Good morning, it's Paul here!

I don't have a lot of time available today, so apologies but won't be able to do any reader requests today.

3 companies have caught my eye, so here goes;

Future (LON:FUTR)

Share price: 346.3p (up 8.9% today)

No. shares: 45.4m

Market cap: £157.2m

Trading update - for the year ended 30 Sep 2017.

I'm not terribly familiar with this company, not having looked at it personally for over 3 years. Graham did a nice review of the latest interim results here on 19 May 2017, flagging potential value if growth continues. Well growth has continued, and the share price has risen by 68% in less than 5 months - so well done to shareholders here!

The activities of this group are publication of special interest consumer magazines, Apps, and websites. That sounds a little bit like what XLMedia (LON:XLM) do - although XLM seems focused mainly on feeding new customers to gambling websites, in return for a revenue share. I know XLM are diversifying into other areas too.

Anyway, things seem to be going well;

Overall trading for the year has been positive and it is anticipated that results for the full year will be ahead of the Board's expectations.

The Group has achieved good growth in operating profitability and has benefitted from strong cash conversion in the period, with year-end leverage less than 1x adjusted EBITDA.

The Group's Media division is performing well with fast revenue growth, particularly in eCommerce and events.

I like the sound of that - particularly the strong eCommerce revenue growth, which could drive the PE ratio higher - as we're in a market which loves online growth companies. Although I note from the last interim results that eCommerce was only 10.5% of total revenues.

Various other details are given.

Note that some growth has come from acquisitions.

Forecasts - I haven't seen any new broker updates today yet. So working on the existing Stockopedia broker consensus EPS figures, which are 15.2p for 09/2017 (which we now know will be exceeded). For 09/2018 the existing consensus is 20.5p.

Valuation - at 346p per share currently, I make the forward PER 16.9, which sounds reasonable for a growing company.

Balance sheet - as last reported this looks very weak to me. Although I see that a £22m placing at 250p per share was done in Jul 2017, to fund the bulk of a large £32m acquisition. That would still leave the balance sheet in a significantly negative NTAV position, which is a concern.

As always, the problem with acquisitive groups, is that the balance sheet usually ends up lop-sided, with massive intangibles (which are often ultimately written down to zero, when acquisitions go wrong at a later date). So there are risks associated with this type of acquisitive growth.

My opinion - this looks potentially interesting in my view, and is possibly worth a closer look. Have any readers looked into this one? I note that shrewd investor Richard Crow flagged this company as interesting recently, on Twitter. He has a good knack of spotting decent turnarounds.

I would want to get a better understanding of what went wrong in the past too, as there were a couple of years of heavy losses. It seems to have been a successful turnaround since then - so again it would be good to focus on what was wrong, and how it was fixed.

A lovely chart - but has the good news now been priced-in?

Topps Tiles (LON:TPT)

Share price: 73p (down 2.3% today)

No. shares: 192.4m

Market cap: £140.5m

Trading update - the company calls itself the UK's largest tile specialist (i.e. retailer).

This update covers the 52 weeks to 30 Sep 2017.

Like-for-likes down 2.9% for the year, but these are reported quarterly, so the trend was already known. Q4 was -3.0% LFL, which was a sequential improvement on Q3 being -4.7% LFL. Also note that the FY2016 comparatives were quite strong - making them hard to beat.

Whilst we have seen a moderate improvement in trading in our final quarter, market conditions remain challenging and the Group expects adjusted pre-tax profits for the 52 week period ended 30 September 2017 will be at the lower end of the current range of market expectations.

We already know that the consumer is being cautious at the moment, particularly on bigger ticket/household items, and that retailers are facing numerous cost headwinds. So this seems a reasonable outcome to me - it's not a disaster by any means.

Valuation - I see that one broker has trimmed its forecast for FY 9/2017 from 7.9p to 7.6p EPS. That puts the share on a PER of 9.6 - seemingly good value.

The trouble is, there is no earnings growth forecast for FY 9/2018 or FY 9/2019. So a mature business, which is struggling to stand still in terms of earnings, probably should be on a low PER.

