Good morning from Paul & Graham.

That's all we've got time for today, see you tomorrow! I want to circle back to Keller at some stage, but am too tired now.

FTSE 100 futures are showing we could be in for nice bounce today. Has this been a "flash crash" I wonder? Hope so, as I did some buying yesterday for 11 shares that had been on my watchlist, but were put on mid season sale earlier this week! After all, the idea is to buy low and sell high (BLASH), something that's easy to forget when caught up in the drama of a sudden sell-off.

Explanatory notes -

A quick reminder that we don’t recommend any shares. We aim to review trading updates & results of the day and offer our opinions on them as possible candidates for further research if they interest you. Our opinions will sometimes turn out to be right, and sometimes wrong, because it's anybody's guess what direction market sentiment will take & nobody can predict the future with certainty. We are analysing the company fundamentals, not trying to predict market sentiment.

We stick to companies that have issued news on the day, with market caps (usually) between £10m and £1bn. We usually avoid the smallest, and most speculative companies, and also avoid a few specialist sectors (e.g. natural resources, pharma/biotech, investment cos). Although if something is newsworthy and interesting, we'll try to comment on it. Please bear in mind the "list of companies reporting" is precisely that - it's not a to do list. We typically cover c.5 companies per day, with a particular emphasis on under/over expectations updates, and we follow the "most viewed" list of readers, so if you're collectively interested in a company, we'll try to cover it. Obviously with the resources available, we can't cover everything! Add you own comments if you see something interesting, and feel free to discuss anything shares-related in the comments.

A key assumption is that readers DYOR (do your own research), and make your own investment decisions. Reader comments are welcomed - please be civil, rational, and include the company name/ticker, otherwise people won't necessarily know what company you are referring to, if they are using unthreaded viewing of comments.

What does our colour-coding mean? Will it guarantee instant, easy riches? Sadly not! Share prices move up or down for many reasons, and can often detach from the company fundamentals. So we're not making any predictions about what share prices will do.

Green (thumbs up) - means in our opinion, a company is well-financed (so low risk of dilution/insolvency), is trading well, and has a reasonably good outlook, with the shares reasonably priced. And/or it's such deep value that we see a good chance of a turnaround, and think that the share price might have overshot on the downside.

Amber - means we don't have a strong view either way, and can see some positives, and some negatives. Often companies like this are good, but expensive.

Red (thumbs down) - means we see significant, or serious problems, so anyone looking at the share needs to be aware of the high risk. Sometimes risky shares can produce high returns, if they survive/recover. So again, we're not saying the share price will necessarily under-perform, we're just flagging the high risk.

Others: PINK = takeover approach, BLACK = profit warning, GREY = possible de-listing.

Links:

Paul & Graham's 2024 share ideas - live price-tracking spreadsheet (2 separate tabs at bottom), Video update of results so far, June 2024.

Frozen SCVR summary spreadsheet for calendar 2023.

New SCVR summary spreadsheet from July 2023 onwards.

Paul's podcasts (weekly summary of SCVRs & macro views) - or search on any podcast provider for "Paul Scott small caps" - eg Apple, Spotify.

Phil Hanson's data analysis measuring performance of our colour-coding system in the SCVRs, from July 2023- Mar 2024 (with live prices). My video explaining/reviewing it.

My other video (June 2024) - How to screen for broker upgrades on Stockopedia.

