Good morning, it's Paul & Graham here today.

Podcast and my SCVR summary spreadsheet were both updated this weekend, so we start the week up-to-date!

Stelrad (LON:SRAD) - many thanks to all the readers who responded to my question last week about how the supply of radiators would be affected by a move towards heat pumps. It sounds as if it might even be positive for Stelrad (a manufacturer & distributor) of steel radiators, if people need to fit larger radiators in future. That's dealt with one of my concerns. The issue over high bank debt remains though. As I mentioned in the weekend podcast, a lot of housebuilding, and building supplies shares are now looking cheap, but there's mounting evidence from their trading updates that macro factors have pushed back any recovery into 2024, and another wave of forecast downgrades looks likely. Hence I'm currently wary of both sectors - it feels too early to be bottom fishing, now that an H2 2023 recovery seems to have gone for a burton (thanks to our friends at the central banks).

Explanatory notes -

A quick reminder that we don’t recommend any stocks. We aim to review trading updates & results of the day and offer our opinions on them as possible candidates for further research if they interest you. Our opinions will sometimes turn out to be right, and sometimes wrong, because it's anybody's guess what direction market sentiment will take & nobody can predict the future with certainty. We are analysing the company fundamentals, not trying to predict market sentiment.

We stick to companies that have issued news on the day, with market caps up to about £1bn. We avoid the smallest, and most speculative companies, and also avoid a few specialist sectors (e.g. natural resources, pharma/biotech).

A key assumption is that readers DYOR (do your own research), and make your own investment decisions. Reader comments are welcomed - please be civil, rational, and include the company name/ticker, otherwise people won't necessarily know what company you are referring to.

What does our colour-coding mean? Will it guarantee instant, easy riches? Sadly not! Share prices move up or down for many reasons, and can often detach from the company fundamentals. So we're not making any predictions about what share prices will do.

Green (thumbs up) - means in our opinion, a company is well-financed (so low risk of dilution/insolvency), is trading well, and has a reasonably good outlook, with the shares reasonably priced.

Amber - means we don't have a strong view either way, and can see some positives, and some negatives. Often companies like this are good, but expensive.

Red (thumbs down) - means we see significant, or serious problems, so anyone looking at the share needs to be aware of the high risk.

Summaries of main sections below

Robert Walters (LON:RWA) - 383p (£280m) - H1 Results - Paul - AMBER

H1 results came out on 1 August. I'm taken aback by the 70% fall in H1 PBT, which seems to be due to an ill-timed increase in overheads. With FY forecasts substantially reduced, I'm questioning whether this company is as good as I previously thought? Positives include generous divis, buybacks, and a strong balance sheet. I would have expected profitability to be more resilient, so can't go above AMBER now.

Crest Nicholson Holdings (LON:CRST) - down 14% to 167.3p (£430m) - Trading Update (profit warning) - Graham - GREEN

This housebuilder reports a sharp reduction in expected profitability due to lower transaction levels. I think that property prices will fall further from here but also suspect that this has been priced in already at Crest’s current market cap. Discount to NTAV is tempting.

DP Eurasia NV (LON:DPEU) - up 3% to 52p (£76m) - Update on Russian Business - Graham - AMBER

This rises on news that the Russian subsidiary will file for bankruptcy. It’s good news as the losses and the risks associated with Russia will finally be over. DPEU investors will hopefully be left with a good, profitable business in Turkey. Could be worth a second look.

888 Holdings (LON:888) - down 1% to 115p (£515m) - Holdings in Company - Graham - AMBER

[No section below] [Graham has a long position in 888] We don’t usually comment on a “Holdings” RNS, but I think it’s noteworthy that the former GVC/ Entain (LON:ENT) executives, through their consortium vehicle “FS Gaming”, have started to cut their stake in 888, after their proposals were rejected by 888. Formerly at a 6.6% holding, when they wanted to take control of the company, they are now at 4.5%. Why wouldn’t they sell all the way down to zero, now that their takeover plans have been scuppered? There are some regulatory concerns surrounding GVC/Entain’s historical conduct, and these could potentially have led to problems for 888. 888 should hopefully be able to move on now with a clean bill of regulatory health, although I suspect there will be continued selling pressure from FS Gaming.

