Good morning from Paul!

I'll leave it there for today, and the week.

Didn't buy Warpaint? - really insightful article here from Ed, delving into a new study on momentum. Very topical as we enter a new bull market. I've also always had problems buying shares in an up-trend, and where valuation looks stretched. I've missed loads of good investments in this way, sitting on the sidelines complaining about a stretched valuation whilst it gradually multibags! So there's a lot I need to learn about just paying up for the best companies, and not letting the value investor in me block that path. Although there's also the point that this strategy could result in over-paying for stretched shares, right at the top.

Explanatory notes -

A quick reminder that we don’t recommend any shares. We aim to review trading updates & results of the day and offer our opinions on them as possible candidates for further research if they interest you. Our opinions will sometimes turn out to be right, and sometimes wrong, because it's anybody's guess what direction market sentiment will take & nobody can predict the future with certainty. We are analysing the company fundamentals, not trying to predict market sentiment.

We stick to companies that have issued news on the day, with market caps (usually) between £10m and £1bn. We usually avoid the smallest, and most speculative companies, and also avoid a few specialist sectors (e.g. natural resources, pharma/biotech, investment cos). Although if something is newsworthy and interesting, we'll try to comment on it. Please bear in mind the "list of companies reporting" is precisely that - it's not a to do list. We typically cover c.5 companies per day, with a particular emphasis on under/over expectations updates, and we follow the "most viewed" list of readers, so if you're collectively interested in a company, we'll try to cover it. Obviously with the resources available, we can't cover everything! Add you own comments if you see something interesting, and feel free to discuss anything shares-related in the comments.

A key assumption is that readers DYOR (do your own research), and make your own investment decisions. Reader comments are welcomed - please be civil, rational, and include the company name/ticker, otherwise people won't necessarily know what company you are referring to, if they are using unthreaded viewing of comments.

What does our colour-coding mean? Will it guarantee instant, easy riches? Sadly not! Share prices move up or down for many reasons, and can often detach from the company fundamentals. So we're not making any predictions about what share prices will do.

Green (thumbs up) - means in our opinion, a company is well-financed (so low risk of dilution/insolvency), is trading well, and has a reasonably good outlook, with the shares reasonably priced. And/or it's such deep value that we see a good chance of a turnaround, and think that the share price might have overshot on the downside.

Amber - means we don't have a strong view either way, and can see some positives, and some negatives. Often companies like this are good, but expensive.

Red (thumbs down) - means we see significant, or serious problems, so anyone looking at the share needs to be aware of the high risk. Sometimes risky shares can produce high returns, if they survive/recover. So again, we're not saying the share price will necessarily under-perform, we're just flagging the high risk.

Links:

Paul & Graham's 2024 share ideas - live price-tracking spreadsheet (2 separate tabs at bottom),

Frozen SCVR summary spreadsheet for calendar 2023.

New SCVR summary spreadsheet from July 2023 onwards.

Paul's podcasts (weekly summary of SCVRs & macro views) - or search on any podcast provider for "Paul Scott small caps" - eg Apple, Spotify.

