Good morning from Paul & Graham!

A fairly uneventful budget yesterday, with all the main points already leaked to the media, as usual. Here's my brief summary -

Main measure, as expected another 2% cut in employee NI.

OBR forecast growth increased & expect inflation to fall to 2% target soon.

Plan for productivity gains in NHS & other public services.

Fuel & alcohol duties frozen again, as expected.

New British ISA - extra £5k allowance for investing in UK companies.

Non-dom being abolished, new regime for 4 years not 15.

As mentioned frequently in my podcasts, I think the macro outlook for the UK economy is now looking favourable, which I think should be bullish for equities. In particular, with inflation heading for 2%, and many households receiving 8-10% pay rises from April, plus another 2% NI cut, we could go from famine to feast. So I'm expecting the consumer to come roaring back this year, hence lots of opportunities for us to make money I think. Let's hope I'm right!

EDIT: I should have mentioned that others have commented the freezing of personal allowances for years means that the Govt is giving with one hand, and taking away with the other - a valid criticism. Increasing numbers of people are getting sucked into the 40% tax band for income tax. I feel the jump from 20% to 40% is far too great. Surely it would be more sensible to protect incentives to earn more if we had a 30% intermediate band? Some other countries have many more income tax bands, so that increases are much more gradual as salaries rise. There are also wild anomalies around £100k gross income, which deter people earning above that level, due to tapering of the personal allowance creating a c.60% marginal income tax rate. If you were to design a taxation system from scratch, you definitely wouldn't come up with anything like the system we currently have!

Keelan's thread on the budget is here, if you haven't already seen it.

Explanatory notes -

A quick reminder that we don’t recommend any stocks. We aim to review trading updates & results of the day and offer our opinions on them as possible candidates for further research if they interest you. Our opinions will sometimes turn out to be right, and sometimes wrong, because it's anybody's guess what direction market sentiment will take & nobody can predict the future with certainty. We are analysing the company fundamentals, not trying to predict market sentiment.

We stick to companies that have issued news on the day, with market caps (usually) between £10m and £1bn. We usually avoid the smallest, and most speculative companies, and also avoid a few specialist sectors (e.g. natural resources, pharma/biotech).

A key assumption is that readers DYOR (do your own research), and make your own investment decisions. Reader comments are welcomed - please be civil, rational, and include the company name/ticker, otherwise people won't necessarily know what company you are referring to.

What does our colour-coding mean? Will it guarantee instant, easy riches? Sadly not! Share prices move up or down for many reasons, and can often detach from the company fundamentals. So we're not making any predictions about what share prices will do.

Green (thumbs up) - means in our opinion, a company is well-financed (so low risk of dilution/insolvency), is trading well, and has a reasonably good outlook, with the shares reasonably priced. OR it's such deep value that we see a good chance of a turnaround, and think that the share price might have overshot on the downside.

Amber - means we don't have a strong view either way, and can see some positives, and some negatives. Often companies like this are good, but expensive.

Red (thumbs down) - means we see significant, or serious problems, so anyone looking at the share needs to be aware of the high risk. Sometimes risky shares can produce high returns, if they survive/recover. So again, we're not saying the share price will necessarily under-perform, we're just flagging the high risk.

Links:

Paul & Graham's 2024 share ideas - live price-tracking spreadsheet (2 separate tabs at bottom),

Paul's 2023 share ideas, with live prices.

New SCVR summary spreadsheet from July 2023 to date, updated at weekends (very useful quick reference tool, search for ticker using CTRL+F). Hover over cell for pop-up notes.

Frozen SCVR summary spreadsheet for calendar 2023.

Paul's podcasts (weekly summary of SCVRs & macro views) - or search on any podcast provider for "Paul Scott small caps" - eg Apple, Spotify.

Other mid-morning movers (with news)

Rentokil Initial (LON:RTO) - up 15% to 495p (£12.6bn) - PAUL

Unusual to see a larger cap responding so well to Final Results figures & outlook. I’m surprised at how weak (or efficient?!) balance sheet is, with NTAV negative £(3)bn, and lots of debt. Adj PBT up 44% to £766m, but adj EPS only up 9% to 23.1p, due to dilution (shares in issue up from 2002m to 2516m in the year) - presumably for big acquisition of Terminix - going well with better cost synergies than originally planned. Outlook sounds confident for 2024.

