steadily.

We then show the operating cash flow share, which was also growing nice and steadily for GAW, and fairly comparable versus the earnings. This suggests strong cashflow conversion. You want to see a good conversion of earnings into operating cash flow as that cash can be used in the business.

Then you see CapEx per share (capital expenditures) which was fairly moderate for GAW. A very high CapEx business often will have a very volatile Return on Capital. They can regularly dip into losses and often need a lot of debt to keep operating. So keep an eye on that.

If you subtract the capex from the operating cash flow you calculate the free cash flow per share. This very, very high throughout most of the period for GAW. So it was a company that spat off a lot of cash flow. That's very, very beneficial for shareholders.

Warren Buffett loves to see businesses that spit off cash flow because there's so much they can do with it in the business, but also they have the option to pay it out to Buffett so he can invest in other profitable businesses that need the investment.

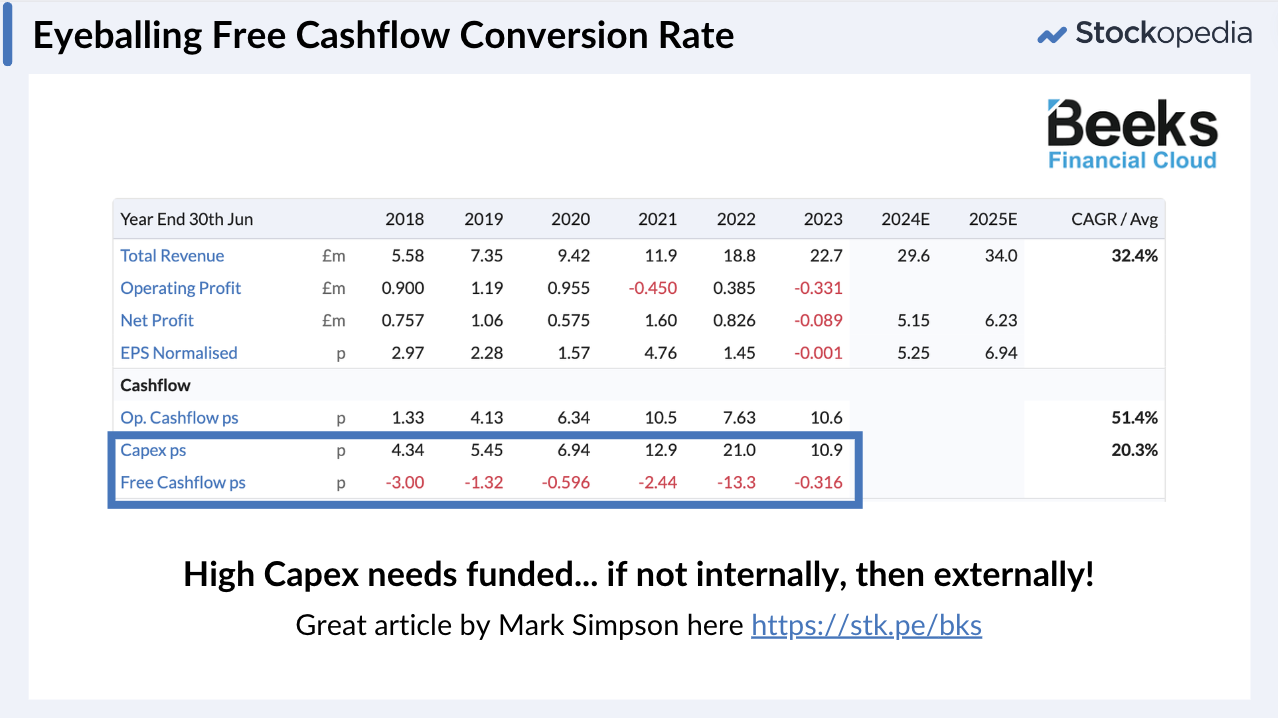

Another case study - Beeks Financial Cloud

Here's an example of another business that's investing heavily in the future called Beeks Financial Cloud, which has been increasing its revenues quite strongly. But as you can see, operating profits have been a bit more patchy, and so have the earnings per share.

It is indeed generating operating cash flow per share, but the CapEx is really high. That made the free cash flow per share very negative. If it's not generating free cash flow internally, then the capex likely needs funded. That likely means it needs funded by external sources, shareholders putting more money into the business, or through debt. This can really increase risk.

Acquisitive businesses and free cashflow

Businesses that serially acquire other businesses need some subtle treatment here. We found there were a few acquisitive businesses in our study of the Top Ten Multibaggers. Judges Scientific (JDG) was one such business. It grew by very carefully acquiring businesses at very earnings enhancing rates.

But when you're looking at free cash flow to the firm, if you’ve only subtracted CapEx like we do on the StockReports, you may not see the full impact of the acquisition spending on the resulting cashflow. JDG used some of that free cash flow to actually acquire other businesses. These investments are shown in the cashflow statements, so it’s always worth referring to the accounts.

In the chart below on the left, blue is the free cash flow, but in red is free cashflow after acquisition expense. When the red line is significantly below the blue, it’s likely been making acquisitions.

In the 2022 period, there was a large acquisition made, which created a large outflow to pay for the acquisition, reducing the cash balance. In the chart on the right you can also see a very significant increase in the debt burden. It paid for the acquisition with debt.

Now this business has very good management, and they've got a proven track record of exceptional capital allocation, but it's something that is one should be aware of and investigate. If the debt is going up, it does increase the risk. And if the cash is going down, well, you have to think about the implications.

Summary

So just to wrap up this section.

Potential multibagger ideally have good conversion of profits into free cash flow. Cash is king. This minimises the need for external finance - avoiding debt and dilution. Businesses that spit off cash flow have less need for debt.

Multibaggers also have moderate requirements for capital expenditure, capital light businesses are preferable. Be wary of very, very heavy CapEx businesses because they can actually sometimes get into trouble.

In the next article we’re going to investigate the extraordinary power of “Multiple Expansion” on share prices. Don’t miss it.