Good morning from Paul & Graham!

Today's report is now finished.

Explanatory notes -

A quick reminder that we don’t recommend any stocks. We aim to review trading updates & results of the day and offer our opinions on them as possible candidates for further research if they interest you. Our opinions will sometimes turn out to be right, and sometimes wrong, because it's anybody's guess what direction market sentiment will take & nobody can predict the future with certainty. We are analysing the company fundamentals, not trying to predict market sentiment.

We stick to companies that have issued news on the day, with market caps up to about £1bn. We avoid the smallest, and most speculative companies, and also avoid a few specialist sectors (e.g. natural resources, pharma/biotech).

A key assumption is that readers DYOR (do your own research), and make your own investment decisions. Reader comments are welcomed - please be civil, rational, and include the company name/ticker, otherwise people won't necessarily know what company you are referring to.

What does our colour-coding mean? Will it guarantee instant, easy riches? Sadly not! Share prices move up or down for many reasons, and can often detach from the company fundamentals. So we're not making any predictions about what share prices will do.

Green (thumbs up) - means in our opinion, a company is well-financed (so low risk of dilution/insolvency), is trading well, and has a reasonably good outlook, with the shares reasonably priced.

Amber - means we don't have a strong view either way, and can see some positives, and some negatives. Often companies like this are good, but expensive.

Red (thumbs down) - means we see significant, or serious problems, so anyone looking at the share needs to be aware of the high risk.

Summaries of main sections

UP Global Sourcing Holdings (LON:UPGS) - up 3% yesterday to 126p (£113m) - Improved Net Debt Expectations - Graham - GREEN

This household brand owner announces net debt at year-end (July 2023) is significantly below expectations (c. £15m vs. £21m). We don’t have info on average net debt and I’m not sure the improvement has come from sustainable sources, but the stock is interesting.

Zotefoams (LON:ZTF) - up 9% to 350p (£170m) - Joint development agreement - Paul - GREEN

Encouraging news about a partnership to develop the innovative drinks cartons project, ReZorce. This is one of my top picks for 2023, so it's good to see some positive newsflow.

Luceco (LON:LUCE) - Up 4% to 121p (£194m) - H1 Trading Update - Paul - AMBER/GREEN

Quite a good H1 update, and says towards top end of range of broker forecasts for FY 12/2023. Looks a decent, owner/managed business, maybe priced about right? I like that trading seems to have settled down now, after a boom & bust caused by the pandemic. Overall - I'm moderately positive on this share.

Record (LON:REC) - down 6% to 83p (£165m) - First Quarter Trading Update - Graham - GREEN

A reversal in fortunes at this currency manager as they suffer outflows in Q1. Passive Hedging, such a strong performer last year, saw $3 billion removed. I will maintain a positive view here as it has such a long and impressive track record. Hopefully this is just a blip.

Judges Scientific (LON:JDG) - up 3% to £93.99p (£621m) - Half Year Trading Update - Graham - AMBER

Judges returns to solid organic order growth, and organic results will be boosted by Geotek plus some smaller acquisitions. It’s full steam ahead for Judges, therefore, but I would not be in a rush to buy these shares at this level. Long-term holders will be happy.

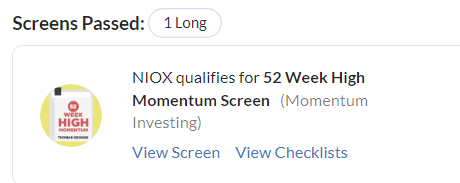

Niox (LON:NIOX) - Up 13% to 72p (£303m) - Trading Update - Paul - GREEN

My first look at this company, which makes asthma diagnosis equipment. It's moved into profit, is growing nicely, with high operational gearing from good gross margins. Looks a very interesting growth company, worth readers researching more I think.

DX (Group) (LON:DX.) - up 1% to 31.9p (£193m) - Trading Update - Paul - GREEN

A solid update, in line with expectations for FY 6/2023. It's absorbed a lot of the business and depots from failed Tuffnells, which sounds positive. We like the cheapness of this share, with a low PER, decent yield, and a decent cash pile too.

