Good morning from Paul & Graham!

We're still having remarkably hot weather in the UK. As Father Ted once said during a September heatwave, "If it stays this warm throughout the whole of the winter, we won't need to turn on the heating at all!" (shortly after he had blown the entire year's heating allowance betting on the wrong sheep). Sometimes my portfolio feels like I've bet on the wrong sheep too, so remarkable parallels there.

Mello Monday 5pm today - is this evening, great to see these interesting investor shows back after a summer break. I’m looking forward to hearing highly experienced fund manager Rosemary Banyard interviewed, she talks a lot of sense, and kicks off the show at 17:00. Also the BASH session is always good. Do support these events, as the danger is in a bear market, investor apathy might mean they wither away.

Explanatory notes -

A quick reminder that we don’t recommend any stocks. We aim to review trading updates & results of the day and offer our opinions on them as possible candidates for further research if they interest you. Our opinions will sometimes turn out to be right, and sometimes wrong, because it's anybody's guess what direction market sentiment will take & nobody can predict the future with certainty. We are analysing the company fundamentals, not trying to predict market sentiment.

We stick to companies that have issued news on the day, with market caps up to about £1bn. We avoid the smallest, and most speculative companies, and also avoid a few specialist sectors (e.g. natural resources, pharma/biotech).

A key assumption is that readers DYOR (do your own research), and make your own investment decisions. Reader comments are welcomed - please be civil, rational, and include the company name/ticker, otherwise people won't necessarily know what company you are referring to.

What does our colour-coding mean? Will it guarantee instant, easy riches? Sadly not! Share prices move up or down for many reasons, and can often detach from the company fundamentals. So we're not making any predictions about what share prices will do.

Green (thumbs up) - means in our opinion, a company is well-financed (so low risk of dilution/insolvency), is trading well, and has a reasonably good outlook, with the shares reasonably priced.

Amber - means we don't have a strong view either way, and can see some positives, and some negatives. Often companies like this are good, but expensive.

Red (thumbs down) - means we see significant, or serious problems, so anyone looking at the share needs to be aware of the high risk.

Scraping the barrel today, I'm afraid -

Summaries

Restaurant (LON:RTN) - 47.5p (pre market) £363m - Proposed sale of leisure business - Paul - AMBER/RED

As usual, RTN tries to put a positive spin on a not very good situation - it's having to pay another group £7.5m to take away what's left of its loss-making Chiquito's and Frankie & Benny's restaurant chains. Some lease liabilities remain with RTN though. I reiterate my concerns below about RTN's weak trading, and dangerously stretched balance sheet.

Sportech (LON:SPO) - down 68% to 30.7p (£3m) - Proposed delisting - Graham - AMBER

This small betting company proposes to exit stage left. I’m neutral as the current derisory market cap seems too low, but how many of us want to own shares in a private company? I take the opportunity to remind everyone (including myself) to be careful with delisting risk.

Not a small cap but ….

Vistry (LON:VTY) (mid cap housebuilder) caught my eye, being up 14% to 910p today (£3.2bn). It’s now up 31% since the recent low just 3 weeks ago. H1 results are “robust” (profit up vs LY H1), and in line with expectations. It reiterates FY 12/2023 profit guidance. Note that broker consensus forecasts fell about 40% in late 2022, but have been flat, or slightly up, throughout 2023 to date - surprisingly resilient in a very tough sector. It seems to have a more resilient business model, with public/private developments, with “good demand” for rental affordable housing from local authorities and others. Cost synergies from the acquisition on Countryside. Strong forward order book. Superb balance sheet with £2.0bn NTAV, including huge inventories number of £3.2bn.

Paul’s opinion - I don’t know this company very well, but want to flag it to you as something to possibly research more, if you want upside/recovery from the housebuilding sector, but with seemingly more downside protection than conventional companies in this space, due to its mixed business model (public & private). [no section below]

Inspired (LON:INSE) - down 6% to 85.25p (£86m) - Results for H1 - Graham - RED

These shares are lower despite the company confirming full-year guidance, and the broker increasing estimates for 2024 and 2025. I’m a sceptic on this one due to its balance sheet, debt, acquisition strategy and the presentation of its barely profitable results.

ENGAGE XR Holdings (LON:EXR) - up 14% to 3.24p (£17m) - Interim Results - Graham - RED

This “Metaverse/Spatial computing technology company” announces a pre-tax loss in line with expectations of €2.2m over the six months to June 2023. Revenues were about the same size as the loss (€2.1m, up 18% year-on-year). The company says revenue momentum is picking up, with €1m generated over July and August.

