The average individual investor holds quite a lot of cash. The American Association of Individual Investors (AAII) Asset Allocation Survey puts the average at 23% for US-based investors over the last 30 years. Since the UK markets have not been as strong as the US recently, the average UK investor has likely been even more cautious.

The rules of investment funds mean that many fund managers cannot hold significant cash balances. The average equity fund holds just 3.5% in cash. This should put them at a disadvantage to the individual investor who can be more flexible with their holdings. The problem is that equities have significantly outperformed interest on cash, or short-term government bonds over the long term. Investment writer Cullen Roche argues that this is one of the main reasons individual investors underperform their professional equivalents. Individual investors’ flexibility actually costs them returns because they tend to hold more of a poorly performing asset.

Why do individual investors hold so much cash?

When investors are asked why they hold cash, it is usually to take advantage of market weakness. Investors feel clever when the market sells off, and they are holding a lot of cash, and dumb when they are fully invested. Investment strategist Samuel Lee suggests that investors hold so much cash due to worry. He says:

"In my experience, investors sitting on a lot of cash are usually worried about equity valuations or the economy, and tell themselves and others that they are going to buy gobs of stock after a crash. The strategy sounds prudent and has common sense appeal – everyone knows that one should be fearful when others are greedy, greedy when others are fearful."[1]

The problem with this idea is that the average individual investor is terrible at being fearful when others are greedy, and greedy when others are fearful. To see this, you only have to look at the difference between the average returns of stock market funds and the weighted average returns of investors in those funds. These sound like the same concept but are subtly different: the first is the return if all investors had simply bought and held the fund, and the latter is the return when you take into account trading in and out of the fund by investors. On average, investors’ attempts at timing cost them 0.81% per year in lost returns. It doesn’t sound much, but it compounds to a 26% underperformance over a 30-year investment timeframe.

The situation is likely to be even worse in more volatile investment funds. For example, consider the investors in the CGM Focus Fund run by Ken Heebner. According to Morningstar, Heebner was the best-performing fund manager for the decade ending 2009, delivering an 18% compound annual return during this time. However, the average investor in the fund generated an 11% compound annual loss during the same period. They created this massive 29% annual underperformance for themselves by buying into the fund after it had posted strong returns and bailing after it suffered losses.

A more recent example is that of the ARK Innovation Fund. This took off in March 2020 and had almost trebled by the end of that year. However, the largest fund flows occurred in the months around the peak price in February 2021, when these phenomenal short-term returns were hitting the headlines. A year later, the fund had given back much of its gains but was still up around 50% from pre-COVID levels. The money-weighted return at that point was around -50%, meaning that the average investor had lost half their money through poor market timing in an asset that had gained 50%.

With these examples in mind, it is tempting to think that investors would be better off by being fully invested at all times. That may well be true, on average. However, there is no one-size-fits-all solution. Investors should have different levels of cash holdings depending on their unique strategy and circumstances. There are some good reasons for holding more cash and some bad.

Good reasons for holding more cash

Too few investment ideas

If an investor is struggling to find enough investment ideas and stay within their conservatively set portfolio limits, this can be a good reason for holding cash. It is better to hold cash than be overly concentrated in a few stocks and hence run the risk that unexpected bad news leads to significant portfolio losses. In addition, a shortage of ideas often means that a strategy or the general markets have become overvalued or overbought. In this case, holding cash may give an opportunity to invest at better prices in the medium term. These times should be relatively rare, though.

Needing to react quickly to opportunities

Some strategies require rapid reactions and cash on hand to execute effectively. For example, if an investor engages in opening auctions by entering orders on the order book, they may get good price execution. However, they must have the cash on hand to execute a buy order. Investors who are less reliant on rapid execution or trading on the order book can afford to be more fully invested. If an opportunity presents itself during market hours, they can sell their least-best idea to fund any purchases.

Uncertainty in life

The statistics around investors’ cash holdings look at dealing accounts rather than household assets, so any cash should be that an investor is looking to invest in the short term. Sensible investors have cash holdings to cover emergencies or for shorter-term savings goals. However, given that many hold their investments in tax-sheltered accounts, money that may or may not be required in the short term can be held as cash in dealing accounts. An example would be receiving a medical diagnosis where someone may or may not require private medical treatment. In this case, holding higher cash levels until an investor knows whether they need the cash would be wise.

Better relative returns

There is a theory that lower interest rates should mean higher equity valuations because the future cash flows those businesses generate can be discounted at a lower rate and are worth more today. There are a couple of challenges with this argument, though. The first is the reason interest rates are low: because economic growth is slow or may likely tip into recession. This means that corporate earnings will be growing more slowly, on aggregate. The impact of lower discount rates and lower growth should cancel themselves out. On top of this, the “risk-free” rate is just one part of the discount rate calculation. The other is the risk premium that investors demand. When it comes to riskier equities, such as small caps, a risk premium may well be 15% or more. So, a 1% drop in the risk-free rate from 5% to 4% reduces the discount rate from 20% to 19%. This shouldn’t move the valuation needle by much.

Investors shouldn’t fall into the trap of holding higher cash balances simply because equity multiples are contracting. Indeed, this should make investing in stocks far more attractive. However, there is no avoiding the reality that earning a 5% return in a bank account is far more attractive than holding cash earning nothing. If an investor regularly rebalances, holding another asset with uncorrelated returns adds value to an investment strategy. Hence, the key to this strategy is to have a target weighting for cash or short-term government bonds as an asset class and periodically rebalance the portfolio to this ideal.

