Four reasons why private investors have an edge over professional fund managers

Can we ever outperform the pros? In order to answer this question, we need to define where our edge is.

Firstly, let’s take a look what we are up against. Our competitor investment management company has an army of analysts, each highly qualified with an MBA, PhD and several investing qualifications. They are able to assign individuals not to look at a whole market, but investigate businesses within an industry or in some cases just a handful of companies that the analyst will eventually get to know better than their CEOs. All of these ideas are pitched to the fund manager who then decides, with help from their 6-figure-per-year risk system, how to construct the portfolio.

The scale advantages may seem overwhelming, but there are several disadvantages that the institutional investor must contend with. It is in these disadvantages that the private investor can seek their edge.

The first is liquidity.

Investor Edge 1 - Liquidity

“It’s a huge structural advantage not to have a lot of money. I think I could make you 50% a year on $1 million. No, I know I could. I guarantee that.” - Warren Buffett

“If I were working with a very small sum – you all should hope this doesn’t happen – I’d be doing almost entirely different things than I do. Your universe expands – there are thousands of times as many options if you’re investing $10,000 rather than $100 billion, other than buying entire businesses. You can earn very high returns with very small amounts of money.” - Warren Buffett

The average equity fund manager has around £650m in assets. This means that if they want to allocate 4% of their fund in a stock, there needs to be sufficient liquidity for a £26m inflow. This makes a large, less liquid part of the universe uninvestable for multiple reasons. Firstly, for some stocks a sizeable inflow could result in the fund manager owning a sizeable percentage of the company stock. Due to the takeover code, owning more than 30% of the shares in issue may require a mandated offer for the whole company.

Even a 3% ownership of a company adds the extra regulatory burden of a notification of the acquisition or disposal of major shareholdings. Fund managers are therefore often restricted in their investment mandate regarding percentage ownership of a company. When combined with the necessary large transaction sizes, this limits the investment universe due to an inability to purchase a sufficient holding size to have an impact on portfolio performance.

The large position size in monetary terms also adds further complications. When entering into a position it is likely that the high volume of shares required will negatively impact the price of the desired shares, resulting in a higher price for purchases. This is known as market impact. Upon exiting a position, the high volume of shares will again negatively impact the price of the desired shares, resulting in a lower price for sales. The severity of this impact means that they risk being a forced holder of shares due to a reduced ability to exit, a forced buy and hold.

In order to prevent this predicament, funds will have liquidity constraints meaning they cannot go into a stock if doing so would take up a large percentage of average daily volume. The means even moderately liquid shares are out of scope for large funds. Given the drive of portfolio risk teams to test liquidity of the portfolio in stressed conditions (such as liquidity conditions in the Financial Crisis), this further reduces the investable universe.

With smaller trade sizes, the individual investor has a considerably wider investment universe available to them and is not restricted by limited liquidity. Individuals enter and exit positions in smaller quantities and as such have lower impact on the price of the shares. We can be more dynamic to change and do not need to be locked into our investments - allowing us to run our winners and promptly sell our losers.

Investor Edge 2 - More Control of Mandate and Portfolio Construction

“Control your own destiny or someone else will.” - Jack Welch

When a fund is created, it must complete and submit a prospectus which provides details on the legal and self imposed constraints that it will work within. Further to this, the fund will also have further internal constraints. These will typically include:

Position sizing, determining the maximum and minimum percentage of assets that the fund manager can make to a single stock

Aggregate allocation to certain vehicle structures and cash

Aggregate sector allocation in absolute terms or deviation from the benchmark allocation

Aggregate tracking error restrictions from the benchmark

There are also further constraints based on the structure of the fund. Many fund houses will try and structure their funds compliant with UCITS, which means they can then be passported across the European Union. This widens the potential pool of investors and opens the fund up to other institutions which only invest in these vehicles. However, structuring a fund in this way adds additional constraints in portfolio construction, particularly around position sizing. Funds compliant with UCITS may have a maximum of 5% of the fund that can be invested in a stock, no matter the fund manager’s conviction. If the stock does continue to perform well the position must be continually reduced, forcing the fund manager to cut their winners, rather than letting them run.

There are also further external pressures concerning the style of the fund manager. If the fund is marketed as a certain style, such as a value fund, then it is frowned upon for the manager to invest in a non-value stock, even if they believe that it is an attractive opportunity. There is a lot of pressure for the manager to avoid style drift even if the current investment environment is unfavourable to that style. These restrictions can be justified as we (the investor) would want the fund to stay true to its style. However it does add another layer of constraints for the universe the manager can invest in.