Quick Comments

Bloomsbury Publishing (LON:BMY) - up 2% to 450p (£368m) - AGM Trading Update - Paul - GREEN

In line with expectations for first 4 months of FY 2/2024, with a footnote saying this is revenue: £273m, and aPBT: £32.5m. StockReport shows 29.4p EPS, so a PER of 15.3x.

Forecasts were upgraded previously, see SCVRs 15 March, and 1 June 2023.

Paul's view - Excellent steady growth company, nice balance sheet, lots to like here. So I’ll keep my GREEN view of it. High StockRank of 87.

Revolution Beauty (LON:REVB) - up 4% to 32p (£97m) - Settlement with Boohoo - Paul - AMBER

An agreement has been reached, but it looks more like a capitulation to me! Boohoo has ousted Chairman Bob Holt, with 4 new Directors joining the Board. Who knows what's gone on behind the scenes? Someone should write a book about it.

Paul's view - I can't assess the company itself, as we need much more information on the accounts, and current trading. Boohoo seems to have almost seized control, but without bidding for it, and with a 26.5% shareholding. I bet Mike Ashley has been taking notes!

Paul’s Section:

Zotefoams (LON:ZTF)

Up 9% to 350p (£170m) - Joint development agreement - Paul - GREEN

ZTF is one of my top watchlist shares for 2023. So far it's about flat year-to-date, so nothing exciting going on as yet.

This announcement today concerns ZTF’s blue sky development project, ReZorce - which is fully recyclable one-material drinks cartons. Existing drinks cartons are not recyclable, because they are made from laminates of different materials (eg plastic, aluminium, etc).

Another key advantage is that the ReZorce product, if successful, could be used in drinks packaging factories, on the existing machines, so no special capex required for the drinks makers.

ZTF had previously indicated that it wanted to develop this project with a large scale partner, so this sounds encouraging news -

18 July 2023 - Zotefoams, a world leader in cellular materials technology, is pleased to announce a joint development agreement ("JDA") with a world-leading packer of beverages.

Following successful internal trials, this agreement encompasses the further development of Zotefoams' ReZorce® monomaterial beverage carton packaging, and its planned use in in-market trials for a major European retailer.

The JDA covers all activities, including packing at industrial scale, to trial ReZorce® cartons in the retail market and non-binding provisions for further co-operation. Zotefoams anticipates that the initial scope of work will continue until early 2024.

David Stirling, Zotefoams Group CEO, notes, "This agreement confirms the significant technical progress we have made with our ReZorce® mono-material barrier range. As we have continued our development efforts, it has become clear that demand for a sustainable alternative material for beverage cartons is significant and in line with our initial market assessment.

"This agreement for ReZorce® development is an important milestone and we look forward to it delivering results that clearly demonstrate ReZorce® is the optimal material solution for beverage cartons."

Paul’s opinion - this is encouraging news I think. The way I look at ZTF shares, it’s a decent company making specialised products at fairly good margins. The biggest customer is NIKE, which recently extended its long-term supply agreement with ZTF, so single main customer risk reduced.

The upside potential from the ReZorce project is basically in for free, and at times management have sounded very excited about its potential. However in the most recent updates I perceived that management seemed to have cooled somewhat on ReZorce, which made me wonder if they’re softening up the market for it being quietly dropped?

Hence today’s news of a new partnership should reignite interest in ReZorce.

The valuation metrics look quite good, with a fwd PER of 15.2, and it’s nicely asset backed too with a strong balance sheet. The share price is only 1.53x tangible book value, so very nice asset backing there, including the freeholds to its factories, which have recently been re-equipped with new machines. So all well invested.

At some point I need to pick up a few of these for my own portfolio. Trouble is, there’s such a long list of decent, reasonably-priced shares that I want to buy, we’re spoiled for choice at the moment. Instead of being excited at these bargains, everyone seems scared witless. It’s funny how sentiment changes!

Luceco (LON:LUCE)

Up 4% to 121p (£194m) - H1 Trading Update - Paul - AMBER/GREEN

Luceco plc ("Luceco" or "the Group"), the supplier of wiring accessories, EV chargers, LED lighting, and portable power products, is pleased to provide the following update on trading for the six months ended 30 June 2023 ("H1 2023").

Encouraging first half performance.

Full year guidance towards the upper end of market expectations.

Remain vigilant to the changing economic environment.

Main points -

H1 revenue down 5% to £101m, although it says this is ahead of expectations.