Bad reasons for holding more cash

Being worried about the economy

Equity returns are correlated to GDP. The problem with taking advantage of this fact is that the equity markets lead GDP, usually by about six months. Not only that, but early GDP figures tend to be heavily revised over time, making them particularly unsuitable on which to base investment decisions. If investors wait for GDP to grow strongly, they may well miss the bulk of the bull market.

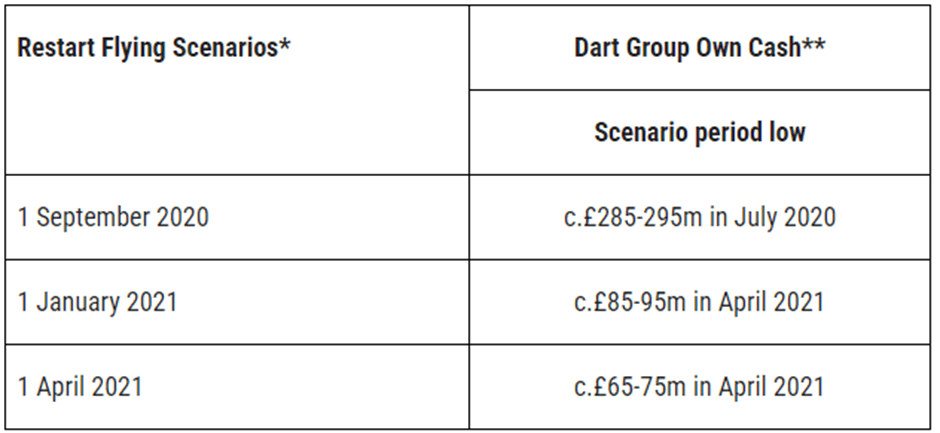

An informative example would be the COVID period. Equity markets sold off heavily in February and March 2020 in response to increasingly worrying news about the global economy due to the pandemic. However, stocks had bottomed by the end of March and rose rapidly from there. The challenge to equity investors was that the pandemic and economic news continued to get far worse for a significant period. Travel businesses were particularly badly hit. The Jet2 share price dropped to around £3 in mid-March 2020. However, by the time they raised money from the market in May 2020, the share price had bounced to the £8 level. They said:

"Based on the indicative scenario planning undertaken by Dart management detailed above, the Board is of the belief that the proceeds from the proposed Placing and the CCFF facility, in addition to potential additional bank debt and/or further mitigating actions (to the extent deemed necessary), will provide sufficient liquidity to deal with this most challenging of trading environments."

These were the restart flying scenarios given (they were known as Dart Group at the time):

However, lockdowns, quarantines and various other restrictions were still in place in early 2021, yet the price had risen to close to £15/share. So, it is no surprise that by February 2021, they had to come back to the market again with an equity raise. All travel restrictions like COVID testing were not removed until March 2022. Anyone trading on the news flow alone during this period would have lost a lot of money.

Trying to time the market

As already explained, most investors have terrible market timing instincts. Unless investors have a strong track record of selling prior to times of stock market weakness and getting back near the nadir, they should not attempt this. They are more likely to harm their returns than enhance them.

Buying the dip

Some investors are happy to sit in significant amounts of cash for long periods and are willing to be greedy when others are fearful and deploy that capital. Unfortunately, even such brave souls may not be improving their returns. Samuel Lee simulated a simple strategy of buying the stock market index on varying levels of weakness and then selling once the market had returned to the level prior to the drop, or after different periods: one, three or five years. Using US market data from 1926-2016 and drawdown thresholds of -10% through to -50%, Lee found that every single combination of drawdown threshold and holding period generated poorer returns, both on an absolute basis and a volatility-adjusted one, than a simple buy-and-hold strategy. The best of the buy-the-dip strategies was to buy on a 45% drawdown and hold for five years, but even this had a Sharpe Ratio (a measure of return per unit of volatility) of 0.26 compared with a Sharpe Ratio of 0.34 for a buy and hold strategy over the same period. It seems a mechanical buy-the-dip strategy doesn’t work. Discretionary strategies are unlikely to fare any better.

Investing Styles

The final factor that may impact cash holding is the investment style. Strategies that take the long-term view, such as Buffett & Munger-style investing, where the bulk of the returns come from internal compounding within the business, should almost always be fully invested. Such investors need to be wary of fundamental changes to these businesses that may short-circuit the compounding process. However, while compounding is in place, holding significant cash balances misses out on that driver of returns.

Quantitative strategies, where investors invest in a target number of stocks with certain metrics, such as income strategies or Ed Croft’s NAPS strategy, should also be fully invested, apart during the brief period of periodic rebalancing. Again, the investor is looking for exposure to specific factors likely to generate positive returns over time and holding cash doesn’t give that exposure.

Strategies that require more rapid reactions to stock-specific share price movements should perhaps hold a cash buffer to enable these actions to be taken rapidly. This may include some Value or Momentum strategies. Given the risks of holding too much cash, the buffer should be relatively small. Whatever an investor’s chosen style, it pays to think through the right level of cash they should hold and be consistent in targeting that level.