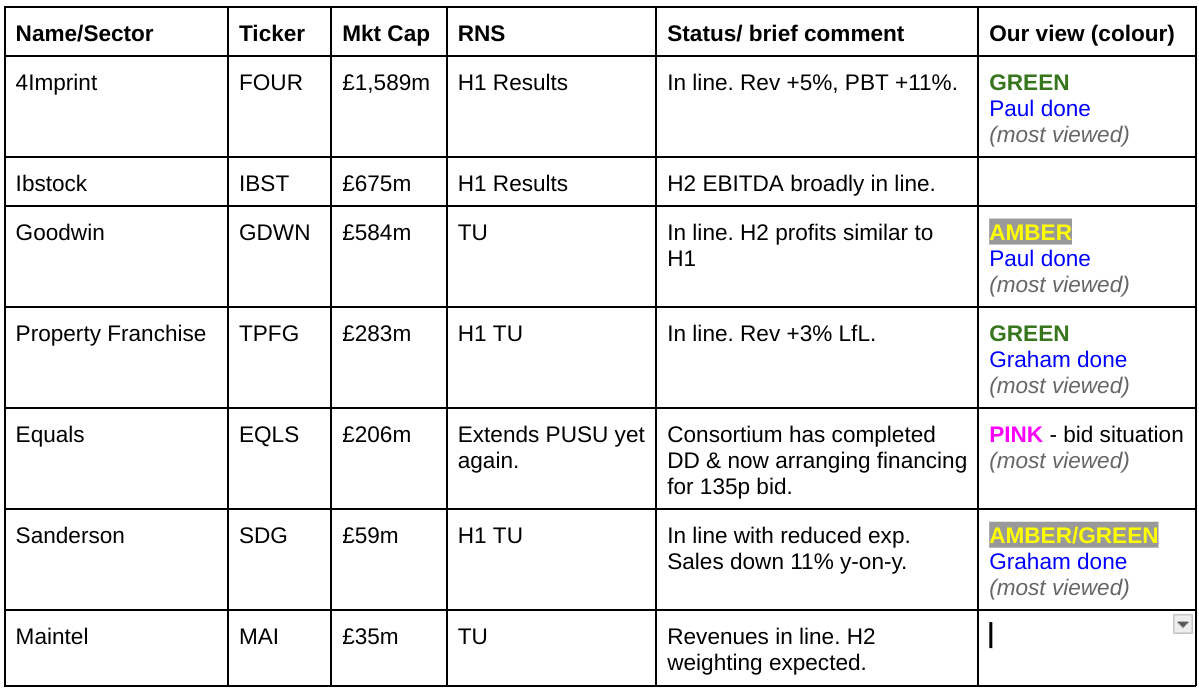

Companies Reporting

Summaries

Hostmore (LON:MORE) - down 19% to 12.2p y’day (£15m) - Updates on Corporate Actions and Trading - Paul - RED

Mgt are trying hard to salvage the situation here, but I suspect things might be slipping out of their control, with worsening recent trading, and the bombshell yesterday that it's seeking additional financing to prevent a breach of its existing borrowing limit imminently. Way too risky to get involved, is my view. So I'm sticking with RED.

Goodwin (LON:GDWN) - 7,780p pre-market (£584m) - FY 4/2024 Results - Paul - AMBER

Good results, but as always the stretched valuation limits how enthusiastic I can be. As before, I really like the company, and am impressed by performance, but the share price is now way above what I personally would be prepared to pay. Cashflows are not great, and it glosses over the reality of increased net debt year-on-year, by instead focusing in the commentary on an H2 reduction in debt.

Property Franchise (LON:TPFG) - up 2% to 465p (£291m) - Half Year Trading Update - Graham - GREEN

A very pleasing trading update with the outlook for the company to achieve full-year results “at least in line with expectations”. The merger with Belvoir and a subsequent cash-purchase acquisition have left the company with a modest debt load. I’m still excited about TPFG’s future but a significantly higher market cap is now starting to price in the company’s excellent prospects, in my view.

Sanderson Design (LON:SDG) - up 2% to 84p (£60m) - Half Year Trading Update - Graham - AMBER/GREEN

I don’t normally cover this fabric/wallpaper group but can understand why it has received positive commentary here before. The company is now seeing some signs of improvement after a very challenging period of trading, particularly in the UK, and it is trading in line with reduced expectations. The market cap strikes me as undemanding given the company’s many attractions, with the main drawback being the lack of top-line growth over the long-term.

4imprint (LON:FOUR) - down 2% to 5,505p (£1.55bn) - Half Year Results - Paul - GREEN

Good H1 results, despite challenging market conditions. A spectacular multibagger over the long term, and I remain enthusiastic about many aspects of this share.

Paul's Section:

4imprint (LON:FOUR)

Down 2% to 5,505p (£1.55bn) - Half Year Results - Paul - GREEN

I tend to briefly cover this mid-cap here because it’s a wonderful company, that has 50-bagged over 15 years!

Previously here -

19/1/24 - Paul - GREEN - 4635p - slightly ahead exps TU.

13/3/24 - Paul - AMBER/GREEN - 5940p - in line TU.

FOUR sells promotional goods with customers’ brands printed on them, mainly in the USA, so a huge market. Funnily enough, on my recent trip to meet extended family in Washington DC, I usually leave the TV on in the background in my hotel room, and was pleased to see 4Imprint TV ads appearing frequently. Which tells me they’re on the front foot, but also that they would have scope to dial down marketing spend if required, eg -

“with the reshaped marketing mix demonstrating the efficiency and flexibility that we expected against a softer economic backdrop.”