Paul’s Section:

Robert Walters (LON:RWA)

383p (£280m) - H1 Results - Paul - AMBER

This is a backlog item, which issued H1 results on 1 August.

I’ve been meaning to review it, as it’s always struck me as a good company at a reasonable price. However, I see that forecasts for FY 12/2023 have reduced substantially, from around 50p EPS a few months ago, to c.30p now. Has the lustre come off this share, will I still rate it highly after seeing the latest numbers? Here at the SCVR we have absolutely no problem changing our mind, if the facts, figures, and forecasts change, that’s the only logical thing to do after all.

Although investors also need to think about the cyclicality of earnings through the economic cycle. If a company is having an unusually weak year because of a cyclical downturn in the economy, at some stage it makes sense to anticipate a recovery, and higher earnings. I’m not sure what stage we’re at, as the macro position is quite fluid & uncertain.

Recapping on previous SCVRs for background, we commented as follows -

6/4/2023 - GREEN - 424p - Solid Q1 TU, Mixed outlook. Roland saw valuation as attractive.

14/6/2023 - AMBER - 402p - Profit warning, FY 12/2023 “significantly lower” than exps. V strong bal sht, Paul thinks it should recover in time.

6/7/2023 - AMBER/GREEN - 417p - Q2 softer revenues. Short-term uncertainty. Paul still thinks it should be fine longer-term.

As you can see, given a string of disappointing updates and considerably lowered forecasts, the share price hasn’t actually been hit particularly hard, particularly given the weak overall small caps stock market. The main move down happened in March, before the above negative newsflow.

Here’s the 2023 YTD (year to date) chart, which still looks firmly in a downtrend -

Let’s have a look at the H1 figures.

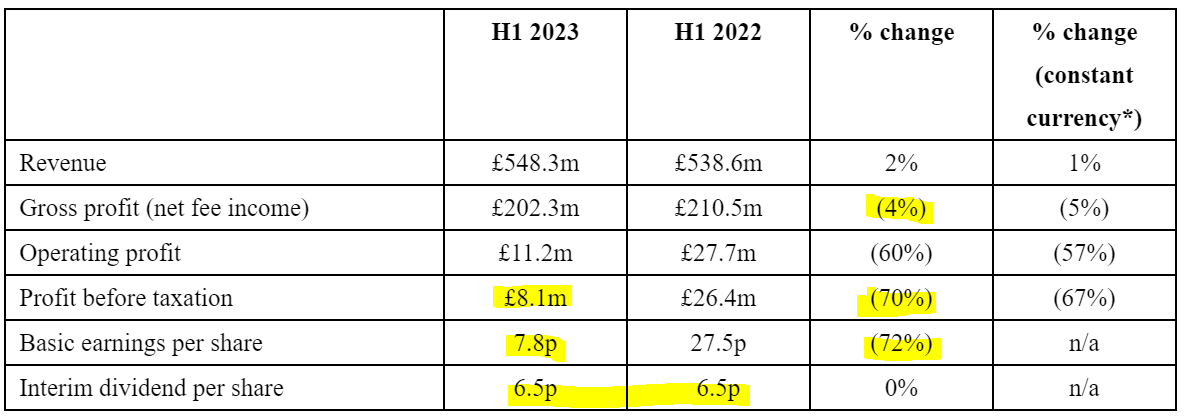

Robert Walters plc (LSE: RWA), the leading international recruitment group, today announces its half-yearly financial results for the six months ended 30 June 2023.

It’s not clear if these are adjusted, or statutory H1 numbers, but they look poor regardless -

This needs some explaining! Why is PBT and EPS down 70%, when NFI is only down 4%? That seems odd. I suspect the reason is that RWA increased its overheads over the last couple of years, which as we’ve discussed here before, now looks ill-timed.