The private investor has considerably more flexibility in their allocation rules and construction of their portfolio. We are not constrained by a certain style and can choose what we believe to be the most attractive opportunities, no matter the style, sector or benchmark weight. We can choose to be concentrated in our best ideas or build a more diversified portfolio in line with our conviction. Finally, we can use cash or other assets as an alternative to dampen volatility of the portfolio in line with our risk tolerance and view of market conditions. By contrast, the fund manager will often be forced to take a diluted approach to investment risk control via sector allocation (like allocating more to defensives in stressed markets).

Investor Edge 3 - Longer Time Horizon

“If everything you do needs to work on a three-year time horizon, then you’re competing against a lot of people. But if you’re willing to invest on a seven-year time horizon, you’re now competing against a fraction of those people… Just by lengthening the time horizon, you can engage in endeavors that you could never otherwise pursue” - Jeff Bezos

For an industry that stresses the importance of thinking long term, some may be surprised to learn how much focus is placed on short term fund performance. Fund management is a very competitive industry and each period of performance is scrutinised both internally by management and risk teams and externally by media and competitors. Often a long steady record of performance can be discounted by “yeah, but how have you performed year to date?”

This is also compounded by the industry’s trait of focusing on rolling periods to evaluate performance. This is again a rational response given that one cannot buy past performance, however it does make assets with certain return payoffs hard to hold for a professional fund manager.

Suppose that you have an asset that has a negative cost of carry (either in absolute or relative to a peer group/benchmark), but on occasion generates a large positive performance.

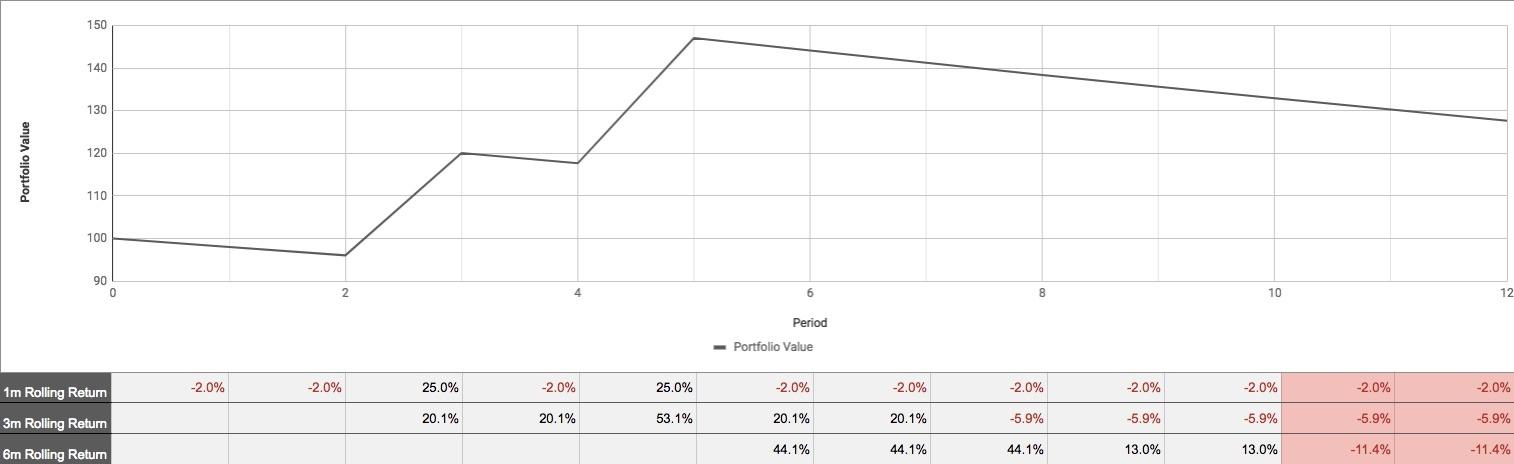

For illustration, one of the many possible portfolio performance returns is provided below. In this simplified example, there is a 20% chance of a 25% (relative) return in a period and a 80% chance of -2% (relative) return, resulting in a positive expected (relative) return of 3%. This is an asset with positive expected return and a positive skew.

We can see that although the performance over the whole period is attractive had you owned the portfolio since inception, on a rolling basis it appears to be less attractive and the small periods of success are quickly ‘forgotten’ or could quite easily be determined as ‘unrepeatable’ from an outside view.