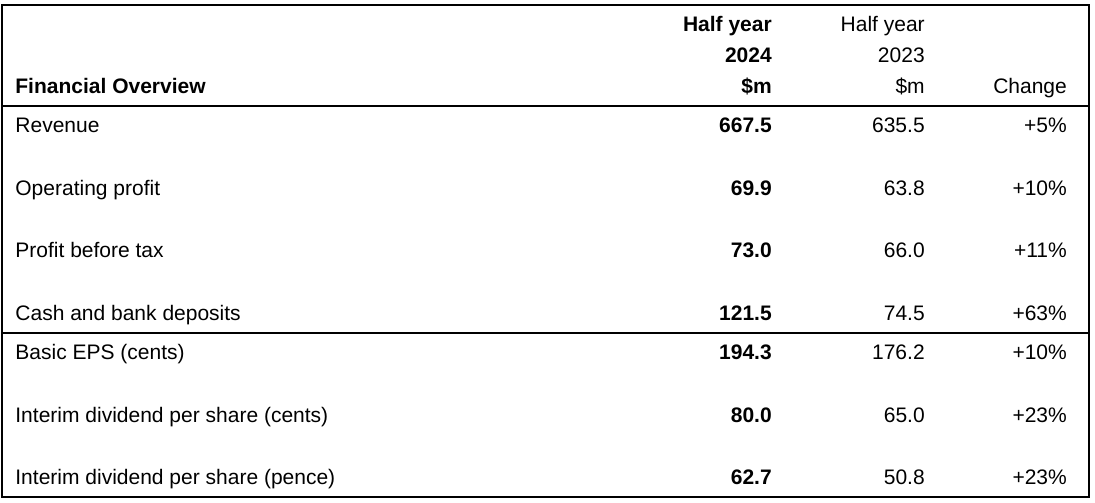

H1 figures today - this is very quick reporting, just over 5 weeks after the half year end.

“4imprint Group plc, (the "Group"), a direct marketer of promotional products, today announces its half year results for the 26 weeks ended 29 June 2024. The results for the half year and prior half year are unaudited.”

“Strong financial performance; taking share in challenging market conditions”

Some nice numbers in the H1 highlights, note this is US dollars/cents -

Outlook -

“Based on our first half financial results and recent internal forecasts, the Board expects that 2024 full year Group revenue will reflect a growth rate similar to the first half of the year. As a result of improving financial dynamics in the business, particularly higher gross profit percentage and the flexibility of the marketing mix, it is expected that profit before tax for the 2024 full year will remain within the current range of analysts' forecasts.

The Board is confident in the Group's ability to manage through the current market conditions, blending resilient near-term financial results with attractive prospects for significant further organic growth over the medium term…

In summary, our strategy remains the same - to deliver attractive organic revenue growth by increasing our share of the fragmented yet substantial markets that we serve.

We take a long-term view of the business and its future development. This includes making necessary investments in the people, marketing resources and infrastructure required for success, regardless of the immediate market conditions. Experience has taught us that if we remain diligent in looking after the business in more difficult times, a market share opportunity tends to follow.

Brokers - there are 3 broker updates available on Research Tree. I’ll look at Edison, as that’s directly commissioned by FOUR. It trims revenue, but slightly raises profit for FY 12/2024, to 405 cents. Convert at 1.27, and that’s 319p. So at 5,505p, that’s a 2024 PER of 17.3x, which I think is reasonable, given that this is a year where market conditions are seen as challenging. Hence there could be upside once an economic recovery is (hopefully) more established in the USA, currently an unknown factor that markets are trying to figure out.

Balance sheet - is very healthy. It’s a strikingly good business model, with hardly anything in inventories, and quite modest receivables too. So it looks as if they possibly drop ship products, and/or send things out as soon as they arrive. That makes sense, since product will be personalised to each customer’s brand. Hence it’s sitting on a healthy & rapidly growing $121.5m net cash pile, and can safely pay out most of earnings as divis, with the yield c.3.7%.

Cashflow statement - really impressive, it’s just a cash generation machine, which it pays out to shareholders, exactly what I like to see!

Paul’s opinion - this looks excellent, it’s a thumbs up from me again. Not obviously cheap, but I think if you take a long-term view, you should do well with this share. Providing nothing unforeseen goes wrong of course, as with any share.

I’ll put this on my watchlist, and might have to consider dipping in my toe if the current downtrend continues.