Thanks to a fundraise, the company finished H1 with over €9m of cash. Cash burn in H1 was around €3m so it should have some cash runway - over a year, hopefully? Maybe 18-24 months? Best of luck to investors in this one but I have to give it the thumbs down based on the statistical improbability of it working out. The StockRank is 11 (including a ValueRank of 2).

WANdisco (LON:WAND) - down 6% to 62p (£73m) - Interim Results - Paul - RED

I won’t go over all the detail again, as we’ve wasted far too much time on this dreadful company in the last year. The short version is that the exponential rise in sales bookings, which took the market cap up to nearly £1bn, was all a fraud. Despite this, the rich & successful financial backers refinanced it at 50p, and shares have come back from suspension.

Today we have more dreadful figures from WANdisco (LON:WAND) as expected. My main concern is that the forecast cash is said to be down to $16m by Dec 2023. It raised $30m recently, so is tearing through that fresh cash raise pretty fast (although c.$7m one-off costs re survival/restructuring/fraud).

Looks utterly grim, for sure, as the published accounts always have done. I foolishly believed their too-good-to-be-true bookings/pipeline RNSs, which of course then turned out to be completely fictitious, not something that anyone predicted I don't think.

Paul’s opinion - I can’t see any merit in this share for now. Given the rate of cash burn, it has to be RED.

M P Evans (LON:MPE) - down c.3% to 740p (£399m) - Interim Results - Paul - AMBER/GREEN

Fancy owning part of an Indonesian palm oil producer? Then this is your share! A long track record of generous divis, strong asset backing, and reasonable PER have caught my interest here. H1 profits are well down, but it sounds like H2 is improving, and Cavendish leaves forecasts unchanged. Could be worth a closer look, but obvious overseas risk, and volatility of price for its palm oil production.

Paul’s Section:

Restaurant (LON:RTN)

47.5p (pre market) £363m - Proposed sale of leisure business - Paul - AMBER/RED

I reviewed the interim results here last week, and was distinctly unimpressed with the wafer thin profit margin, and the awful, overly-indebted balance sheet, also with onerous lease liabilities.

Press reports over the weekend suggested a deal was imminent for the disposal of its slowest-growing leisure division (Chiquito’s, and Frankie & Benny’s restaurants). A “dowry” was mentioned in press articles, suggesting that RTN would actually be paying the buyer to take away its problem leisure division.

Today it says -

- Agreement signed to sell 75 trading sites to Big Table Group (private equity backed, operator of Bella Italia, Las Iguanas, and Banana Tree) for £1.

- RTN will pay £7.5m to Big Table Group, to get rid of this loss-making division.

- Expected to complete soon, in early Q4 2023.

- Improves leverage - not really, because it’s only getting rid of lease liabilities, not actual debt.

I don’t like the sound of this bit (equity placing on the cards, possibly?) -

…continuing to actively explore its strategic options to further accelerate margin accretion and deleveraging.

I don’t like this bit either, which suggests that there might be some potential liabilities remaining for RTN (TRG) -

Sites that have been previously closed as part of the Leisure businesses estate rationalisation plan will remain the responsibility of TRG… and we expect to exit the majority of the lease obligations of the recently closed sites by the end of FY24. We would therefore expect the remaining liability and expected cash outflow from closed sites (most of which are currently sub-let) to be no more than £1m to £2m a year from FY25 onwards.

Paul’s opinion - it’s striking how RTN has got rid of most of its original businesses. Some investors thought the acquisition of Wagamama a few years ago was a life raft for management, tacitly admitting that their older brands were withering away. They were right!

It’s another demonstration of how restaurant chains come in and out of fashion, and that they have to continuously adapt to stay relevant. Also, there's clearly still over-capacity in the restaurant sector. Good reasons why I’m avoiding this sector altogether these days - it’s so difficult to make any profit at all, after the big hikes in wages, energy, and raw materials. It could take years to rebuild margins, if that's even possible.

Why get involved here, when it’s also laden with excessive debt, which could further destroy what’s left of shareholder value?

Shareholders must be hoping that the consumer squeeze ends, and households increase their spending on eating out. And that costs reduce. If those things don’t happen, then it’s difficult to see RTN making any progress, and with little to no prospects of any meaningful divis, why would anyone want to invest here?

