Good morning from Paul, and I hope you enjoyed the Christmas break.

Not a great deal of news today, but a couple of companies caught my eye, and also you need a place to discuss the day's news - so if the UK market is open, I'll write an SCVR.

There's also a lot of new content coming in the next few days from other writers, so I'll flag up those articles here at the top of the SCVRs, in case you miss them.

Here's a terrific article from Roland, explaining how he's set up a simple stock screen to find good small cap shares - I recognise lots of the companies in this screen as being decent small caps that we also like here in the SCVR. Highly recommended article!

Housebuilders - could benefit from press reports that the Govt is likely to introduce new incentives for first-time buyers. That's all very well, but will they be in office long enough to implement these measures, and would a new Govt repeal or support them? Who can say?!

Explanatory notes -

A quick reminder that we don’t recommend any stocks. We aim to review trading updates & results of the day and offer our opinions on them as possible candidates for further research if they interest you. Our opinions will sometimes turn out to be right, and sometimes wrong, because it's anybody's guess what direction market sentiment will take & nobody can predict the future with certainty. We are analysing the company fundamentals, not trying to predict market sentiment.

We stick to companies that have issued news on the day, with market caps (usually) between £10m and £1bn. We usually avoid the smallest, and most speculative companies, and also avoid a few specialist sectors (e.g. natural resources, pharma/biotech).

A key assumption is that readers DYOR (do your own research), and make your own investment decisions. Reader comments are welcomed - please be civil, rational, and include the company name/ticker, otherwise people won't necessarily know what company you are referring to.

What does our colour-coding mean? Will it guarantee instant, easy riches? Sadly not! Share prices move up or down for many reasons, and can often detach from the company fundamentals. So we're not making any predictions about what share prices will do.

Green (thumbs up) - means in our opinion, a company is well-financed (so low risk of dilution/insolvency), is trading well, and has a reasonably good outlook, with the shares reasonably priced. OR it's such deep value that we see a good chance of a turnaround, and think that the share price might have overshot on the downside.

Amber - means we don't have a strong view either way, and can see some positives, and some negatives. Often companies like this are good, but expensive.

Red (thumbs down) - means we see significant, or serious problems, so anyone looking at the share needs to be aware of the high risk. Sometimes risky shares can produce high returns, if they survive/recover. So again, we're not saying the share price will necessarily under-perform, we're just flagging the high risk.

WH Ireland (LON:WHI)

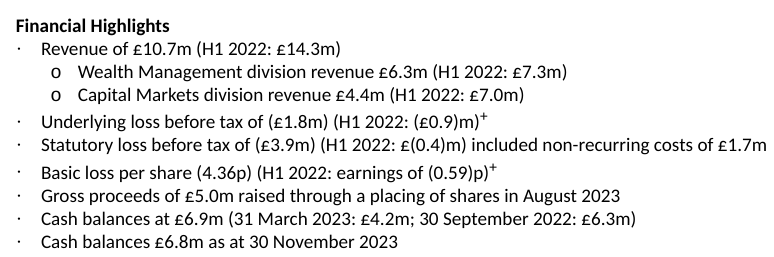

Unch 3.5p (£8m) - Interim Results (Sep 2023) - Paul - AMBER

Poor results from this small stockbroker, but note the strong cash balance relative to the market cap, after a £5m placing in the period, which greatly increased the share count -

Cost savings - WHI has made deep cuts to its cost base, £3.8m annualised, including a large reduction in head count. Therefore this should benefit future periods, providing some upside on future profitability.

The £2.1m non-recurring costs are for redundancies, and project costs.

Tentative signs of improvement is noted in the commentary on recent trading.

Balance sheet - NTAV is level with the market cap, at £8.5m. Only minor lease liabilities, so no worries here about costly empty office space obligations.

Paul’s opinion - after an equity fundraise which has repaired the balance sheet, and deep cost cuts, WHI is probably looking more interesting now than it has for years. Historically it’s never really made any reliable profits though, and arguably there are too many smaller brokers still, with some merging (eg Cavendish from Finncap and Cenkos). Does that leave any room for a minnow like WHI?

I considered having a dabble here, for a rebound as the small caps space starts to come alive again, but taking everything into account, I’d probably be more inclined to punt on Cavendish Financial (LON:CAV) instead, which has a bit more scale, and has also done deep cost-cutting in its recent merger. Graham reported positively on CAV last week.

The liquidity in shares like these is very poor most of the time.

This whole sector is bombed out, and looks ripe for recovery, I think.

Note that the share count has roughly quadrupled recently, so it's unlikely to recover to previous highs on the chart when the share count was so much smaller, so not much point in drawing lines on this particular chart!

Agronomics (LON:ANIC)

Up 3% to 9.65p (£95m) - Final Results 6/2023 - Paul - AMBER

This is my first look at Agronomics, catching my eye on a quiet news day.

I think it’s quite interesting, and might be worth some deeper research, hence why I’ve decided to flag it.

This is an investment company connected to serial entrepreneur/investor, Jim Mellon (15.5% shareholder). It invests in a portfolio of “cellular agriculture” companies, such as lab-grown meat. So this share is a way to gain exposure to a portfolio of companies in that sector, without having to pick the investments ourselves. The hope being that amongst its portfolio, there might be one or more future stars. Obviously I can’t assess the prospects of the individual companies, and probably nor can you, so it’s maybe a bit of a punt? I heard Jim Mellon give a talk about new types of agriculture a while back, and he was very convincing.

The numbers out today show a big profit, which has come from marking up the valuations of its investments. That’s the worst kind of profit, as it’s notional, and completely dependent on the method used to value investee companies. I imagine these are loss-making and cash-burning ham tomorrow (geddit?!) projects, so some of them might turn out to be worthless, and others need repeated rounds of financing.

Note that shares are valued at £95m in total, whereas NTAV is much higher at £168m, so there’s an attractive discount to (possibly questionable) NTAV.

Paul’s opinion - on the briefest of looks, I can see some merit in having a small punt on this share, to get some exposure to what could be a huge growth area in future. I would never pay a premium for this type of share, but it’s now at a potentially attractive discount, so possibly worth a deeper dive, if you have time?

Do let me know what you think, if you’re already researched it.

EDIT: Very helpful additional points made by Mojomogoz here in the comments below - thank you!

Superdry (LON:SDRY)

Press reports originated in The Telegraph I believe, behind a paywall, and picked up here by Retail Gazette, indicate that it is in talks to dispose of more international brand rights, in the Middle East, and USA. It talks of "tens of millions" of potential cash receipts.

At about 36p share price (£34m market cap), SDRY shares are little more than an option on survival/turnaround. So it's probably going to be a zero, but if a miraculous turnaround is achieved, then it could be a multibagger.

The trouble with selling off international brand rights, is that the profits from those territories are then lost, making future trading results even more difficult.

I'm told that one broker has massively reduced FY 4/2024 forecast, to about £(45)m loss. The consensus (of 2 brokers) is now £(23)m, so maybe one broker has not updated yet, from the previous c. breakeven forecast, which has turned out to be wildly over-optimistic.

Paul's view - I've been very wary of this share for a long time, and maintain my RED stance. It's just for gamblers & traders now.

See what our investor community has to say

Enjoying the free article? Unlock access to all subscriber comments and dive deeper into discussions from our experienced community of private investors. Don't miss out on valuable insights. Start your free trial today!

Start your free trialWe require a payment card to verify your account, but you can cancel anytime with a single click and won’t be charged.