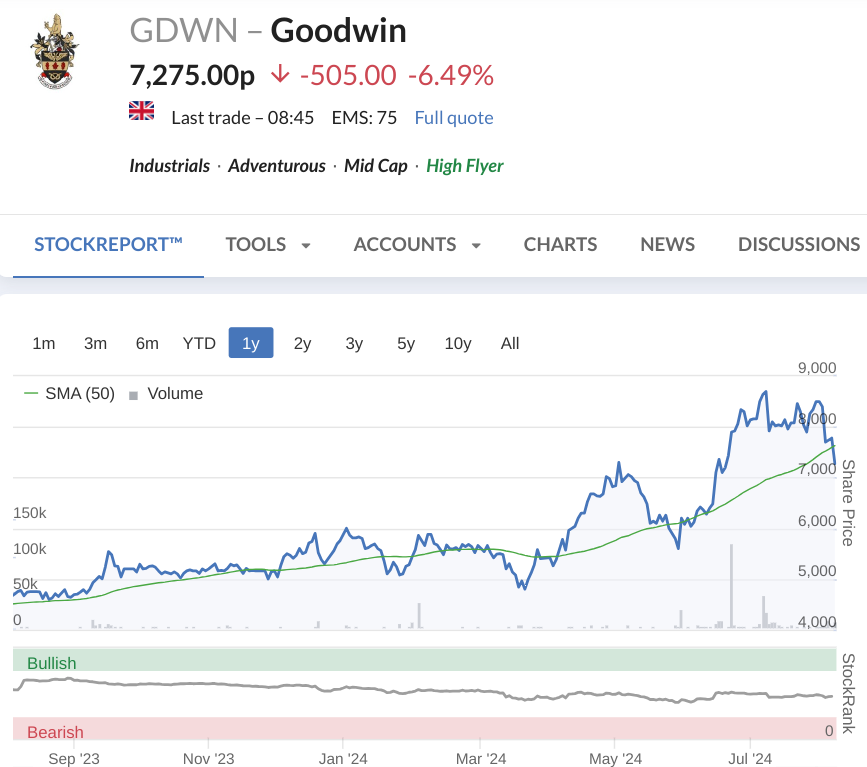

Goodwin (LON:GDWN)

7,780p pre-market (£584m) - FY 4/2024 Results - Paul - AMBER

From Goodwin’s website -

“Goodwin PLC is a group of established mechanical and refractory engineering companies, specialising in the design, manufacture and supply of high-quality products and solutions.

Goodwin PLC’s subsidiaries manufacture and operate in over ten countries worldwide, enabling the Group to capitalise on local market growth and take new products to market quickly, in both the established and emerging markets.”

Why can’t companies give examples of the main products that they make, instead of general descriptions like the above?

We’ve reviewed GDWN here 3 times in the last year - you can see a consistent querying of the valuation, but approval of performance, and me being more positive than Graham! Despite the high valuation, this has been a case where running your winner has played out well so far -

11/8/2023 - 4745p - Paul - AMBER/GREEN - Good FY 4/2023 results, fully priced maybe?

20/12/2023 - 5424p - Graham - AMBER - Profit up, large order book, but looks expensive.

14/3/2024 - 5240p - Paul - AMBER/GREEN - In line TU.

This share was also one of my top 20 shares ideas in 2023, and has been a star performer, currently up 128%.

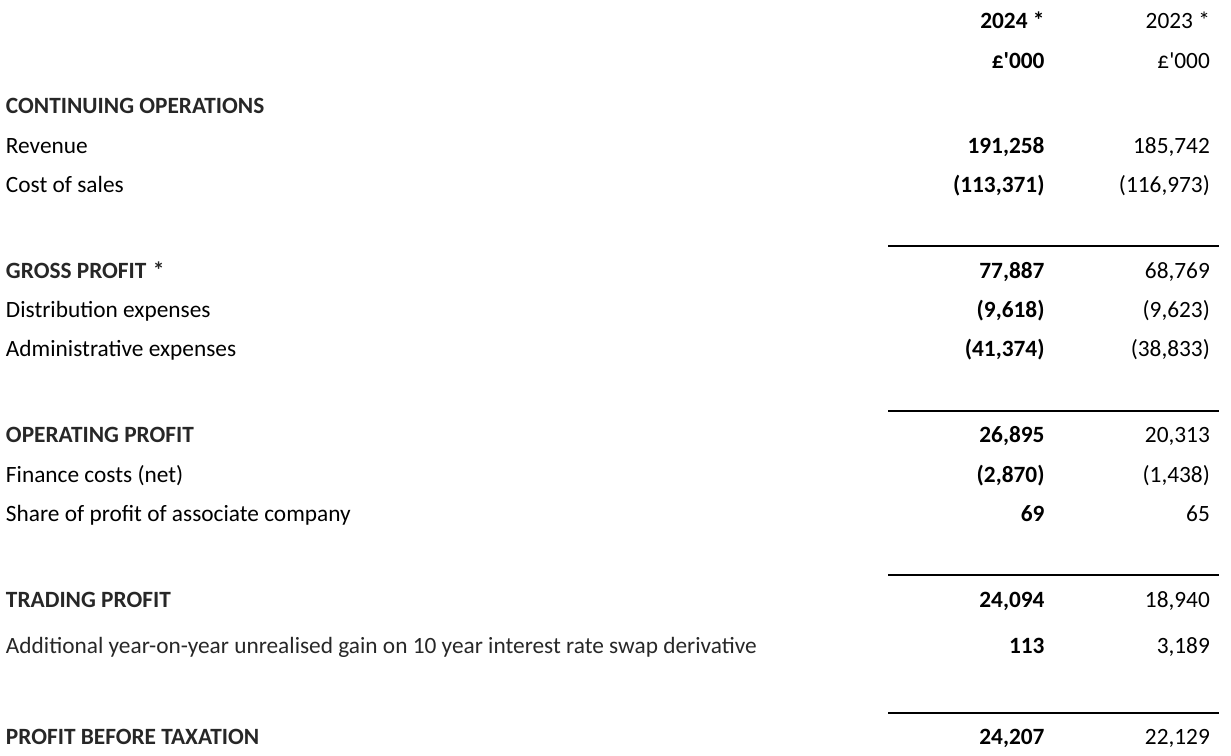

That’s set the scene and refreshed my memory, so let’s move on to the FY 4/2024 results out today.

