After a stellar 2020 (FY21), the UK’s largest bicycle and motoring parts retailer, Halfords, has seen its fortunes take a turn for the worse. Whilst the lockdowns led to a significant rise in the demand for bikes, and the travel restrictions a notable increase in the demand for spare car parts necessary for domestic travel, the company is now suffering from some post-lockdown headwinds.

Source: Halfords website (The Investment Case pdf)

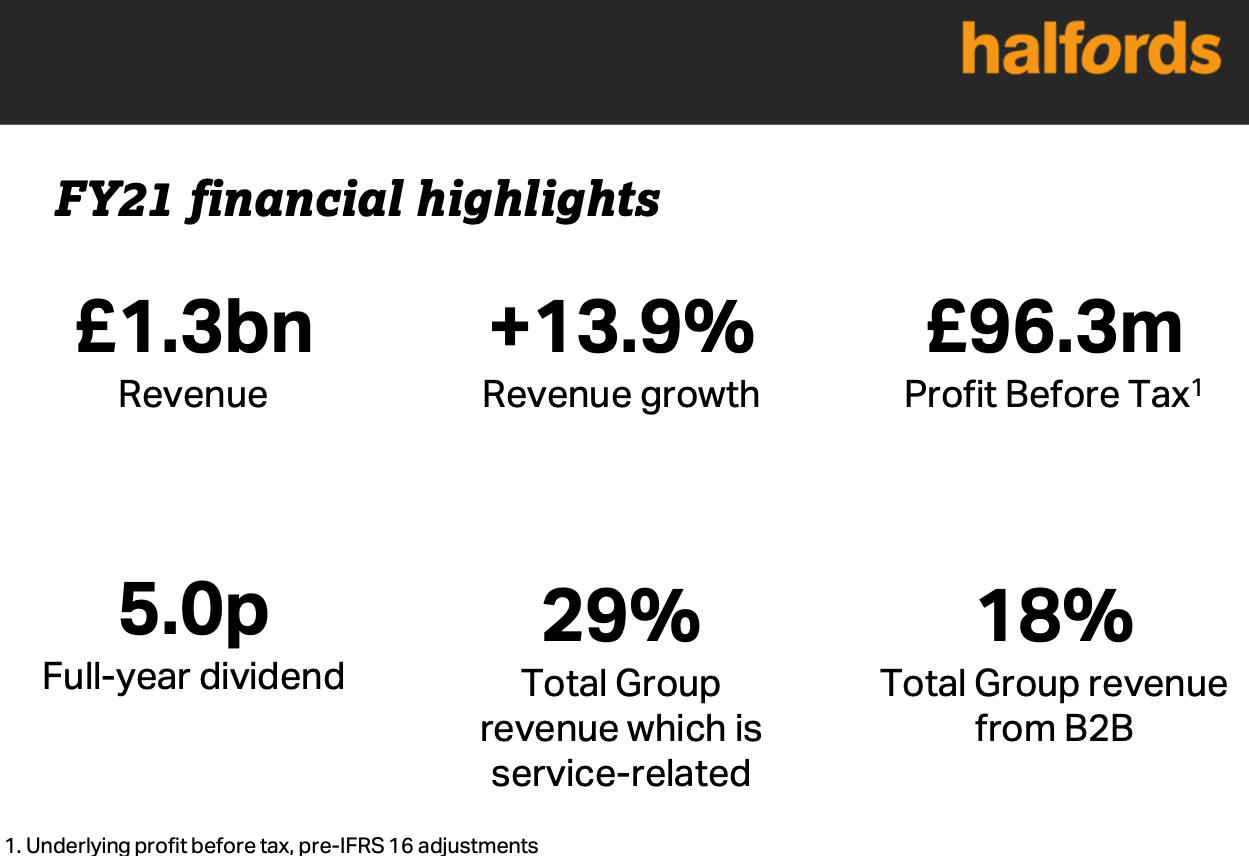

Halfords managed to generate £96.3 million in profits before tax last year, being a clear beneficiary of the government's granting of ‘essential’ status for its shops during lockdown and the subsequent unprecedented demand for its products & services.