Downturn due to reduced activity in the housing RMI (repair, maintenance, and improvements) market. This is obviously the hangover after the pandemic boom.

Gross margins improved.

Customer de-stocking “appears to have ended”.

H1 profit guidance -

Adjusted Operating Profit is expected to be no less than £10.5m, ahead of our expectations.

No figures on bank debt, but covenant net debt is 1.3x (target range 1.0 - 2.0x) - this sounds OK.

Working capital increased in H1, expected to unwind in H2 - that’s OK I think, it’s normal for working capital to fluctuate, especially after all the disruption in recent years.

2 recent acquisitions “both performing well”.

Full year guidance -

Assuming demand continues at current levels and is not impacted by macro-economic headwinds, we anticipate that Adjusted Operating Profit for the full year will be towards the upper end of the range of current market expectations*.

*consensus at the 17th July 2023, full year 2023 Adjusted Operating Profit £20.3m (Analyst Range £19.2 - 21.9m)

General moan - I wish we could get some uniformity for trading updates. Different companies seem to pick whatever benchmark they like. Most report EBITDA, which many investors (including me!) dislike. I prefer adj PBT, providing the adjs are reasonable, but most companies don’t report that in trading updates. I see the latest fashion seems to be reporting adj operating profit, which of course omits finance costs (which often include a lot of lease-related costs), unhelpful in a higher interest rate environment. Hardly anybody reports the most important measure I use, which is adj EPS.

So we’re forced to go to (often unavailable) broker notes to get the figures we actually need, and of course to find out if the company has slipped out a profit warning on the sly - another infuriating, and dishonest trend we’re seeing too much of lately.

Anyway, back to LUCE. We can see from the helpful footnote above that it expects FY 12/2023 operating profit to be near to £21.9m.

Outlook - this all sounds quite encouraging -

"It is encouraging to again see our gross profit margin improving and reassuring that our order book supports a good outlook for Q3.

Material and freight cost pressures continue to ease on the whole, but wage pressures remain.

We are excited by a number of product developments which provide us with good medium and long-term opportunities for growth, particularly within the EV business.

We continue to build an attractive M&A pipeline.

Historically the Group has enjoyed a stronger second half and, whilst we are mindful of the current economic environment, we expect a similar profile again this year."

Broker update - many thanks to Liberum for an update on the numbers. It highlights the importance of improving gross margin, as cost & freight pressures ease.

FY 12/2023 forecast EPS is now 9.3p (prev. 8.9p).

That gives a current year PER of 13.0x, which looks about right to me.

Thanks also to the Liberum analyst Charlie Campbell, who includes some interesting macro charts in the Luceco notes.

Paul’s opinion - it looks as if things have settled down now, with the boom & bust cycle having played out now.

The aggressive selling (in other sectors) direct into the UK by Chinese websites SHEIN and TEMU has unnerved me. So I’m generally avoiding all companies which just get stuff made in China, then sell it in the UK, because these could all be vulnerable to new, well-funded, and aggressively price-cutting direct competition from Chinese companies. So we need to be asking what defensible moats do companies like LUCE really have? Established, trusted brand names would be one potential moat for LUCE (also the same for UPGS).

The chart for LUCE seems to have found a floor over the last year, and maybe it can now start a fresh bull run at some stage? The valuation looks reasonable, and the newsflow today looks quite good.

There’s a nice StockRank of 94.

Owner/manager John Hornby has a healthy 18% stake. It looks like a private equity firm, Epic Investments, owns 22% - so maybe some delisting risk, given the top 2 hold 40%?

Pulling all this together, I think LUCE looks quite good. There’s a lot less guesswork needed now, than there was last year.

So I’ll give it a cautious thumbs up, so AMBER/GREEN.

I would ignore the pandemic boom share price movement, it's now reset back down to a more sensible level. So we need to avoid anchoring to the unrealistic spike in price that happened in 2020-21.

Niox (LON:NIOX)

Up 13% to 72p (£303m) - Trading Update - Paul - GREEN

Oxford, UK - 18 July 2023: NIOX Group plc (AIM: NIOX), a company engaged in the design, development and commercialisation of medical devices for asthma diagnosis and management, today announces a trading update for the six months ended 30 June 2023 ("H1 2023").