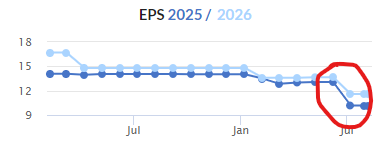

Decent figures here, with PBT up 9% to £24.2m.

Note that last year was boosted by a derivative gain of £3,189k, so the better comparative of underlying performance is the “Trading Profit” figure below of £24,094k, up a much more impressive 27%.

How does this compare to forecasts? I can’t find any broker notes, a consistent problem with Goodwin, which is run like a private company unfortunately. However, it’s moving in the right direction, with the recent introduction of quarterly trading updates. Shore Capital said previously it intended issuing a more detailed research note, but I can’t see that as yet on Research Tree. Hopefully it’s gestating, maybe they wanted full year numbers published before committing to forecasts?

EDIT: a one-pager has just come through from Shore, but it just summarises the RNS, and doesn't contain any forecasts.

Guidance from Goodwin itself on 14/3/2024 allowed me to simply work out a 231p EPS estimate here in the SCVR on 14/3/2024. Today’s actual of 224.5p is slightly below my estimate, but not enough to make much difference.

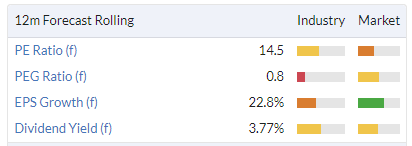

Valuation we already knew was high, and at 7,780p/share the 231p EPS gives a PER of 33.7x - I know we keep saying it’s expensive, and it keeps rising in price, but surely there has to come a point where people bank profits? What level would be too high? A PER of 40, 50, 60? Remember that it’s an engineering company, not a tech exponential growth story!

Balance sheet - NAV is £127m. That includes £26m in intangible assets, so £101m NTAV - a healthy position.

As you would expect in the engineering manufacturing sector, Goodwin is capital-intensive, with £105m fixed assets (property, plant and equipment). Working capital is strong, with £74m net current assets. However, this is funded with £62m of non-current borrowings.

Overall it’s OK I think, but Goodwin doesn’t have the substantial surplus capital of Castings (LON:CGS)

Cashflow statement - looks similar to last year. Net operating cashflow (post tax & finance costs) was £27.1m this year, vs £29.1m last year. Near enough to make no difference.

Capex was considerable, at £16.9m this year, consuming 62% of cash generated. A reminder that this is a capital-intensive business, meaning that there’s little scope to pay out much in divis.

After capex, cash generation was only £10.2m, less £2.9m lease costs, gives £7.3m cashflow remaining.

It then spent £8.9m on buybacks, and £8.6m on divis, which was really an overspend, funded by increasing net debt.

These full year cashflow figures are completely at odds with the company's commentary, which talks about having reduced net debt, and absorbing heavy capex whilst also paying out divis and doing a tender offer. However, net debt actually rose year-on-year, from £34.3m in April 2023, to £45.3m at April 2024 (I think that might include leases, as they're not shown separately on the balance sheet). What they’ve done is highlight that net debt fell in H2, from £54.6m at end H1. So I find the “Cashflow” section of the commentary misleading, since it ignores the net cash outflow, and increase in net debt, for the year as a whole.

Overall then, cashflow is not great, and they’ve paid shareholder returns out of increased net debt - the opposite of what their commentary says!

Interest rate swap - I’d forgotten about this, but GDWN made a very shrewd move to lock in low interest rates, thus boosting profitability now -

“The interest rate swap continues to benefit the Group as it locked in a very preferential borrowing rate of less than 1% up to 2031 on the Group's first £30 million of debt.”

Order book - is similar to last year at this stage - but the commentary says big contracts are multi-year, repeating type orders. So the likely order pipeline could be a lot larger than the published order book figures.

“Currently, as of the date of writing this report, the Group's cumulative future orders stand at £264 million (August 2023: £271 million)”

Dividends - increased to 133p (LY: 115p) but due to the very high share price, this is only a 1.7% yield, and as flagged above in the cashflow section, I question whether GDWN can afford even this fairly modest payout?

Outlook - there isn’t a section on this, but details are scattered through the fairly detailed & useful commentary.

A couple of interesting excerpts -

“The continued increase in the performance of the Group in the financial year just ended is a result of the hard work and strategy to break into new markets coming to fruition. The profits have again taken a step forward as a direct result of the strategic investments that have been made over the last decade, and particularly the supply of mission-critical, high integrity components to the nuclear waste storage industry and key components for the naval propulsion and hull construction markets from the Mechanical Engineering Division…

The majority of the Division's forward order book relates to advanced solutions for the nuclear waste storage industry and key components for the naval propulsion and hull construction sector. From the discussions that the sales teams of both Goodwin International and Goodwin Steel Castings have had with their key customers, it is expected that there will be more orders for the same components in the coming years. Furthermore, a significant proportion of this workload consists of repeat orders for components where we have already overcome many of the manufacturing uncertainties, allowing us to realise future production efficiency gains on these repeat components.”