Darktrace (LON:DARK) - up 15% to 403p (£2.84bn) - PAUL

Calls itself a “global leader in cyber security AI” - Interim Results well received today. Increases revenue (slightly) & margin expectations for FY 6/2024. H1 EBIT $46m vs £0.6m H1 LY! Negative tax charge on P&L looks odd. Balance sheet $252m NTAV. Big cash pile of $383m mainly comes from up-front customer payments, deferred revenue creditor totalling $317m. “Capitalised commission” on balance sheet of $41.8m + $43.2m is unusual. Cashflow statement - cash generated mainly used for share buybacks. Paul’s view - neutral, as I don’t know enough about the company. Large rise in profits, and raised guidance does look impressive though.

Summaries of main sections

Kier (LON:KIE) - up 2% to 139p (£619m) - Interim Results - Paul - AMBER

H1 results look as expected, and FY 6/2024 outlook remains in line (note that forecasts have been slightly reduced in the last 9 months). Balance sheet is large, complicated, and weak. Shares have had a great run, but look up with events to me, for a low quality, low margin contracting business. So I'm less keen that previously, and reduce my view to neutral - AMBER.

Tyman (LON:TYMN) - down 4% to 283p (£554m) - Final Results - Graham - AMBER

This supplier of products to the construction industry reports profits in line with expectations, but I think revenues have fallen short. Looking ahead, 2024 is expected to be another challenging year. Rate cuts might spur demand in North America. I’m neutral on this one.

TT electronics (LON:TTG) - up 5% to 146.7p (£260m) - Full Year Results - Graham - GREEN

These are decent results from a stock I’ve been bullish on. Financial net debt has reduced to £105m; perhaps the amount of leverage reduction I was hoping for was unrealistic. Another £20m of disposals have since been announced. I remain of the view that this stock is cheap.

Paul’s Section:

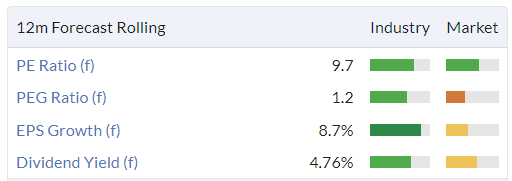

Kier (LON:KIE)

2% to 139p (£619m) - Interim Results - Paul - AMBER

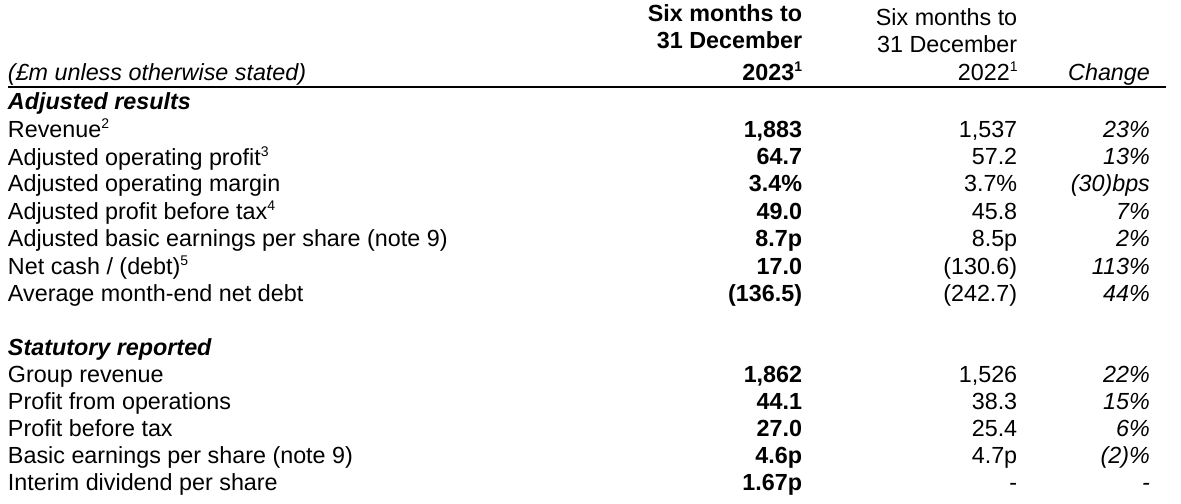

Kier Group plc ("Kier", the "Company" or the "Group"), a leading UK infrastructure services, construction and property group, announces its results for the six months ended 31 December 2023 ("HY24" or the "period").

I’m starting with a favourable impression of Kier’s performance. Previously, I reviewed its AGM update here on 16/11/2023 - trading well, positive outlook, cheap at 104p, forecast 5% yield, GREEN.

On 19/11/2024 here I reviewed an in line trading update, moderating my view to AMBER/GREEN mainly due to the share price having risen to 125p. Also noting the weak balance sheet and low margins.