I’ve not looked at this company before, as medical devices is not a sector I have experience investing in. The early stage companies nearly always disappoint, but I can see a good case for investigating potential investments where a successful product is being commercially rolled out, which seems to be happening at NIOX.

Renowned fund manager Christopher Mills mentioned NIOX in his brilliant talk last night on Mello Monday (watch the recording if you missed it, this was quality stuff, from a man with a 40+ year superb track record at North Atlantic Smaller Companies Investment Trust (LON:NAS) - he reckons it’s 150-bagged in the time he’s been running it!)

There’s been a positive up 13% share price reaction to today’s trading update from NIOX, and this chart is signalling to us that something positive is going on - especially as this 1-year period has been a deep bear market for smaller caps, so this is a major out-performer -

Background - I’ve found a terrific article here from Jan 2022, which Jack Brumby wrote in the SCVR, detailing this company when it was called Circassia. Old management failed, and were replaced with new more commercial management, focusing on its most promising asthma diagnostics product called NIOX, hence the company name change.

Massive losses from 2017-2020 now seem to have been turned around into profit.

A special dividend of 2.5p was announced in June 2023 - looks a one-off.

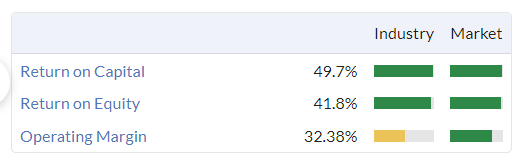

Results for FY 12/2022 were boosted by £8.1m from a settlement with “Beyond Air” for a success fee, giving a total PBT of £10.5m, on revenues of £31m. The cash pile was £19.4m at Dec 2022. Strong recurring revenue. Gross margin of 71% gives excellent operational gearing as sales increase. Good balance sheet.

Latest news - today it says -

H1 revenue up 22% to £18.8m

Singers (many thanks!) estimates £37.9m revenues for FY 12/2023.

Adj EBITDA in H1 almost doubled to £6.2m.

Singers say £11.7m EBITDA for FY 12/2023, which is mostly real profit, as adj PBT forecast is £9.3m.

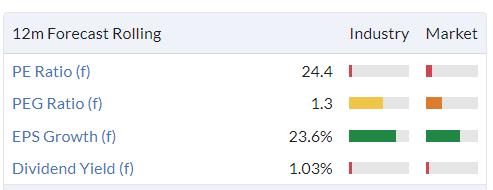

Forecast EPS for FY 12/2023 is 2.1p, so the PER is 34x - maybe justified, given the growth potential, and the operational gearing?

Net cash at June 2023 was £23.8m, but the special divi will make a £10.5m dent in this, when paid in Sept 2023.

I like this bit -

The Group is now generating sufficient operating cashflow to permit both continued investment in the development of its business and the payment of ongoing dividends to shareholders.

And this is good too! -

Ian Johnson, NIOX's Executive Chairman, said: "I am pleased to report continued growth in revenues and profits in the first half of the current financial year. It is particularly satisfying to describe the strong growth in our core Clinical business, which continues to benefit from a high degree of recurring revenues.

We indicated at the time of our AGM in May that adjusted EBITDA1 would be significantly higher than management expectations at the start of the year. After two further full months of strong trading, particularly in the APAC region, management's expectations for the year end outturn have been subject to further material upgrade.

The Company is now in a strong financial position and with positive momentum in the business. I look forward to updating shareholders again at the time of the half-year results."

Paul’s opinion - definitely not my area of expertise, but from what I’ve seen, this share looks attractive, and definitely worthy of further research. The hope is obviously that global sales of the product could really take off. With such high gross margins, that could be very exciting. Yet we can still value the company on traditional metrics like PER, and it’s paying divis too.

Plenty to like here! How to value it, no idea, but personally I’d be happy to have a punt on this. Vastly better than all the speculative rubbish we usually see in this sector, this is a proper company, making lovely margins, and generating cash. Is it worth £303m? I think that can be justified, providing growth continues. It’s about 20x Singers forecast for 2025, which I don’t have a problem with. An initial thumbs up from me I think, although as a credible growth company, not a value share. That’s based purely on a quick desktop review, not in depth research remember - that’s your job! ;-)

I see NIOX qualifies for the new 52-week highs screen - so let's have a look at this, and see what the other big winners are. There's a lot to be said for screening for out-performing shares, as winners often carry on winning. Or, they can be over-priced speculative bubbles! So sorting the wheat from the chaff may not be easy -

(picture is clickable link)

DX (Group) (LON:DX.)