Paul’s opinion - I’m a bit concerned the valuation is now looking too stretched, but we say that every time!

From talking to bulls in GDWN shares, their main interest seems to be in the potential for nuclear waste related orders to be highly lucrative over a long period of time. The outlook excerpts above do seem to back up that view.

Cashflow has underwhelmed me, and I take issue with the commentary glossing over the increased net debt by only focusing on the improvement since the H1 results.

Short term, I can’t justify being anything other than AMBER, due to a stretched valuation. However, on fundamentals, it sounds like the company is likely to keep doing well. So with a say 2+ year view, I’d be looking at this as AMBER/GREEN. On balance, I think for now it has to be AMBER, and then I’d move back up to amber/green if there’s a pullback in price to something more sensible, say 20x earnings, suggesting a price target of 4,620p for me. The existing price of 7,350p (it’s down about 5% today at 09:52) is 59% above what I see as a fair valuation today. Bulls may well be proven correct longer term, but they’ve chased the price a long way above a reasonable level in the short term, in my view.

The company highlights its superb long-term track record - so it could well be the case that patience could remain a virtue with GDWN shares -

"the Total Shareholders Return including the dividends paid over the last 20 years is 4,632% (versus FTSE100: 282%)."

Shares have joined the FTSE 250 recently.

While I've been writing the above, the share price has had a pullback - it's a thinly traded share though, as I suspect most shares are locked away by long-term holders.

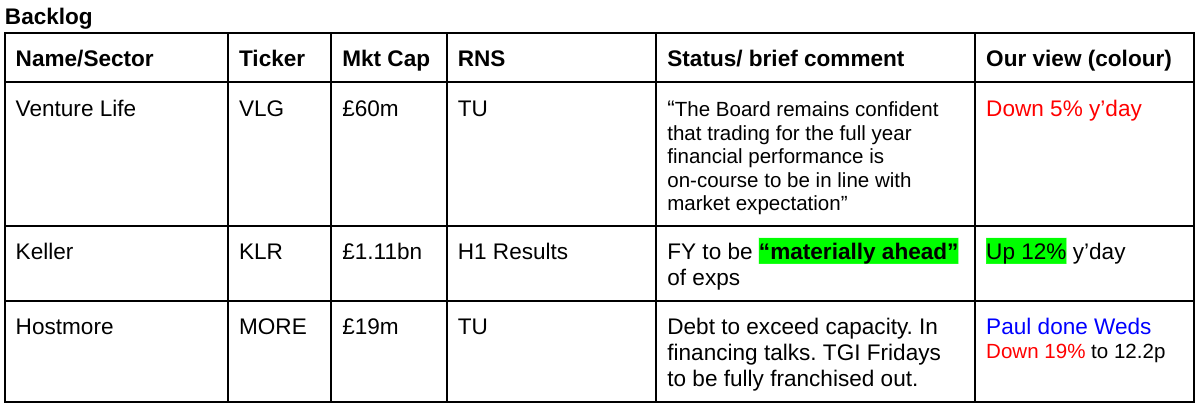

Hostmore (LON:MORE)

Down 19% to 12.2p y’day (£15m) - Updates on Corporate Actions and Trading - Paul - RED

This is the financially distressed UK franchisee of TFI Friday’s casual restaurants. A replacement management team are fighting hard to keep it afloat, strip out costs, etc. Debt is dangerously high, although the bank gave it some breathing space in an extension of the borrowing term. More recently it announced a surprising proposal to reverse the US franchisor into this UK listing, in a reverse takeover, that still seems to be work in progress.

I can’t see the point in getting involved here, when the risk is so high, so I’ve been negative on this share 3 times in the last year -

8/9/2023 - RED

3/5/2024 - RED

3/6/2024 - RED

Although as with everything, we keep an open mind, and change our view if the facts change.

As a reminder, RED is reserved for situations where we see substantial risks of insolvency or dilution, and a struggling business model.

Reverse takeover - they still haven’t agreed terms. Given that MORE’s share price has been significantly falling recently, it’s becoming clearer that this deal may not happen at all now, and if it does, the dilution is likely to be much larger than originally anticipated.

It says the existing 87 corporate stores will be sold off to franchisees, moving to a capital light model. Note that the c.$40m from disposals mentioned relates to the US company, which is not currently part of MORE.

Funding requirement from lenders will be less, thanks to the newly planned capital light, franchising model.

It’s not clear who these “related parties” are - possibly the US TGI's group it's trying to merge with?