H1 dividend - is maintained at 6.5p, but note it’s now only just covered by H1 earnings.

Brokers are forecasting divis being maintained, with the yield an attractive 6.4%.

Share buybacks have been ongoing.

Contract/temps now generate 33% of revenue (up from 29%).

This is an international business - mainly Europe & Asia, which generate 76% of NFI - so we shouldn’t make any false conclusions about these results from how the UK economy is performing.

Current trading - “remains in line with Board expectations”

Sector comments - quite interesting for possible read-across to other shares -

Candidate and client confidence has been muted throughout the first half of 2023 in a continuation of the trend we first experienced during the second half of last year. Whilst recruitment market fundamentals such as vacancy levels, candidate shortages and wage inflation have remained relatively solid, job churn has reduced, and time-to-hire has lengthened and been compounded by a noticeable increase in buybacks as organisations fight to retain their top talent.

I’ve not heard the term “buybacks” from a recruiter before. From the context I presume this means companies offering people more money to stay put, when they announce that they’re leaving?

The technology and financial services sectors have been particularly volatile during the period. Large-scale technology layoffs have continued right across the globe, a rightsizing of the industry following the high volume of hiring to underpin the global digital transformation that has taken place over recent years. The collapse and merger of several banks during the first half also served to affect confidence levels across the financial services market worldwide.

Geographies -

On a regional basis, Europe and Asia Pacific, which together account for 76% of the Group's net fee income, proved to be most resilient with our blend of permanent, interim and contract recruitment underpinning growth in net fee income across Europe in particular. Our UK, US and Mainland China businesses have been most significantly impacted by the lack of client and candidate confidence and we have been and are acting in each market to mitigate the short-term pressure but with a sensible lens to ensure we are still able to quickly take advantage of any return in confidence.

Balance sheet - NAV is £166m, less intangible assets of £31m, gives a healthy NTAV position of £135m. That’s nearly half the £280m market cap supported by what is mainly working capital, since fixed assets are modest in this sector.

Net cash looks very healthy at £69.8m at 30 June 2023, meaning RWA has plenty of flexibility, strength, and of course the ability to keep paying divis and doing buybacks, despite the disappointing level of profit currently. It’s much better to hold high yielding shares where there’s pots of cash available for divis, rather than some other situations where divis are being paid out of bank debt.

Overall then, there’s nothing to worry about with RWA’s balance sheet, it’s solid, and well able to withstand an economic downturn, should it worsen.

Paul’s opinion - I’m unsettled by the sharp drop in profitability, because it’s not as if the world is in a recession. So if the first signs of trouble produce a halving of profit forecasts, then maybe RWA isn’t such a good business after all?

It seems to be in a tricky position where it’s increased overheads (which will be mainly people and premises, I suppose) at a time when the sector is turning down. Now it will be having the quandary of whether to maintain higher overheads, or reverse course to boost short-term profitability (but maybe then not being in such a good position to capitalise on future recovering markets).

Overall, I’m lukewarm on RWA shares now, so viewing it AMBER.

I now much prefer SThree (LON:STEM) which has not seen any major reduction in its forecasts, and seems to have more reliable repeating earnings from mainly contract (temporary) staff. Whereas RWA seems to have been hurt by both increased overheads, and a greater reliance on permanent recruitment.

For these reasons, I’m not tempted to put RWA on my personal list of possible buys, I think it would need to be a good bit cheaper to tempt me into taking the uncertain macro risk. In any case, with SThree (LON:STEM) now looking the more robust of the two staffing companies we’ve previously admired here, then I’m more likely to focus any available money on that one.

There again, the leveraged downturn that RWA has seen, could flip into a leveraged upside case once macro improves.

As with a lot of cyclical sectors, it currently feels too soon to be bottom-fishing for a recovery, in my view - we can’t just ignore the worsening newsflow.