That sets the scene, on to today’s H1 figures - as you can see from the highlights table below, the very low PBT margin of only 2.6% is a reminder of why many investors avoid contracting groups with big, complicated projects that can easily go wrong, but no financial buffer to absorb problems given they win business through price (competitive tenders) -

Also note a massive reduction in net bank debt (reported excl. leases), and the excellent additional disclosure of average month-end debt. Average daily net debt would be even better, but we’re not told that. Clearly this is a big business, with considerable working capital swings, so extra caution is needed when interpreting the cash/debt numbers, as they clearly fluctuate very considerably.

The net cash of £17m above looks an unusual peak, but the average month-end debt still shows a very considerable reduction in net debt.

Huge order book, up 6% to £10.7bn.

Strong visibility, with 97% of FY 6/2024 revenue secured.

Dividends have resumed, as expected, with 1.67p interim divi declared.

Financing sounds good -

Successful refinancing post period-end providing long-term debt facilities and a strengthened maturity profile

Outlook - in line -

The second half of the financial year has started well, and we are trading in-line with expectations. The Group is well positioned to continue benefiting from UK Government infrastructure spending commitments and we are confident in sustaining the strong cash generation achieved over the last 18 months, allowing us to continue to significantly deleverage the Group. We remain committed to delivering our medium-term value creation plan which will benefit all stakeholders."

Valuation - no broker notes are available right now. Stockopedia has consensus of 19.9p (PER of 7.0x), and note that forecasts have been in a gentle decline -

Balance sheet - I’ve previously described as large, and complicated, which it remains. Writing off intangible assets gives negative NTAV of £(129)m. Gross debt strikes me as too high, and I note in the commentary it talks about deleveraging being part of the strategy.

Note that it has a pension deficit (costing £5m pa in cashflows) yet shows a pension scheme asset on the balance sheet of £125m - a reminder of how absurd pension scheme accounting rules are!

This bit is reassuring on the pension schemes, which looks a manageable, and declining problem -

In FY23, the Group agreed the triennial valuation for funding six of its seven defined benefit pension schemes. Given the Group's improved covenant and payments made under the existing schedule of contributions, the schemes are in a significantly improved position. Accordingly, deficit payments will decrease from £10m in FY23 to £9m in FY24, £8m in FY25, £5m in FY26, £4m in FY27 and £1m in FY28. Once the pension schemes are in actuarial surplus, they will cover their own administration expenses. In FY23, expenses amounted to £2.9m. The largest of the six schemes is already in surplus.

At the very least though, I would remove the £125m pension scheme asset from the balance sheet, which roughly doubles the negative NTAV to £(254)m - a poor overall position in my view. So balance sheet weakness is definitely an issue here - which could become a crisis if some major contracts go wrong in future, which tends to happen sooner or later with most big contracting businesses.

Paul’s opinion - KIE shares have been really good over the last year, and it’s established a nice up-trend -

However, I can’t get excited about the valuation - why pay more than a PER of 7.0x for a low quality, low margin contracting business with a weak balance sheet?

I suspect the best part of this current bull run might now have already happened. It probably needed an ahead of expectations update to move it meaningfully higher, which hasn’t been forthcoming -a actually forecasts have been gently eased down in the last 9 months.

Overall then, I’ll ease back on the throttle to AMBER.

Graham's Section

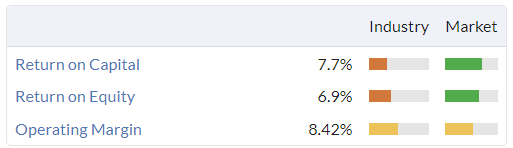

Tyman (LON:TYMN)

- Share price: 283p (-4%)

- Market cap: £554m

Tyman is “a leading international supplier of engineered fenestration components and access solutions to the construction industry.”

Products supplied by the company include window and door hardware, window and door seals, niche products such as roof doors, and various related products (see more here).

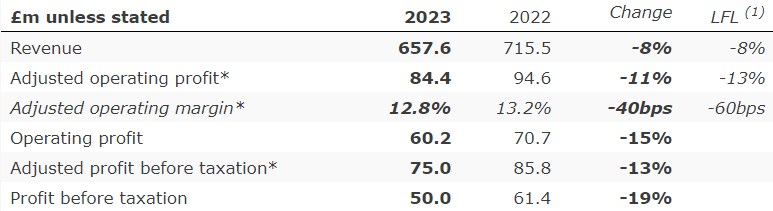

Performance for 2023 is described as “robust”, and profits are in line with expectations.