Dividends - well worth having. The well-covered 3.5p divis are yielding 4.8% - so this share could be worth considering for an income portfolio, perhaps? I don't see any reason why that level of divi payout would not be sustainable, providing we don't encounter a more serious economic downturn.

Balance sheet - not the strongest, but a great deal improved from the very poor shape it was in a few years ago. I feel that gross debt of £40m is still a bit too high for comfort. Although deducting cash, reduces net debt to £26.6m - which looks OK.

My opinion - I have a generally favourable view of this business, as it is the sector leader in its niche, and seems to be well-managed.

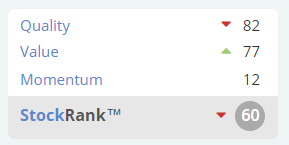

The StockRank sums things up nicely;

The quality ranking is very good, and I'm impressed with the decent operating profit margin, and strong ROCE and ROE.

Value is also ranking fairly strongly, which makes sense, given a low PER and decent dividend yield.

The big missing link at the moment is momentum - remember this score includes earnings forecast momentum, not just share price momentum (although the two often move in tandem, for obvious reasons).

I'm struggling to find any reasons why the company might begin out-performing forecasts any time soon. It seems to me that good companies in this sector are struggling to stand still whilst weaker companies are seeing profits go backwards.

Therefore, it's probably one I'll put on my watchlist, but I'm not ready to buy any yet. Ultimately though, it is a share I would like to own, once consumer confidence shows signs of returning, because it's a quality business.

We have to consider the political cycle here too. I think it's looking increasing inevitable that politicians of all sides are likely to be forced into having a splurge in public spending. Probably unwise long-term, but that would certainly be helpful in boosting demand for companies like TPT in the shorter term.

Image Scan Holdings (LON:IGE)

Share price: 10.2p (up 13.2% today)

No. shares: 135.7m

Market cap: £13.8m

(at the time of writing, I hold a long position in this share)

Trading update - this tiny company is a specialist in x-ray screening systems for security and industrial applications. It was brought to my attention after a series of recent positive trading updates. Well there's another one today! The numbers are still very small, but sales and earnings momentum really seem to be gathering pace.

It's now upped guidance for profits for y/e 30 Sep 2017 from £250k to £450k. This seems to be due delivering more orders before the year end cut-off than anticipated. There's also a strong order book, so hopefully the good momentum might continue.

Directorspeak sounds good;

Bill Mawer, Chairman and CEO of Image Scan, said: "September has been an exceptionally busy month for the Company and the response of our staff to new opportunities has been very impressive. I am also particularly pleased by the strength of the orderbook with which we start the new financial year. Demand for our new systems remains strong."

(apologies for formatting, I couldn't manage to clear the bolding)

My opinion - I wouldn't normally touch anything this small & iliquid. However, what I like here are;

- Newish management with relevant experience & good track record

- Positive results are now appearing from streamlining & refocusing the business

- Innovation - new products have been successfully developed, which are clearly meeting market demand

- Niche activities with little competition

- Earnings momentum - whilst still quite early days, we've now seen 2 or 3 consecutive earnings upgrades

- Operational gearing - so if demand continues rising, then profits could rise a lot more than people currently expect

- Poor historic track record & results. So the shares are still somewhat off the radar for most investors - possible upside if institutions start to get interested maybe? (probably too small at the moment, but in future that could be a good catalyst)

There's an excellent, recent, comprehensive review of the business from the Chairman, recorded by PIWorld available here.

I think the current share price is probably about right, but it's the long-term potential which interests me, if trading continues to improve.

I have to dash now, see you tomorrow!

Regards, Paul.

See what our investor community has to say

Enjoying the free article? Unlock access to all subscriber comments and dive deeper into discussions from our experienced community of private investors. Don't miss out on valuable insights. Start your free trial today!

Start your free trialWe require a payment card to verify your account, but you can cancel anytime with a single click and won’t be charged.