However, in the company’s most recent trading update it announced that despite a strong start to the year, the trading environment was ‘challenging’. This has been primarily due to global supply chain issues, which have had a notable impact on the group’s cycling division.

Since reaching a high of £4.35 a share last summer, the shares have fallen over 36% despite upbeat comments from management about prospects for the next year. Trading on a forward price to earnings ratio of 8.5, does Halfords represent an interesting contrarian opportunity?

Profile

What are the company's principal business activities, how does it generate its revenues?

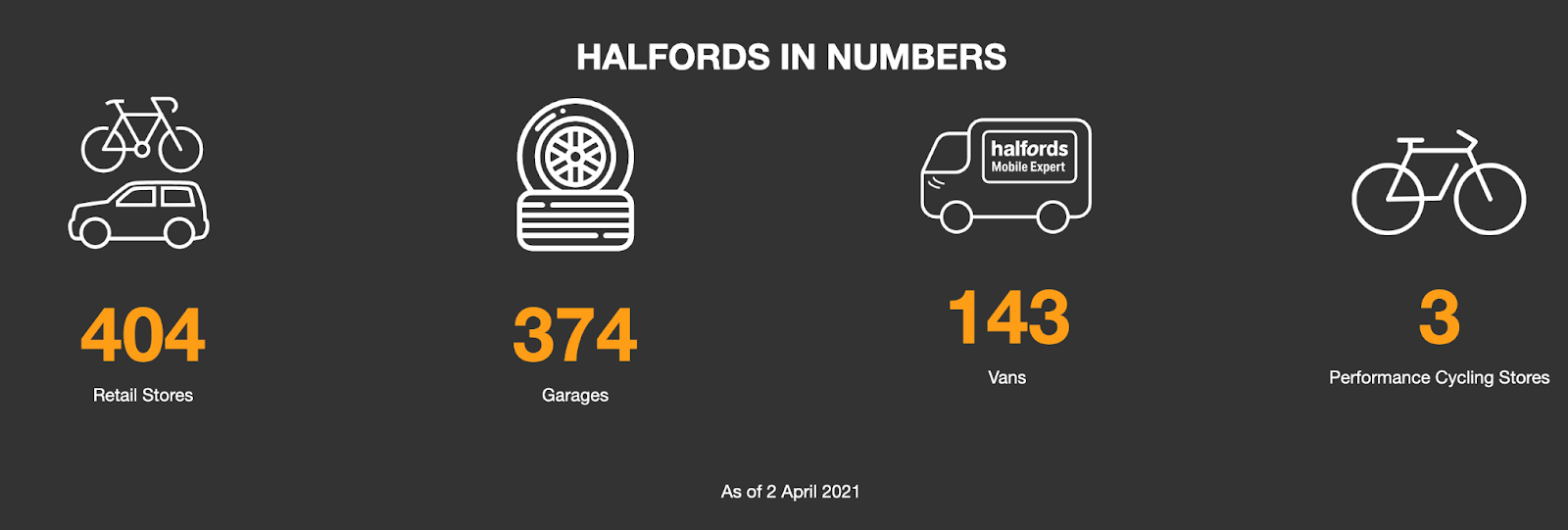

With 404 retail stores, 3 performance cycling stores, 374 garages, 143 ‘Mobile Expert’ vans and 185 commercial vans, Halford’s is the market leader in the UK for cycling and motoring products and services. The company currently holds around a 20-25% market share in its respective markets.

On the product side, Halfords offers Mainstream Cycling, Performance Cycling and Motoring Products. In 2020, the company saw sales of electric bikes, e-scooters, performance bicycles and traditional bicycles soar as people took to bikes during lockdown.

When it comes to services, Halfords is a specialist in not just Retail Cycling, but also car servicing and aftercare through its Autocentres/Mobile Experts and Retail Motoring divisions.

Halfords currently derives the majority of its revenues from mainstream cycling division (33%), whilst motoring products comes in at a close second (32%). However, the company’s fastest growing division over the last few years has been its services offering, in particular its Autocentres Mobile Expert services, which have proven…