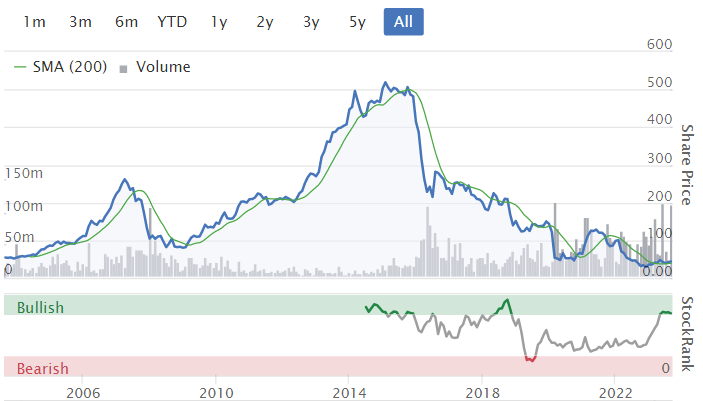

A reminder below of the huge shareholder value destruction long-term at RTN. It's now hoping that Wagamama will succeed, where the other brands failed -

M P Evans (LON:MPE)

Down c.3% to 740p (£399m) - Interim Results - Paul - AMBER/GREEN

A producer of sustainable palm oil in Indonesia. Not a company I follow or understand. Graham reviewed it here in Dec 2022, sounding quite positive.

H1 figures today look poor - operating profit is 62% down to $23.4m.

Interim divi maintained at 12.5p is a good sign. Note that the FY 12/2023 forecast yield is a healthy 5.6%, and the history of paying reliable and growing divis is excellent, over many years.

Post period end it agreed a substantial $60m purchase of 8,350 hectares of planted land.

Outlook comments are vague, with no mention of performance vs expectations. But it does say that new land purchases

…along with increasing cropping levels, put the Group in a strong position to deliver a productive and profitable 2023 and bodes well for its longer-term prosperity."

Also, production in H2 to date (July & Aug) is up 35% on H1’s rate, which sounds good.

Balance sheet - looks good. Large NTAV of $467m, means it effectively owns outright the land & palm trees on them and all its equipment. Cash offsets borrowings.

Paul’s opinion - not a share I’m familiar with, but the lowish PER, strong asset backing, and generous/reliable divis (plus small buybacks) impress me. Cavendish has left forecasts unchanged, so see their note for more info. Could be worth a closer look. I’ll go with AMBER/GREEN - modestly favourable.

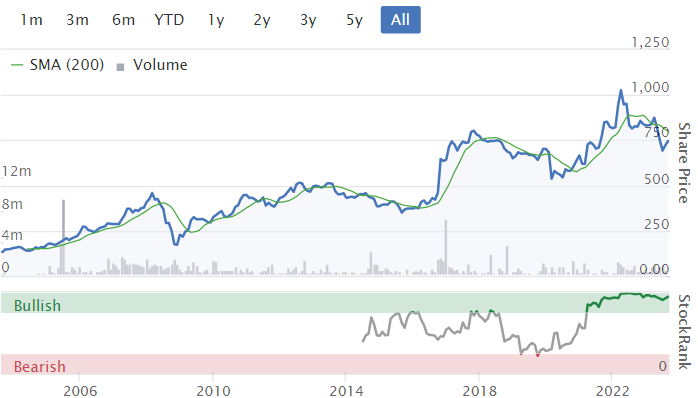

Very good long-term share price performance, especially if you add on all the generous divis on top of the share price -

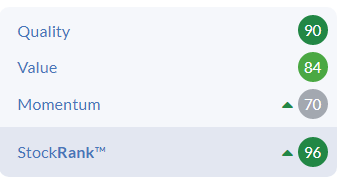

Stockopedia's computers put a cherry on top, with a high StockRank -

Graham’s Section:

Sportech (LON:SPO)

Share price: 30.7p (-68%)

Market cap: £3m

We covered this one very rarely - when I looked at it in April, it was the first mention of the stock in five years.

This morning, we are reminded why we normally use a £10m market cap cut-off. This one had a £9m market cap last night. It is now just £3m.

It has signalled an intention to delist, pending shareholder approval (a vote in favour with 75% support is required).

Sportech has at least distributed vast amounts of cash to shareholders over recent years - £121m since 2017.

The remaining businesses are of a small size: revenues of £13.5m in H1 (according to the interim results published today), with adjusted EBITDA of less than £1m.

I note the presence of Harwood Capital: they are the third largest shareholder with 18%, recently (30th August) announcing an increase from 17%. This may just be a coincidence, but we are used to the pattern of seeing Harwood-related entities delisting.