Unlike individuals, who are by definition invested since inception and get to keep all their performance, the lumpy periods of returns have a tendency in the industry to be quickly discounted by the longer period of negative performance. To ensure fund managers provide a return payoff that is attractive for investment, it is preferred to generate a smoother performance profile rather than a lumpy returns, even if a lumpy profile may generate more returns over the longer term.

As Jeff Bezos wisely noted above, a simple way to gain an edge over a fund manager is to give yourself a longer term horizon. The competitive pressure of the industry means that a large number of fund managers are unable to focus on the long term, despite knowing its importance.

This neatly links to the biggest advantage the individual has over the fund manager, a lack of career risk.

Investor Edge 4 - Lack of Career Risk

“Worldly wisdom teaches that it is better for reputation to fail conventionally than to succeed unconventionally.” - John Maynard Keynes

In the film ‘The Big Short’, we hear the story of Michael Burry, the fund manager at Scion Capital who is early to identify the instability of the US housing market. He uses collateralised debt obligations to bet against the housing market, which requires a monthly premium to be paid, creating a burden to the performance of the fund whilst waiting for the housing market to crash. It is in this period that we get an insight into the pressure that Michael is put under by his investors as the losses continue to grow, with many demanding to withdraw from the fund. Michael is subsequently proven to be correct, earning 489% for investors, but was impacted by the experience: “disheartened on many fronts, I shut down Scion Capital in 2008”.

The typical fund manager won’t be making $1bn bets against the housing market, but investors should not underestimate the large impact career risk can have on fund manager positioning. Even if a fund is described as benchmark agnostic the pressures of performing against the relevant index are still apparent. Internally, fund managers are constantly pressured on losing positions and externally prolonged periods of relative underperformance are often punished with asset outflows.

A survey by CFA Institute[1] asked how long investment teams could underperform at their firms before they should start to worry about their jobs and the results were startling:

“Of the 774 respondents, 78% said that career risk due to underperformance is a factor at their firms, and the largest number (28%) said that between one to two years was the time period when job security would start to be an issue. Another 13% said that in even less than one year the investment team should be concerned. In other words, 41% said investment teams have less than two years to turn around underperformance or it may be time to dust off the resume.”

Joachim Klement’s paper [2]demonstrates how even a potentially successful investment strategy may not be one that can be maintained by a fund manager due to the career risk effect.

If a fund manager has an annual alpha of 2.5% and a tracking error to the comparison benchmark of 5% (an impressive Information Ratio of 0.5), then, Klement points out, the manager will have a:

31% probability of underperforming in a given year

40% probability of underperforming in a given quarter

44% probability of underperforming in a given month

Given that a period of underperformance may result in the fund manager losing assets (or being fired) then there is an incentive to reduce deviation of returns from the benchmark. The term closet indexer is often used to describe when this is taken to the logical extreme. As fund managers are rarely punished for offering benchmark-like returns, then it makes sense to ensure that tracking error is low. This comes at the expense of leaving potentially attractive investment options on the table.

As private investors, we are afforded the luxury of being able to be truly agnostic to our return versus a benchmark, without fear of sudden outflows. Provided we maintain a good investment discipline, we can choose to holds positions that may underperform the benchmark in the short term if we believe the longer term prospects are strong, without being pressured by internal or external forces.

Am I wasting my time? - the intangibles

Throughout this piece I have been focussing on tangible reasons for adopting a personalised approach, however there are other softer yet no less key aspects to this question.

An investor must consider if they gain any enjoyment or utility from managing their portfolio. If one does not, then a suitable alternative may be outsourcing portfolio management to an external fund. On the flip side, many of our community will agree that they like the intellectual challenge of the markets and derive utility from seeing the impact of their decisions on their investment performance and ultimately their lifestyle.

The knowledge and skills developed can compound up over time, allowing you to improve future investment performance and pass on your knowledge to future generations. As Benjamin Franklin noted "an investment in knowledge pays the best interest."

Conclusion

Managing your own portfolio isn’t for everyone. With the plethora of passive options that are widely available, investors can now very easily achieve satisfactory market-like returns. However, the fact you are on Stockopedia implies that you, like myself and the rest of the Stockopedia community, believe it is possible to attain excess returns and are eager to do so.

With more information available than ever before and transaction costs trending down, there has never been a better time to be an investor. If we choose to adopt a personally managed approach, we should seek to continually improve our investment knowledge and ensure that our processes incorporate our advantages as private investors.

What other key edges do you think individual investors have over institutions and how have you adopted this into your approach?