Fulcrum Utility Services (LON:FCRM)

Down 70% to 0.25p (£1m) - Results & Delisting - Paul - RED

We’ve not looked at this nanocap this year, because it’s too small, and performance in recent years has been disastrous. I last commented here on 5/12/2022, with a RED opinion, noting the big discount on a convertible (at 0.5p) emergency loan fundraise.

It's always worth looking at situations that have gone wrong, to learn from them, and avoid similar situations in future.

For a little while, earlier in 2022, this share had looked quite interesting as what looked like a fairly well-funded potential turnaround. However, the commentary from management turned out to be wildly optimistic, and the cash ran out, leaving it at the mercy of major shareholders including Harwood Capital, who certainly extract their pound of flesh in crisis situations, potentially diluting existing holders to almost nothing through a 0.5p convertible loan. When they're the only game in town, activist shareholders just name their terms, and management don't have any other options.

Figures today for FY 3/2023 look bad, but it’s still a significant sized business, and the balance sheet isn’t actually too bad (NTAV of £18m). The trouble is inadequate liquidity, which has enabled the two largest shareholders (Bayford & Harwood) to lock it in their vice-like grip, and take control. Now they’re delisting it, to save costs and simplify the business. I wonder if, once they've sorted it out, it might come back to the market at a very large multiple of the current market cap?! That's a tried & tested strategy in Harwood's playbook.

Small shareholders had plenty of opportunity to sell up, so it’s difficult to understand why anyone would still be holding now?

Anyway, that’s the end of that one - for small shareholders anyway, although there might be a chance to retain a position in it as a private company, which can sometimes work out alright.

Graham’s Section:

Crest Nicholson Holdings (LON:CRST)

Share price: 167.3p (-14%)

Market cap: £430m

It’s a profit warning from this property developer. Transaction levels across the industry have weakened, “particularly in recent weeks”, with no material improvement expected between now and the company’s financial year-end in October.

Here is the explanation:

Against a backdrop of persistently high inflation and rising interest rates, trading conditions for the housing market have worsened during the summer of this year. While pricing has remained resilient in a market with limited supply and few distressed sellers, the economic uncertainty is deterring prospective home movers. Additional mortgage borrowing for those looking to upgrade or for those with low levels of equity, notably first-time buyers, has become significantly more expensive with no Government support (following the end of Help to Buy) now in place to cushion this impact.

For buyers, is this currently the worst of all possible worlds? Usually, higher borrowing costs should be accompanied by the compensation of an attractive discount in the price paid. But the discount on offer is very limited: according to Nationwide, house prices have fallen by 3.8% in the year to July 2023.

That is the largest fall since 2009, and it’s much larger in real terms if you subtract inflation over the past year, but it’s hardly the sort of fall you might have been hoping for if you are going to pay 6% on your new mortgage.

First-time buyers can be forgiven for taking a “wait-and-see” approach. Some will have no choice, given the affordability constraints. And with fewer transactions taking place, maybe it is only a matter of time before sellers start to accept larger price reductions?

At Crest, sales per outlet per week (“SPOW”) has fallen to 0.25 over the past seven weeks, versus a forecast rate of 0.50.

Management actions - the land portfolio has been increased with the addition of “several high-quality sites”, but Crest “expects future land activity to reduce significantly”. Cost overheads will be reduced for next year.

Dividend - the profit warning does not affect the declared dividend.

Outlook - “positive and confident” over the medium term, as inflation and rates are expected to reduce. Adjusted PBT is now expected to be c. £50m (previously forecast to be over £73.7m).

Graham’s view

This is a severe profit warning that has emerged over just a seven week period. It’s another reminder that housebuilder profits are highly vulnerable to macro conditions.

And when the company says it is positive and confident over the medium term, because interest rates and inflation are expected to reduce, I think it’s important to bear in mind that the company has no idea when these things will happen - none of us know for certain!

However, despite the enormous uncertainty clouding the outlook here, I’m going to maintain a Green view on the shares, on valuation grounds.