Up 1% to 31.9p (£193m) - Trading Update - Paul - GREEN

DX, the provider of delivery solutions, including parcel freight, secure courier and logistics services, is pleased to provide an update on trading for the second half of the Group's financial year ended 1 July 2023.

We flagged the good turnaround, and cheap value metrics of this delivery company in the SCVRs on 15 Dec 2022, and 1 Feb 2023, with a GREEN opinion in both reports.

So what’s the latest?

Trading has been in line with management expectations for FY 6/2023.

Revenue up 10% to £470m.

Net cash rose 39% in the year, reaching £38m (20% of the market cap)

Targeting further improvements in operating margin.

“Major development” has been taking on 15 of insolvent Tuffnells depots, with £35m pa of customer work added so far (not clear what period this covers, or what it would be if annualised?)

Outlook sounds positive -

Despite the current economic headwinds, the Board remains encouraged about growth prospects for the Group, and the recent additional volumes secured should enhance profitability in the new financial year and beyond.

Paul’s opinion - it sounds as if DX has been a beneficiary of Tuffnells demise. Maybe that could drive broker upgrades?

I’m still not clear how much of the group’s profit comes from its specialist network for lawyers, which has been shrinking due to email substitution.

This is not the sort of business I would want to invest in, against lots of competition, and maybe the old legal business is a cigar butt that could expire at some stage, I’m not sure?

Finncap (many thanks) has edged up forecast EPS by 2% today. It’s now saying 3.8p FY 6/2023, and 4.3p FY 6/2024. So a PER of 7.4x looks good value, considering it also has a nice balance sheet with plenty of cash. Thumbs up from me again, more on cheapness than quality! The c.5% yield helps too.

So far it's been a good turnaround from previously quite serious problems -

Graham’s Section:

UP Global Sourcing Holdings (LON:UPGS)

Share price: 126p (+3% yesterday)

Market cap: £113m

This company owns a range of household brands, and you may already be familiar with several of them. Of the brands managed on its website, be careful to remember that the one it doesn’t own is Russell Hobbs - but it does have a licence to use that trademark.

Yesterday the company announced that it expects its financial net debt at year-end (July) to be “in the region of £15m, which is significantly ahead of current market expectations of around £21m”.

For some context, net debt was £19m at the end of H1 (January 2023) and £24m at the end of the previous financial year (July 2022).

The company’s debt is made up of the following: overdraft, term loan, RCF, invoice discounting, and import loans. In their own words:

The Group makes use of term loans for longer term funding, such as acquisitions, whereas our invoice discounting and import loan facilities are designed to fund our working capital, and automatically increase in relation to our levels of trading.

So what was the reason for the £6m reduction in net debt? After all, a reduction in trading activity could reduce the company’s debt level. As I’ve said before, there are some companies where I like to see debt rising, because it means the company is very busy!

The reason given at UPGS is: ongoing improvements in working capital management and the phasing of trading during the second half of the year.

“Working capital management” - to me, this typically means one of two things. Either the company has managed to convert receivables into cash faster than expected, or it has managed to stretch out its payables (paying its suppliers later than expected). There are other possibilities but these are the most likely. It’s good news, of course - it’s not the same thing as higher profits exactly, and it might end up reversing at some point, but it’s certainly good news.

“The phasing of trading during the second half of the year” - this is more nebulous to me. But if the company is talking about how the timing of orders over a six-month period has boosted its cash balance, then I would expect any reduction in net debt arising from this to be temporary. The company has a history of seasonality.

I see no changes to sales or profit forecasts arising from this RNS.

Graham’s view - I would treat this RNS carefully, as it’s not clear to me that the surprise reduction in net debt is coming from sustainable sources. I suspect that it’s coming from a mix of sources, some of which are permanent and some of which will reverse in future periods. It would be more helpful if companies such as this provided transparency around average monthly net debt, and indicated the highs and lows it reached.