However, the numbers don’t seem terribly robust at first glance, and revenues have fallen short of the figure indicated on the StockReport (£668m):

Everything has moved in the wrong direction, with signs of operating leverage working in reverse as profit figures shrink faster than revenues.

Explanation of performance? Weakness is due to “the impact of a significant reduction in volumes due to underlying demand softness and customer destocking, which more than offset the benefit from the carryover of pricing actions and share gains”.

Acquisition: in July 2023, Tyman made an acquisition in America for an initial cost of £44m ($57m). This deal was said to be “immediately earnings enhancing”, i.e. it will have boosted H2.

This is reflected in adjusted operating profits being down 11% in total (including the effect of the acquisition), but down 13% on a like-for-like basis.

Dividend is unchanged, “reflecting confidence in the Group’s future growth prospects”.

The yield at the current level isn’t to be sniffed at:

CEO comments: the company changed CEO on 2nd January 2024, so we get two CEO comments for the price of one.

The outgoing CEO says Tyman is “well-positioned to take advantage of the positive structural growth drivers when the housing market backdrop improves”.

The new CEO says:

The structural growth drivers for the Group remain attractive, although leading indicators for our major markets are currently signalling a challenging market outlook for 2024. However, given our self-help measures and a full-year contribution from Lawrence, the Board expects the Group to make progress in 2024."

“Make progress” is nebulous, but maybe it’s difficult to make predictions with any confidence at this early stage in the year?

The StockReport suggests revenues will grow to £688m in 2024. This could be overly ambitious, seeing as the 2023 forecast wasn’t met.

Geographic split - the majority of Tyman’s profits are in North America, and in that geography, adj. operating profit only fell by 5% (vs. a 17% fall in the UK and Ireland, and 31% fall in the “International Division”.

Therefore, the outlook for the North American market is worth focusing on:

The underlying fundamentals of the US housing market remain strong, with years of supply lagging demand creating a significant housing deficit. Economists are forecasting that the easing in inflation that began in 2023 will lead to interest rate reductions in the first half of 2024, which could alleviate the recent constraints on market demand and stimulate activity later in the year. The NAHB currently forecasts a 5.5% increase in single family housing starts, whilst LIRA (GN note: the Leading Indicator of Remodeling Activity) projects that the spend on repair and remodelling will decline by mid to high single digits.

In summary: there should be a bounce in building activity, assuming that interest rates start to fall, but RMI (repair, maintenance and improvement) of existing homes is expected to continue falling.

The outlooks for both the UK/Ireland and International markets are worse, with declines expected in both, but Tyman will try to gain market share.

Adjusting items of £10.6m include nearly £7m of “restructuring costs” and £1.3m of “CEO transition costs”.

Many different types of costs have been lumped into the restructuring category, and I note that there was over £6m of restructuring costs last year, too. I would therefore not treat these costs as exceptional. I’d also be reluctant to treat the CEO transition costs as exceptional - changing CEO is not exactly a rare and unusual event.

Net debt finished the year at £110m. Fortunately it seems that the company should be able to handle this amount of debt: the leverage multiple was only 1.1x for 2023, with interest cover of 13x.

Graham’s view

I don’t remember spending much time studying Tyman before, but my overall impressions this morning are positive. This looks to be a solid international business, apparently having 3,600 employees in 15 countries. It consistently earns a profit and pays a dividend, is modestly leveraged, and seems to take a thoughtful approach to the economic challenges it faces, such as input cost variability and volatile demand.

Against that, I don’t know if I’ve seen enough to get me too excited for the prospects here. Quality metrics, for example:

The level of adjustments to earnings is another factor to consider: there’s a really large gap between £84m of “adjusted” operating profit and the £60m of what I call the “actual” operating profit. The difference is made up of the adjusting items mentioned above, plus £13.6m of amortisation.

It’s not an unusual way to present results, but I much prefer when accounts are presented cleanly.

On balance, I’m going to take a neutral stance on Tyman. Paul has been slightly more positive on it - see his November coverage here.

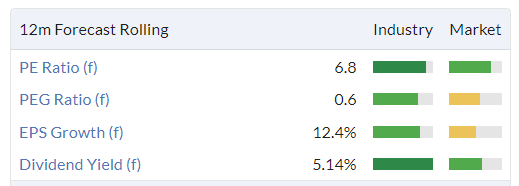

TT electronics (LON:TTG)

Share price: 146.7p (+5%)

Market cap: £260m

TTG is “a global provider of engineered electronics for performance critical applications”.