“Instead, the parties are in discussions with their lenders and other stakeholders to repay or reduce existing indebtedness using proceeds from the sale of corporate stores and/or new facilities from related parties.”

Delay - the deal will not now complete by end Q3 2024, as previously intended.

Strategic review - is being undertaken to look at other options, in case the reverse takeover does not complete. What would this entail, it is not stated. Maybe a sale of the company, or a CVA perhaps (me speculating here).

Trading update - LfL sales were down c.10% YTD to late May 2024. Things have worsened in June & July, such that YTD LfL sales are now down 12%. That’s very bad, since costs will be higher. So I don’t see much future for this company unless it somehow manages to turn things around into rising LfL sales from now onwards.

H1 trading was loss-making, even at EBITDA (old basis), albeit not as bad as in 2023 -

“EBITDA (FRS102) in H1 2024 delivered a loss of £1.2 million, which was £2.6 million better than the £3.8 million loss in H1 2023. It is noteworthy that this improvement in EBITDA was after a reduction in revenue of £9.5 million for the period and, therefore, the EBITDA delivered underscores the positive impact of the cost reduction programme implemented in 2023 and the Group's ongoing strong operational discipline.”

Given the big depreciation charges on the stores, and heavy finance costs, this means the real profit (PBT) will be a heavy loss.

I don’t have access to any broker notes. Also the broker consensus figures on the StockReport don’t look right to me, as I think it’s clear MORE is heading for a substantial loss this year, not a profit.

The last balance sheet is a disaster area. Although most of the deficit on NTAV is due to negative lease entries. If these can be disposed of to franchisees, then that could help, although I imagine landlords would insist on a guarantee, in order to allow assignment of the leases. So leases on problem sites could revert back to MORE if a franchisee subsequently went bust.

Bank debt has risen in H1 - again, not the plan, it was supposedly going to quickly degear according to a previous presentation -

“As a result of trading in the period, H1 2024 ending net debt (FRS102) was £29.7 million as compared to £25.1 million at 31 December 2023.”

This is the worst bit below - it’s set to breach borrowing limits soon - this is a serious problem, and anyone still holding this share should be seriously asking yourselves why, when this risk is large, and imminent -

“The Board continues to expect that the Group's standalone peak net debt for the year, without giving effect to the closing of the Acquisition or any sales of the Group's corporate stores, will occur around the end of Q3 2024 due to routine working capital outflows, lower revenues in the period, and payment of transaction fees relating to the Acquisition. Borrowings during this period are likely to exceed the Group's existing borrowing capacity and so, as a part of the Strategic Review, the Board is in discussions with various parties regarding additional financing.”

Paul’s opinion - I think we could be witnessing the death throes of this share.

Casual dining is a horrible sector, where it’s difficult to make any money in the UK. There’s still far too much capacity, and the TFI Fridays format feels dated now. Costs have shot up in the last two years, especially wages, and cost-cutting can only go so far, before any further cuts would impede the ability to keep operating.

I suspect the reverse takeover deal might not happen, and even if it does, MORE shareholders are likely to be very heavily diluted.

Then we have the worst news that it’s about to breach its borrowing facilities.

Let’s hope they can salvage the situation, but I think it’s best to work on the basis that this share could easily end up a zero. So why get involved? The idea that this share could multibag seems potty to me, given how poor current trading is, and that the bank debt is rising, and dangerously high.

So with risk:reward looking unfavourable, I have to remain at RED. Very high risk, could be on its way to zero.

Graham’s Section:

Sanderson Design (LON:SDG)

Up 2% to 84p (£60m) - Half Year Trading Update - Graham - AMBER/GREEN

Note that SDG’s year-end is in January:

Sanderson Design Group PLC (AIM: SDG), the luxury interior design and furnishings group, announces its trading update for the six months ended 31 July 2024.

The company already issued a trading update (a profit warning) in late June, when it warned that trading conditions in the UK had deteriorated. Brand product sales were down 9% year-to-date, and down 14% in the UK.

It cut its underlying PBT forecast for FY Jan 2025 to c. £8m. Here’s the impact on the EPS forecast. The EPS consensus forecast on Stockopedia was reduced from 13.1p to 10.2p:

Today’s update is in line with the revised expectations:

…trading has showed [sic] some signs of improvement in July with brand product sales up 6% at constant currency compared with July last year. As a result, total brand product sales in the six-month period to 31 July 2024 were down 7% in constant currency, an improvement compared with being down 9% at the time of the June trading update and driven by North America.

Brand product sales aren’t the entire story here - we also have external manufacturing sales (£9.3m) and licensing sales (£4.1m).

H1 licensing sales are down by a noteworthy 41% which the company attributes to a strong H1 last year when there was accelerated income from deals with NEXT and Sainsbury’s. Full-year licensing is expected to be about the same as last year.

In aggregate, total sales are down 11%, or down 10% at constant currencies.

