The price of uranium recently broke out to its highest price in more than a decade. This article, contributed by a subscriber, delves into the evolving dynamics of uranium supply and demand, highlighting the growing uranium deficit and the exciting investment opportunities in this resurging sector.

A brief history of the Uranium market

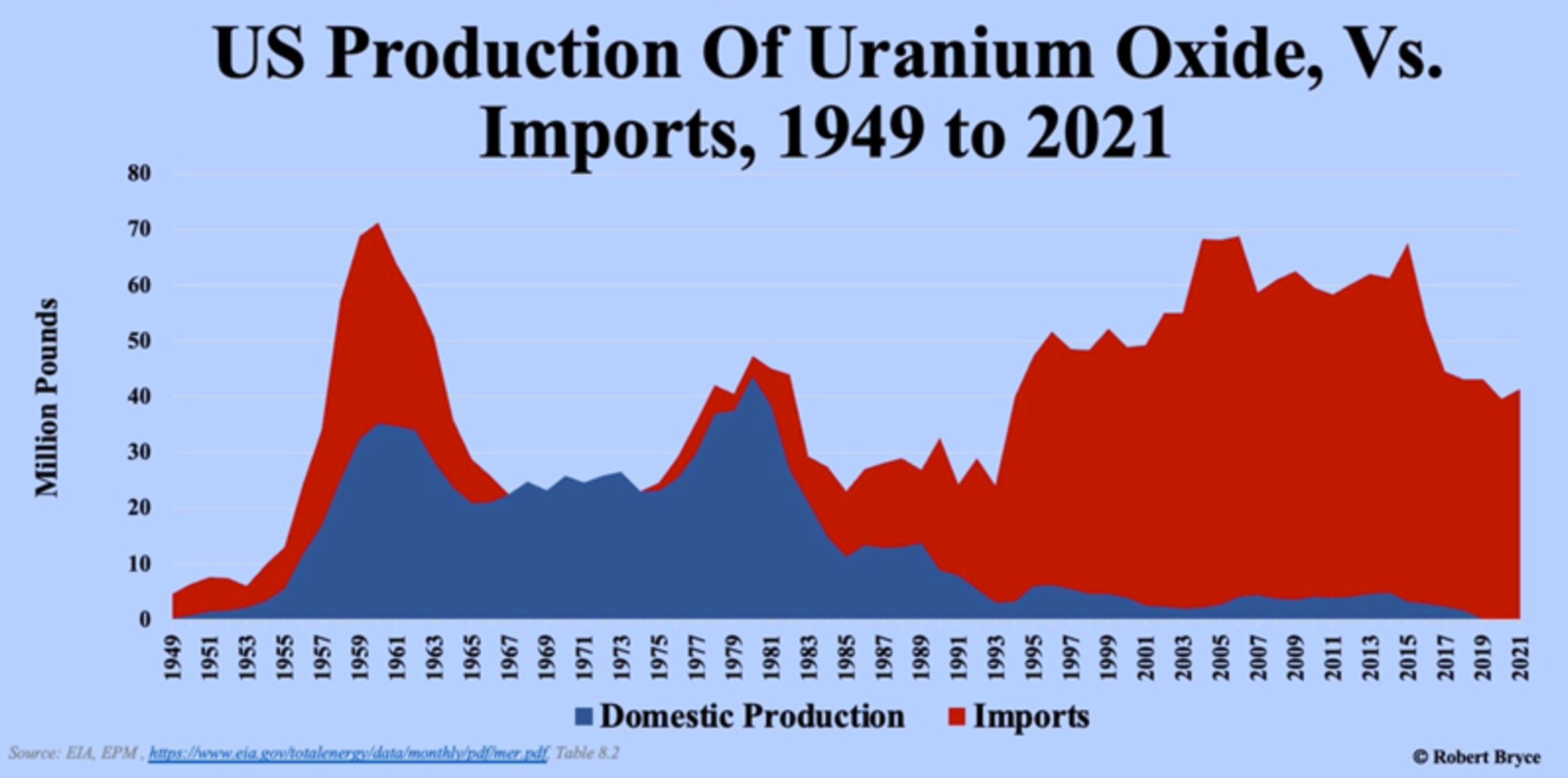

In 1980 the USA was self-sufficient in both mined Uranium and enrichment. In 1987, the Megatons to Megawatts programme (The INF Treaty) was signed by Reagan and Gorbachev to eradicate US and USSR nuclear weapons. The USSR thereby took on all the reprocessing of weapons-grade plutonium to reduce it for normal energy reactor use. The Treaty, an enormous political success, destroyed the US enrichment and mining industries.

The strangulation of US production capacity was made graver by the Collapse of President Nixon’s Project Independence: a plan to build 1,000 reactors. The US had started this massive building program in 1973; over 440 reactors were provisionally ordered but by 1990 only 111 had actually been commissioned and were operational.

The US became progressively more anti-nuclear, as did the rest of the world, after Three Mile Island (1979), Chornobyl (1986), and Fukushima Daiichi (2011).