Companies Reporting

Summaries

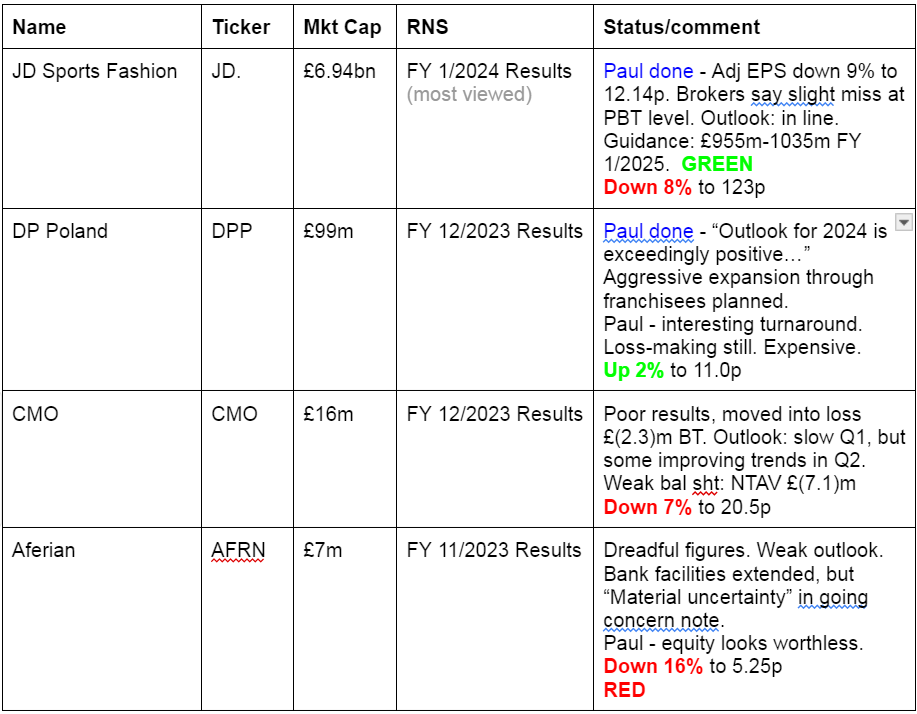

JD Sports Fashion (LON:JD.) - down 11% to 118p (at 08:47) £6.18bn - FY 1/2024 Results - Paul - GREEN

A slight miss at PBT level. Outlook is unchanged for FY 1/2025. I don't understand why the market has dropped this 11% today. Looks a quality company to me, which has self-funded terrific growth in the last 6 years, despite the pandemic & tough macro. Seems too cheap on a PER c.10x.

DP Poland (LON:DPP) - up 2% to 11.0p (£101m) - FY 12/2023 Results - Paul - AMBER

Some exciting bull points here in an interesting turnaround, but the valuation seems way too high to me.

Paul’s Section:

JD Sports Fashion (LON:JD.)

Down 11% to 118p (at 08:47) £6.18bn - FY 1/2024 Results - Paul - GREEN

JD Sports Fashion Plc (the 'Group'), the leading global retailer of sports, fashion and outdoor brands, today announces its full year unaudited results for the 53 weeks ended 3 February 2024.

My initial skim of the results & outlook led me to believe the figures and outlook were in line. So why have the shares dropped 11% this morning? To start with, I’ve got conflicting information on whether the FY 1/2024 results are slightly ahead of expectations (12.14p adj EPS actual, vs 11.8p consensus shown on the StockReport, suggesting a 3% beat), or below expectations (as a couple of brokers suggest)?

In a morning summary note, Winterfloods says the figures are a small miss at PBT level, and notes a small cut in the dividend. Full year divis are actually up from 0.8p LY, to 0.9p this year, but I note the split has changed, so that the final divi was 0.67p LY, and is 0.6p this year. Divis are not material here anyway, as the yield is under 1%, since cashflows are mainly being applied to organic (new stores) and acquisitive growth.

Another broker says PBT at £917m was slightly below expectations of £923m, so overall it looks like a slight miss at PBT level, but nothing to get steamed up about. The -11% share price move this morning seems an over-reaction, but is really only giving up the gains in the 3 days prior to this results release. Maybe traders bought in anticipation of stronger numbers & outlook, and exited this morning? Who knows!

In any case I am encouraged when companies I like become cheaper, providing nothing significant has gone wrong, which it hasn’t here.

JD is a big business these days, and international. Some key numbers for FY 1/2024 -

Revenue £10,542m

Adj PBT £917m (down 8%)

Adj EPS 12.14p (down 9%)

LFL store revenue growth of 3.8% is below peak inflation, but similar to where inflation is now running.

Wages costs in particular are flagged - with £70m extra, in addition to minimum/living wage increases. Total operating costs rose 5.1%, a bit ahead of LFL store revenue growth, so margins have been pinched slightly, but are still good I think.

Overall, I see those figures as respectable, given that we’ve been in a tough consumer macro environment, with cost pressures too.

Note that JD issued a profit warning, which I covered here on 4/1/2024, which took it down 23% on the day to 119p, causing me to highlight that it looked good value. Things didn’t get any worse, with an in line update on 28/3/2024, hence I remained GREEN here, due to the value, and the good long-term track record of rising profits & EPS. Although note the shares have gone nowhere in the last 5 years, since it’s seen a PER de-rating at the same time as rising EPS, which is unusual. EPS has doubled in the last 5 years, but shares have gone nowhere. Could that be an opportunity, or is the market now telling us it’s a mature business, struggling to generate organic profit growth from existing stores? Could the new stores, and multiple acquisitions of other companies be concealing a deteriorating underlying business maybe? That could be what sceptics think possibly?