Highlights: Disney Home x Sanderson and Giles Deacon products for the Sanderson brand have been well received and the brand is selling well in North America and Northern Europe.

New licensing agreements include Zara Home and John Lewis.

Net cash has fallen from £16m (Jan 2024) to £10m. Cash outflows arose from the transfer out of a pension scheme, a temporary inventory build, and capex that is not expected to recur in H2. This all sounds reasonable and I’d expect a much better cash performance in H2.

Outlook: trading conditions remain challenging, but “expectations for full year cash and profits remain unchanged”.

…The previously announced initiative to deliver a more efficient sales model in the UK has recently been completed, achieving annualised savings of approximately £0.6 million of which £0.3 million will be delivered in the current financial year.

At the same time, the Company remains focused on the growth opportunity in the US market and has recently signed a five-year distribution agreement with Kravet Inc. for the distribution of Scion fabrics and wallpapers in the USA. Kravet Inc. already distributes the Clarke & Clarke brand in North America and this new exclusive agreement for the Scion brand is expected to drive the profile of the brand in the USA.

Graham’s view

I think Paul normally covers SDG but I’m glad to have had the chance to take a look at it.

My overall impression of the company is positive - it has great heritage, a nice track record of profits and dividends, a net cash position that still covers a chunk of the market cap, and a growth opportunity in North America. And I always sit up and take notice when I see licensing deals, as they have the potential to create a stream of risk-free pure profits.

The main drawback is that apart from the US-driven growth story, SDG’s other markets appear moribund. The overall growth picture is not great. Indeed, there has been hardly any top-line growth in recent memory.

Is everything priced in at a market cap of £60m? Given the exposure to licensing income and hopefully some growth in North America, I’m happy to give this one the benefit of the doubt and go AMBER/GREEN on it. The enterprise value is only £50m once we deduct cash, and the cash balance should hopefully see a nice bounce in H2. That’s not a very demanding enterprise value to my eyes, vs. underlying PBT of c. £8m in a tough year.

Property Franchise (LON:TPFG)

Up 2% to 465p (£291m) - Half Year Trading Update - Graham - GREEN

Readers will remember that a merger took place between TPFG and Belvoir in March. This means the H1 numbers (to the end of June) are going to require a little more work to understand.

At the end of May, another £20m acquisition took place as TPFG picked up The Guild of Property Professionals and the Fine & Country brand. This gives TPFG some foreign operations for the first time. It has been a busy year!

Here are the highlights from today’s H1 update, which is at least in line with expectations.:

(Like-for-like figures exclude the impact of Belvoir and the more recent acquisition.)

Revenue +3% like-for-like, or up 104% in total to £26.9m.

Management service fee (the royalty charged to franchisees) up 8% like-for-like, or up 60% in total to £12.3m.

Rental properties under management rose 2% like-for-like, but have nearly doubled in total to 152,500.

Outlook for H2: the sales agreed pipeline is up 16% like-for-like compared to a year ago, “which bodes well for H2 trading despite lead times remaining high”. The recent interest rate cut is also a positive factor.

Integration of Belvoir and Guild/Fine & Country “is progressing well with the restructuring of the senior leadership team largely completed”

Net debt: £14m after £20m was borrowed to fund the acquisition in May. It should be straightforward to pay this down.

CEO comment:

"The first half of 2024 has been transformational for our Group, building on our track record of growth and completing two significant acquisitions which has created a substantially larger group with an international presence. We are delighted with our organic revenue performance in the first half year and the contributions from each of our new businesses.

"We have a very resilient and focused franchise model and multiple income streams across 18 brands including a significantly enhanced, exciting opportunity in financial services. With an improving pipeline and at least one interest rate reduction behind us, the Board is confident that trading remains at least in line with market expectations for the full year."

Graham’s view

I’m a long-term fan of this company. I never predicted a merger with Belvoir (although I liked that company, too), but the merger seems to have helped push the share price higher year-to-date.

Indeed, the share price is up by 100p or 27% since I last reviewed this stock in April.

After being bullish for so long, we may be approaching the point where I need to temper my expectations with a downgrade to AMBER/GREEN. Perhaps not quite yet?

I always argued that TPFG deserved earnings multiples that reflected its quality and resilience. It has come a long way towards achieving that, and Stockopedia now only gives it a ValueRank of 14.

If the share price were to suddenly rush to 500p+, for example, that could be the trigger for me to downgrade my stance. This is a high-quality company and I’m excited to see what it can do if the property sales market returns to health. Its M&A activity has been truly transformational, and I applaud it. But at the end of the day I’d still be reluctant to overpay for this stock - so let’s keep an eye on this valuation.

See what our investor community has to say

Enjoying the free article? Unlock access to all subscriber comments and dive deeper into discussions from our experienced community of private investors. Don't miss out on valuable insights. Start your free trial today!

Start your free trialWe require a payment card to verify your account, but you can cancel anytime with a single click and won’t be charged.