Crest has been weak for some time, and is making new lows today. I think this profit warning was largely priced in already:

Paul covered the H1 results here, and noted that the company had a tangible balance sheet value of a staggering £848m, and a net cash position.

Therefore, I like the risk:reward on offer at a market cap today of c. £430m. Even if asset values are written down significantly, the stock is still likely to be trading at a healthy discount to tangible NAV.

How long it might take for inflation and interest rates to reduce is anyone’s guess. But even at a much lower rate of profitability than Crest shareholders have become accustomed to (e.g. PBT of £40-50m p.a.), I think this stock is potentially attractive at these levels.

The ValueRank of 97 here tells the story: the stock is looking very cheap. Perhaps that is for good reasons. But for patient investors who hold this until conditions are booming again, I think it could be very interesting:

DP Eurasia NV (LON:DPEU)

Share price: 52p (+3%)

Market cap: £76m

This Domino’s pizza company has reached a conclusion for its Russian operations: bankruptcy proceedings.

While that might not sound very promising, it does put a full stop on the Russian business which had already been classified as “discontinuing” (see our report in January). DPEU did attempt to sell it as a going concern, but those attempts have come to nothing.

When this stock was originally listed in 2017, the Russian growth story was its most exciting component, as the business in Turkey was already mature.

With the attempt to make money in Russia now conclusively over, it’s understandable that the evolution of the stock price looks like the chart below. It’s hard to imagine that Domino’s will be going back into Russia any time soon:

The financial consequences of the proposed bankruptcy are explained as follows:

It is too early to have an exact estimate of the financial impact of a potential insolvency of DPRussia on the consolidated financial position and results of the Company. The Company can confirm that the external debt of the Russian segment is an amount of c.RUB 520 million, which was guaranteed by, inter alia, the Group's Turkish subsidiary, has been fully and finally settled by the Turkish subsidiary out of existing cash resources, with the Group's gross debt reducing accordingly and a resulting gross cash balance of TRY 162 million (based on the actual but unaudited cash position as at 18 August 2023).

Since DPEU’s financial performance has been less than stellar over the years, and the balance sheet has not been terribly strong, I think it’s important to take a moment dwell on the cash/debt position here.

Firstly, the amount paid off in Russia: 520 million Rubles converts to only about £4 million.

With that amount paid off, DPEU is now left with a gross cash balance of 162 million Lira (£4.7m).

According to the June trading update, the company had access to an undrawn £15m bank facility (in Lira).

Bottom line: DPEU should have access to plenty of liquidity, even after paying off the external debts of the Russian business.

Overall, it does still have a net debt position. A recent -July - broker note from Liberum forecast that the company would finish 2023 with net debt equivalent to c. £16m (using latest exchange rates).

So the company remains significantly indebted, but with good continued access to liquidity.

Graham’s view

It will be easier to judge this when the dust settles: hyperinflation in Turkey and military operations with Russia have been more than slight distractions for DPEU and have impacted financial performance in a variety of ways.

But I think it’s possible that when we finally do get clarity, the picture that emerges could be a pleasant surprise.

The most recent full-year results from the company showed an operating profit on continuing operations of 189 million Lira (£5.5m). Unfortunately, the moving parts of hyperinflation, debt interest expense, and losses on the Russian operations made things complicated for investors to understand.

I’m remaining neutral on this but am primed to turn positive if we start to get clean numbers out of Turkey and an improving balance sheet.

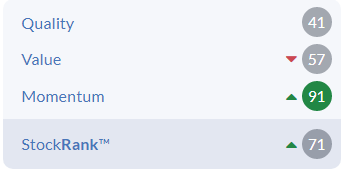

The StockReport is starting to see things it likes here, with the StockRank rising to 71:

See what our investor community has to say

Enjoying the free article? Unlock access to all subscriber comments and dive deeper into discussions from our experienced community of private investors. Don't miss out on valuable insights. Start your free trial today!

Start your free trialWe require a payment card to verify your account, but you can cancel anytime with a single click and won’t be charged.