Outlook - sounds fine to me in the circumstances -

"We have started the new financial year with Q1 in line with our expectations in a volatile market and we are on track to deliver our profit guidance for the full year. Looking further ahead, we have a strong business model and a clear strategy to deliver long-term growth and value creation for our shareholders."

…and maintaining full year profit before tax and adjusting items guidance of £955m-£1,035m. This includes a c.£55m annual increase, announced at our March update, from the accounting policy change to include amortisation of acquired intangibles as an adjusting item from FY25 onwards.

Balance sheet - has £1,032m net cash (excl lease liabilities).

NAV is £2,868m, less intangible assets of £1,429m, giving NTAV of £1,439m, or about 23% of the market cap. So some asset support here, but it’s mainly an earnings & cashflow company, as is usual in this sector.

There's only been modest dilution in the last 6 years, from 4,866m shares to 5,183m, so JD got through the pandemic, and expanded the business 3-fold in revenue, and more than doubled EPS over this period, almost all self-funded from its own cashflows. That is very impressive you know.

As flagged here before, the only unusual large item on the balance sheet is £810m non-current liabilities called “Put and call option liabilities”. That’s a big number, and seems to relate to acquisitions, buying out minority interests. There’s more detail in note 6, I don’t want to get bogged down in it though. My inkling is that this £810m balance sheet liability sounds like deferred consideration, so I’d net it off against cash, bringing the group to a net cash position of £222m, which is fine.

Acquisition - a large acquisition is in progress (announced 23/4/2024) of Hibbett Inc (NASDAQ listed), for £878m, subject to regulatory and shareholder approval. Expected to complete in H2 of (calendar presumably) 2024. So that could give a catalyst for increased forecasts if it goes through. They’re taking on debt to part-fund it though. My initial worry is that a low-PER UK share buying something on NASDAQ (presumably expensive) could destroy shareholder value. However, a quick look at Hibbett’s StockReport (via my US Stockopedia subscription) shows it is actually modestly valued at a similar PER to JD (even with the bid premium included), and solidly asset-backed too. Just on a quick review, this looks a nice bolt-on deal, with 1,169 stores in 36 US states.

The USA is already JD’s largest market, so will grow further if Hibbett is acquired.

Paul’s opinion - JD is a very ambitious growth company, but it’s priced as a value share, on a forward PER of only about 10x. We don’t have to worry about debt, as the balance sheet looks adequate.

My main reservation is that JD’s business model is to provide trendy showrooms for other companies’ brands. So JD doesn’t have any control over product. What if brands decide to sell direct, and scoop up the retail margin for themselves? I’ve been saying that for years, but it’s still a concern to me. Or maybe JD is too big to be ignored or squeezed by the big brands? I don’t know, what do readers think?

As for the brands, I see Nike (NYQ:NKE) shares have been weak , doing a round trip back down to where they were pre-pandemic, and rated highly still on a PER of 23.7x.

adidas AG (ETR:ADS) in Germany shares have been recovering since Oct 2022, but are still below pre-pandemic share price. That’s on a fwd PER of 48x. So there’s clearly a large valuation gap between the brands (highly valued) and the retailers (lowly valued), which makes sense to me, to some extent. Although maybe the retailers could be too cheap now? If the Hibbett deal happens, I reckon that would add about £1.4bn additional revenues to JD, and £75m post tax earnings. That’s before synergies too, presumably the greater group buying power could squeeze higher margins out of the big brands?

Overall, JD does appeal to me, as a value/GARP share. It’s roughly tripled revenues in the last 6 years, from acquisitions and openings loads of new sites too. PER of 10x does seem oddly cheap. Hence I’m sticking at GREEN. Maybe there are issues I’ve not spotted, so it definitely needs readers to do a much more detailed research process yourselves, as with everything. However, superficially I think it looks well worth a closer look.

Note the StockRank system has fallen out of love with JD shares, previously highly rated it now only gets a middling score -

DP Poland (LON:DPP)

Up 2% to 11.0p (£101m) - FY 12/2023 Results - Paul - AMBER

DP Poland, the operator of pizza stores and restaurants across Poland and Croatia, announces its audited results for the year ended 31 December 2023.

Terrible historical track record of losses every year, multiple fundraises, and shareholder value destruction -

Turnaround - this is the interesting bit. New management seem to have convinced everyone that they’re turning it around, and can create a successful business by switching to a franchising model. This got very credible backing in a Mar 2024 fundraising of c.£20m, enough to resolve its previously weak balance sheet, and fund future expansion. A key positive point is that half the money raised came from the UK Dominos operation, Domino's Pizza (LON:DOM) - this is clearly a superb endorsement of DPP’s turnaround potential.