Are Sportech’s existing business worth more than £3m? The end-of-August cash balance is slightly more than that, and it owns betting licences and venues in Connecticut. So I would say that the answer is perhaps yes - for anyone who is happy to own an unlisted company.

At a sub-£10m market cap, with limited liquidity, and with no plans to raise funds, I tend to agree that a stock market listing is uneconomical for companies with this profile.

It’s another good reminder to check whether any companies you own are at risk of delisting in a manner that might be unfavourable to you.

Remaining Sportech shareholders will be feeling sore this morning with the share price down nearly 70% on this announcement. Perhaps we don’t talk about delisting risk enough - it’s one of the most serious and most common dangers of micro-cap investing.

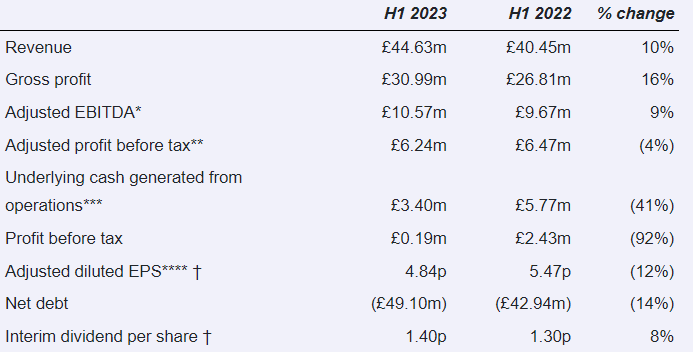

Inspired (LON:INSE)

Share price: 85.25p (-6%)

Market cap: £86m

Inspired (AIM: INSE), a leading technology enabled service provider supporting businesses in their drive to reduce energy consumption, deliver net-zero, control energy costs and manage their response to climate change, announces its consolidated, unaudited half-year results for the six-months ended 30 June 2023.

I fully agree with Paul that energy consultants aren’t the most attractive of investment sectors, and I’d be inclined to avoid them entirely.

Let’s see if there is anything in these H1 results that might spark some interest:

Note that actual PBT is close to zero, despite revenues of £45m and “adjusted EBITDA” of £10.6m.

Net debt of £49m is significant relative to e.g. the company’s market cap and its profitability.

As flagged by Paul in January, there are significant liabilities relating to acquisitions. In H1, £8.6m was paid in earnouts for prior acquisitions.

Balance sheet - this has negative tangible value and looks quite ugly to me.

Tangible value minus £32 million.

Cash £8.4m

Contingent consideration £11.3m in current liabilities (i.e. due within a year).

Bank borrowings £57.5m

£46m of value is tied up in receivables - much of it not invoiced/due yet. The company says that some of this has unwound since H2 began but regardless, working capital management will be crucial when dealing with a number of this size.

Liquidity - only £2.4m of the company’s RCF was undrawn at the end of H1. Normally that would imply almost no headroom, but there was also a £25m “accordion” facility (i.e. it may have been possible to borrow more, if the lenders agreed).

Outlook - “The over-arching business necessity for energy efficiency initiatives should support continued strong demand for the value added by Optimisation Services in H2. ESG Services is expected to maintain its strong momentum in H2..”

The Board is “confident in delivering market consensus for the full year 2023.”

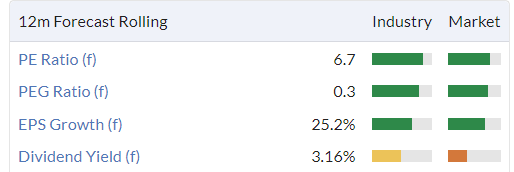

Graham’s view

I was thinking of sticking with a neutral stance on this, due to the valuation:

However, a neutral stance wouldn’t convey what I really feel - which is that this one is to be avoided.

It promotes a nonsense adjusted EBITDA metric that excludes many important costs, including large spending on internally-generated intangible assets.

Balance sheet is hollowed out by acquisitions, leaving negative tangible value for shareholders.

Net debt is significant and the company is carrying large acquisition-related liabilities, too.

Operates in a highly competitive sector and currently earning very little or zero real profits.

A history of shareholder dilution with a rising share count.

So for me personally, this is a bargepole situation.

The shares are lower today despite confirming its 2023 estimates, and the broker increasing estimates for 2024 and 2025 - perhaps the market is starting to get worried about this one?

See what our investor community has to say

Enjoying the free article? Unlock access to all subscriber comments and dive deeper into discussions from our experienced community of private investors. Don't miss out on valuable insights. Start your free trial today!

Start your free trialWe require a payment card to verify your account, but you can cancel anytime with a single click and won’t be charged.