I’ve been looking forward to this report:

Strong profit growth, margin enhancement and cash generation

Adjusted results:

Revenue £614m (up 1% at constant FX)

Operating profit £53m (up 16% at constant FX)

PBT £43m (up 11% at constant FX)

Return on invested capital 12% (up from 10.5%)

Statutory results:

Operating profit £8.7m (2022: operating loss £3.4m)

Pre-tax loss £1.1m (2022: pre-tax loss £10.1m)

Unfortunately this is another case of large adjustments.

In 2022, TTG used £50m of adjustments.

For 2023, it has used £44m of adjustments, so not much improvement.

However, investors might take some comfort from the fact that in both years, large amounts of the adjustments relate to non-cash write downs.

The write downs relate to the disposals announced by TTG a few days ago, which we commented on here. The assets are being sold for less than their balance sheet values, thereby requiring the company to take a hit to its P&L.

The disposals made good sense to me, from the point of view of deleveraging and selling businesses that weren’t helping TTG’s financial performance, and I won’t change my stance on this because of the resulting write-downs.

Taking a broader look at the adjustments, I don’t think I would adjust out certain items, such as “restructuring” (£2m) or “pension restructuring” (£2m). So I do think that TTG’s adjusted operating profit figure of £53m, allowing all of these adjustments, is too optimistic.

On the other hand, the £8.7m statutory figure is probably far too pessimistic, as it includes £32.5m of write-downs which I am glad the company is taking (instead of continuing to hold businesses that weren’t performing well enough).

The truth, as always, lies somewhere in the middle.

Net debt excluding leases falls from £115m down to £105m year-on-year.

Including leases, net debt falls from £138m down to £126m.

Perhaps naively, I was hoping for better than this. After all, the company generated an adjusted PBT of £43m. This translated to £24m of free cash flow and then after £11m of dividends, the net debt reduction was only £10m-£12m.

The year-end leverage multiple was 1.7x (previous year: 2.0x), within the target range of 1-2x. The CEO report says:

We are confident this downward trajectory will continue as EBITDA increases and as we deliver further strong free cash flow in 2024.

The disposals were announced after year-end. Perhaps net debt excluding leases is now approaching £80m? That would be getting into territory where just one more year of good free cash flow performance could bring it rapidly down to the bottom of the target range.

The Board seems to be confident at any rate, as the full-year dividend has grown by 8%.

This is another stock that offers a useful yield:

Outlook excerpt:

There is considerable opportunity to unlock further value in the business by strengthening operational execution, expanding and optimising our routes to market and by enhancing product innovation. A first step in driving improved margins and simplifying the portfolio is the recently announced sale of our businesses in Cardiff, Hartlepool and Dongguan.

Based on the strength and level of visibility in our order book, current end market activity and operational improvement initiatives that are underway, while mindful of the wider macro environment, we are confident we are on track to deliver a 10% operating margin in 2024.

Adjusted operating margin was 8.6% in 2023 and 7.6% in 2022, so 10% would be a considerable improvement.

Nine months of 2024 revenues are already in the order book, implying good visibility (and it’s above pre-Covid visibility).

Graham’s view

Again I’m a little disappointed that we couldn’t get a cleaner set of accounts from TTG, but I think it makes sense to retain my positive stance on these shares.

The leverage multiple is at a reasonable level, far below the 3x number where lenders (and I) typically start to worry about financial distress.

Free cash flow performance was ok, but the cash position has been boosted since by the disposals.

In summary, I still think the market is pricing this one too cheaply at a modest single-digit earnings multiple.

Could 2024 be the year that we finally see a really big cash flow performance, clean accounts, and a reduction in the debt load down towards a leverage multiple of 1x? The closer we get to that level, the more ambitious the company could be, either in terms of growth or rewarding its shareholders.

In my view, based on the financials, there is a good case that TTG should be buying back its own shares at the current valuation. It might be difficult to convince shareholders of the merits of this, but think of it this way: if the company ploughed its entire free cash flow for 2023 into share repurchases, instead of paying down debt or paying dividends, it would reduce the share count by nearly 10% at the current share price.

That would be too aggressive - it’s good that TTG is paying down its debts - but I do think that some buybacks could make sense here, maybe instead of increasing dividends?

Either way, I’ll keep my positive stance on this stock.

See what our investor community has to say

Enjoying the free article? Unlock access to all subscriber comments and dive deeper into discussions from our experienced community of private investors. Don't miss out on valuable insights. Start your free trial today!

Start your free trialWe require a payment card to verify your account, but you can cancel anytime with a single click and won’t be charged.