When the facts change, we change our view, so I was happy to switch from red in 2023, to AMBER on 28/3/2024 when this game-changing fundraise was announced. Graham agreed on 29/4/204 on a trading update showing that it’s approaching profitability.

2023 Results - are poor, and to my mind would only justify a valuation of close to nothing -

EBITDA is positive, but it’s less than the depreciation charge (although that’s distorted by IFRS 16). If we’re kind, then I would see the above as being c.£(2)m loss before tax, having accepted the £1.44m non-cash & non-recurring items.

Balance sheet - was weak at 31/12/2023 with negative NTAV of £(3.0)m, but that has since been comprehensively repaired with the c.£20m equity fundraise in Mar 2024. So NTAV should now be positive, possibly about £15m, if we allow for some more losses in early 2024. Its finances are sorted now I think, so I don’t have any remaining balance sheet concerns.

Outlook - this is what almost all of the market cap relies on. At £101m market cap, and with no historical profits at all, DPP absolutely has to move into significant profits, and demonstrate the ability to strongly grow those profits. It’s very unusual for a business in the hospitality sector that has been a long-term serial loss-maker, to suddenly become a terrific, profitable growth company, but it can happen occasionally when economies of scale kick in, and a brand becomes well-liked by customers.

New management are also highly regarded, several sector experts have told me, so that could be a key catalyst, well it already has been, given the mkt cap has soared, and they got a big fundraise away, including £10m from UK Dominos.

Very strong LFL store sales growth so far in 2024, this is very impressive - as it needs to be -

Looking to 2024, our strong growth has continued, with LFL sales up 19.9% year to end of April. Supported by our recent fundraise, we aim to open 45-50 new stores, upgrade 25-30 stores, and transition to a franchise model. I'm excited about our future and our team's potential to continue delivering."

Although note that it mentions high inflation in 2023 of 11.4% (Poland) and 8.4% (Croatia). I’ve checked the latest figures, and these have come right down, to 2.5% in Poland and 3.3% in Croatia (year to April 2024). Therefore the +19.9% LFL sales growth so far in 2024 is almost all genuine, real terms growth. Very good!

Current trading is in line -

Forecasts - thanks to Singers for an update today, as follows -

FY 12/2024 - adj PBT £0.7m, adj EPS 0.1p

FY 12/2025 - adj PBT £2.9m, adj EPS 0.2p

FY 12/2026 - adj PBT £4.6m, adj EPS 0.4p

Let’s be very generous and put it on 20x forecast 2026 EPS, that would be a share price of 8.0p.

Slight problem here, the share price is already well above that, at 11.0p.

So bulls must be hoping not only that DPP can move into profit, but that it can smash these forecasts.

Paul’s opinion - it’s a turnaround, no arguments there, but from basket case, to something that might reach breakeven shortly. It's difficult to get excited about that.

However, the forecast upside is already more than fully baked into the share price today. So where’s my upside, if I decide to buy at 11p?

Also, the franchise side of things is an aspiration. Franchising only works if there’s a really big profit margin, which can be shared between the brand owner, and the franchisee. Since DPP’s own stores generate very little site level profit at the moment, why would anyone want to set up a franchised store that’s unlikely to make them much (if any) profit after fees? Also, franchise operations can be a handful to manage, as the operators have autonomy, and might start doing things the main company may not like.

Overall then, I like the beginnings of a turnaround, and it should be good if DPP can (after many years) finally deliver a maiden profit (slightly above breakeven). Does that make it a business worth £101m though? Not by a long shot, in my opinion. To me, this share is worth maybe £20-30m market cap. Hence the £101m market cap is way above my perception of value, based on the existing forecasts. So where’s my upside going to come from? Unless it delivers stellar trading updates, there’s a considerable risk here that the shares might slowly drift back down. So at the moment, I think risk:reward seems weak. I’ll stick at AMBER though, as it’s now well-funded, but shares would have to more than halve for me to even consider investing here. Good luck to bulls, I hope the company delivers forecast-busting results!

See what our investor community has to say

Enjoying the free article? Unlock access to all subscriber comments and dive deeper into discussions from our experienced community of private investors. Don't miss out on valuable insights. Start your free trial today!

Start your free trialWe require a payment card to verify your account, but you can cancel anytime with a single click and won’t be charged.