The big picture here is that the stock does look interesting in terms of its overall financial metrics - on a PER of 8x and a yield of 6%, with a good track record of profitability. By all accounts they have dealt very well with the challenges posed by Covid and subsequent economic difficulties. UPGS has a StockRank of 96 and therefore while I haven’t studied it in depth on the back of this RNS, I will give it the thumbs up on the basis that it’s worthy of deeper research.

Record (LON:REC)

Share price: 83p (-6%)

Market cap: £165m

Record plc ("Record" or the "Company"), the specialist currency and asset manager, is pleased to announce its trading update for the three months ended 30 June 2023 ("Q1-2024").

This share took off after I no longer owned it (shouldn’t complain, though - I have had many graceful exits from shares which subsequently did badly!).

Here’s the Q1 news:

Performance fees of £0.5m earned.

AUME (“assets under management equivalent”) $86.4 billion, down 2% since the end of the previous financial year.

Performance fees come and go; in FY March 2023, the company earned £5.8m, but they only earned £0.5 in the entire financial year before that.

CEO comment:

"Notwithstanding the challenging macro-economic backdrop, we expect the business to achieve a number of important milestones in FY-24, and look forward to the rest of the year with optimism."

Net flows for the quarter are negative to the tune of $2.5 billion. This is poor considering that flows were positive $9.1 billion in the previous financial year.

The outflows are concentrated in the Passive Hedging product. This activity has seen steady fee compression over many years but in the most recent full-year results statement, Record claimed that this fee compression had levelled out and that new types of clients (asset managers) were using it. Last year, Passive Hedging saw inflows of nearly $5 billion.

Fee rates are “broadly unchanged”.

Graham’s view

I note that Record shares are off by nearly 6% today, and this may be a fair reaction to a turn in the fortunes of the company.

The CEO mentions a “challenging macro-economic backdrop”, which is understandable, but I’d like to think that Record sees opportunities in difficult economic circumstances - the need for currency advice and currency management should remain strong in these times. Or as Neil Record himself said in June:

Record is not immune from these [economic] challenges, but structurally we are positioned to be nimble and adaptable to client demand as it develops and changes. While cost pressures (particularly labour costs) will undoubtedly impact the business, the current pace of growth and change should allow the revenue to grow sufficiently to more than compensate for the cost-base growth.

I will maintain a positive view on these shares as I think it’s reasonable to treat a disappointing quarterly update as a “blip” in an otherwise good business. This company has never reported an annual loss. And here are its most recent quality metrics:

Judges Scientific (LON:JDG)

Share price: £93.99 (+3%)

Market cap: £621m

Judges Scientific (AIM: JDG), the group focused on acquiring and developing companies in the scientific instrument sector, provides the following update regarding the Group's trading performance for the six-month period ended 30 June 2023.

This is a pleasant update: there have been “generally favourable markets” and “moderate progress in dealing with supply chain challenges, thus allowing the delivery of solid growth in both Organic order intake and Organic sales”.

Key points:

Organic order intake up 14% vs. last year, up 23% vs. 2019 (pre-Covid). It’s helpful to show both due to variability introduced by Covid, though remember that inflation has been significant since 2019.

Order book reaches a mid-year record of 22.4 weeks.

Organic revenue up 17% vs. last year. Total sales will be up significantly more due to the contribution of Geotek.

Outlook is in line with expectations:

The strong order book, and the general resilience of Judges' business give the board confidence that the current market expectations for the full year will be met.

Organic revenue growth is producing “double digit profit growth, albeit at a slower rate than revenue growth as measures taken to compensate for the inflationary pressures observed in 2022 Q4 are progressively having an impact”.

Graham’s view

Not much has changed here, so there is no need to change your prior view on Judges. I am impressed by the return to strong organic order growth, so it’s tempting to take a more bullish stance on the shares. But the price tag remains very heavy: price to book is 11x, and price to sales is 5x.

It’s a truly great success story, but there are times when the price excites me and times when it doesn’t. This is one of the times when it doesn’t excite me now, so I’ll stay neutral.

See what our investor community has to say

Enjoying the free article? Unlock access to all subscriber comments and dive deeper into discussions from our experienced community of private investors. Don't miss out on valuable insights. Start your free trial today!

Start your free trialWe require a payment card to verify your account, but you can cancel anytime with a single click and won’t be charged.