Environmentalists and Green Parties in the US, Japan, Belgium, Germany, Canada, Sweden and elsewhere succeeded in decommissioning nuclear plants, further shrinking demand for yellowcake. Sweden, for example, voted in a non-binding referendum in 1980 to phase out nuclear power. It shut down six of its 12 reactors.

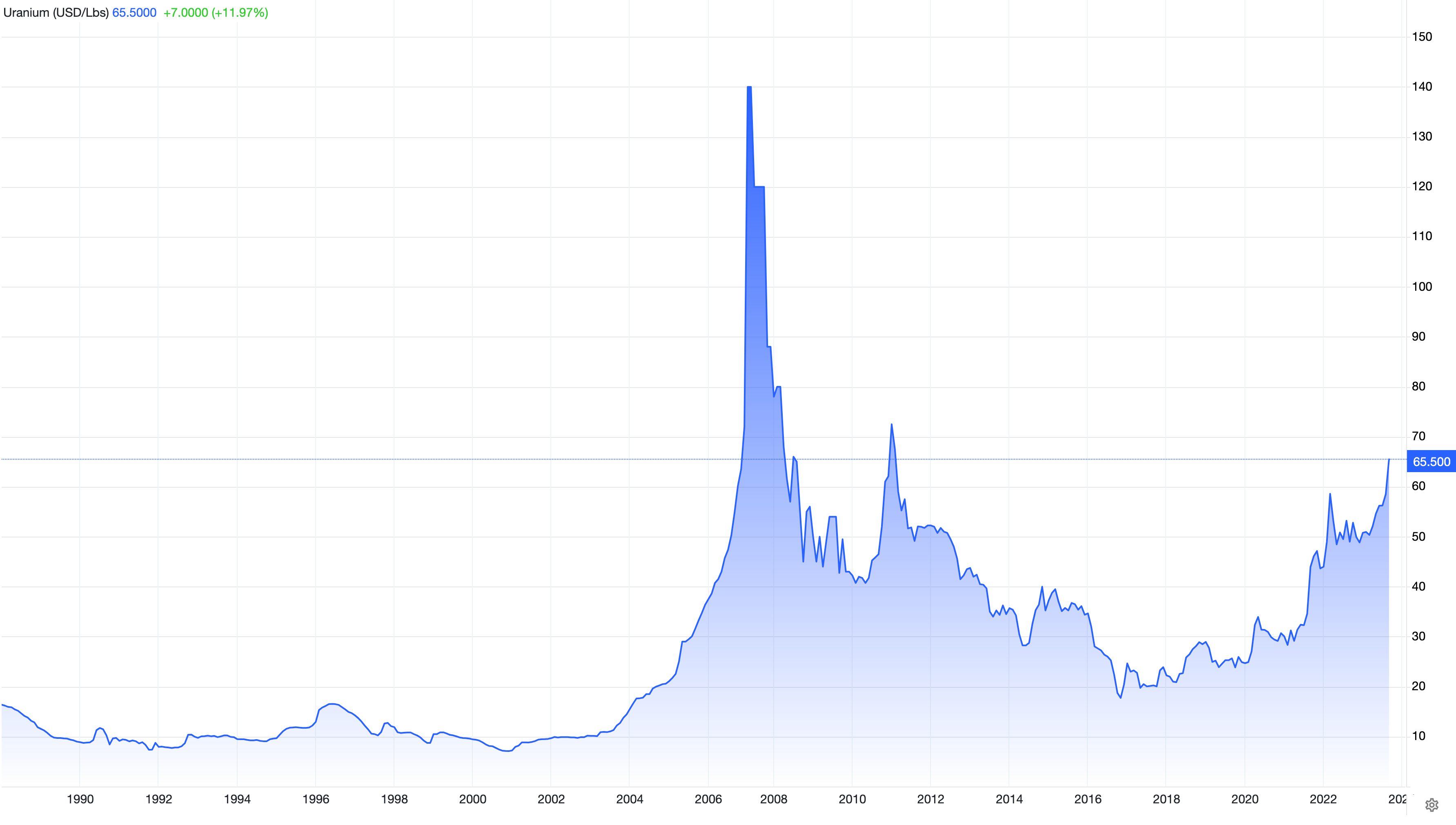

The world price of yellowcake and enriched uranium (SWU) collapsed and both traded below their production costs for many years.

Problems in Cameco's Athabasca Basin, Saskatchewan mines led to shutbacks. The number of quoted uranium and nuclear companies halved. The uranium market was consistently oversupplied.

The main survivors in nuclear supply apart from Cameco (CCO) and Kazatomprom (KAP) were the state-sponsored and government-owned companies of Russia (Rosatom), France (Orano), China (CNNC), and Belgium/Germany/UK (Urenco).

Russian supply was waning by 2020; no new mines were being commissioned but the market was coming into balance. China was rolling out a major nuclear expansion and a modest revival was underway in Europe.

Geopolitics has fractured supply lines

22nd February 2022 upended the landscape. Skyrocketing European and world gas prices led electricity higher. The realisation that a hostile Russia controlled not just the European…