As part of the Stockopedia Strategy Map, I have been taking a look at some SuperStocks, stocks that score highly on all three Quality, Value and Momentum Ranks. Last week, I took a deep dive into a SuperStock I know well: Quarto (LON:QRT) . This week, I pick three small cap Superstocks with StockRanks of 97 or over, which may be worth researching further: Severfield (LON:SFR) , Costain (LON:COST) and Tclarke (LON:CTO) .

Severfield (LON:SFR)

Profile

Severfield Rowan is a designer, manufacturer, and fabricator of structural steel. The type of projects are best known for are stadia and multi-storey car parks. However, they have recently had a divisional restructure into Commercial & Industrial, Nuclear & Industrial and Modular. By focusing on the latter two divisions, the company believes it can drive greater revenue growth, with less cyclicality and higher margins than their more traditional business. They have also undergone a multiyear operational improvement programme called Project Horizon. This has more than 100 initiatives to improve client service, boost productivity, and enhance their competitive edge over smaller rivals.

They are also not opposed to growing via bolt-on acquisitions either. They acquired Harry Peers in 2019. In April of this year, they acquired Dutch fabricator VSCH for E24m in cash. This gives Severfield a production foothold in Europe, which the group has previously supplied from the UK.

The Stockopedia algorithm rates the company highly for all the individual StockRanks, giving it a 99 StockRank overall:

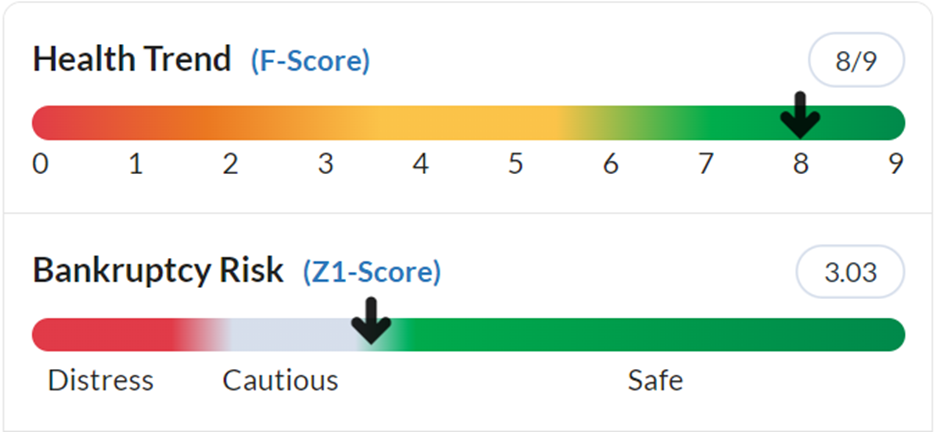

Quality

The high Quality Rank is primarily driven by the high Piotroski score due to positive sales and earnings trends. The bankruptcy risk is also low:

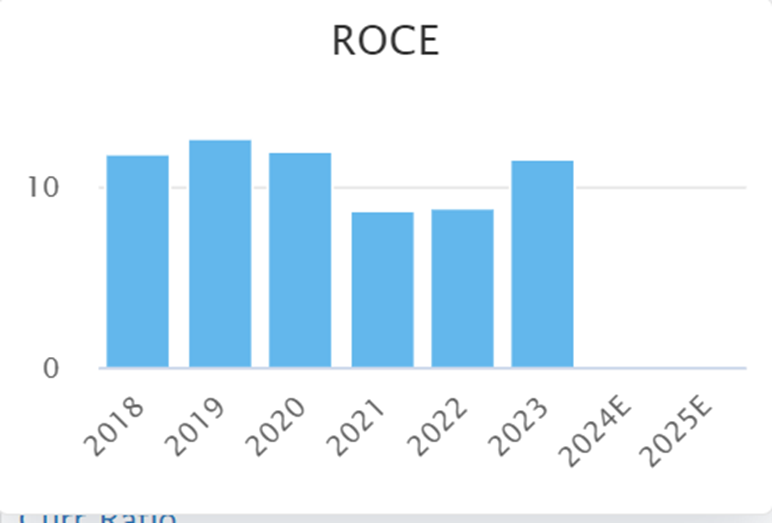

However, the company's return on capital is not particularly impressive and may be below their cost of capital over the last few years:

This is a capex-heavy industry. Although we have yet to see the full impact of their initiatives to boost productivity, a lot of work is required to get this up to a level that long-term shareholders will be happy with. If they remain a low-ROCE business, the market is unlikely to give them a higher earnings multiple, meaning that any shareholder returns will come from earnings growth alone.

Value

The…