Good morning from Paul!

I'm pushed for time today, as I have to drive from Bournemouth to Brighton this afternoon for a (not dirty) weekend away - I'm doing more UK mini-breaks with mother, brother, nieces & nephews, etc, in AirBnB's. Doesn't look like we'll be basking in the sun on Brighton Pier (LON:PIER) - more likely trying to avoid being swept overboard in gale-force winds! I'll also attempt to record the weekend podcast early too, so let's crack on!

This weekend's podcast has landed early! Here's the web link. It's also available on the main podcast services. A more positive tone this week, and some comments about market doldrums & keeping your pecker up!

Explanatory notes -

A quick reminder that we don’t recommend any stocks. We aim to review trading updates & results of the day and offer our opinions on them as possible candidates for further research if they interest you. Our opinions will sometimes turn out to be right, and sometimes wrong, because it's anybody's guess what direction market sentiment will take & nobody can predict the future with certainty. We are analysing the company fundamentals, not trying to predict market sentiment.

We stick to companies that have issued news on the day, with market caps (usually) between £10m and £1bn. We usually avoid the smallest, and most speculative companies, and also avoid a few specialist sectors (e.g. natural resources, pharma/biotech).

A key assumption is that readers DYOR (do your own research), and make your own investment decisions. Reader comments are welcomed - please be civil, rational, and include the company name/ticker, otherwise people won't necessarily know what company you are referring to.

What does our colour-coding mean? Will it guarantee instant, easy riches? Sadly not! Share prices move up or down for many reasons, and can often detach from the company fundamentals. So we're not making any predictions about what share prices will do.

Green (thumbs up) - means in our opinion, a company is well-financed (so low risk of dilution/insolvency), is trading well, and has a reasonably good outlook, with the shares reasonably priced.

Amber - means we don't have a strong view either way, and can see some positives, and some negatives. Often companies like this are good, but expensive.

Red (thumbs down) - means we see significant, or serious problems, so anyone looking at the share needs to be aware of the high risk. Sometimes risky shares can produce high returns, if they survive/recover. So again, we're not saying the share price will necessarily under-perform, we're just flagging the high risk.

Summaries

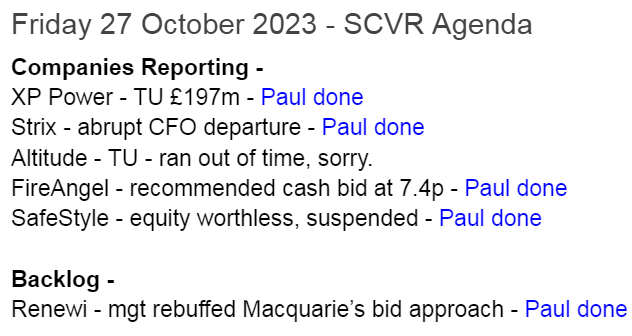

Renewi (LON:RWI) - down 18% to 540p y’day (£434m) - No takeover bid - Paul - AMBER

Investment giant Macquarie had previously (28 Sept) announced that it was minded to offer 775p for this waste recycling group, but that management had rejected its approach. It updated yesterday that, due to continuing rejections from Renewi management it won't now be bidding for the company. The share price has now fallen to 30% below Macquarie's indicated price, so management have some explaining to do, as to why they rebuffed what struck me as a fair deal that would have allowed shareholders to exit with a decent premium.

Fireangel Safety Technology (LON:FA.) - Recommended takeover bid at 7.4p

What a turn up for the books here! Shareholders are bailed out by a trade buyer from Singapore (already holding 17.5%) which has announced a 7.4p cash takeover offer, recommended by management. This is a cracking premium of 252%, which I imagine shareholders will gratefully accept, since this serial under-performer and diluter looked to be heading towards zero. Bear in mind it peaked at c.300p in 2015.

Safestyle UK (LON:SFE) - suspended.

Another serial under-performer that looked to be heading to zero. No white knight has been found here, not even Pat Butcher's mob are interested in the equity! Shares are now suspended, and it confirms this morning that there's unlikely to be any return for shareholders. That's that then.

Strix (LON:KETL) - down 3% to 57p (£121m) - Corporate Update - Paul - RED

CFO sudden departure concerns me. I review the other points that concern me - excessive bank debt, covenant relaxation required, awful balance sheet with negative NTAV, lots of cash wasted on dubious acquisitions and capex, and a close connection with China. Good luck to holders, but it's definitely not one I would want to go near.

XP Power (LON:XPP) - up 9% to 1094p (£216m) - Q3 Trading Update - Paul - RED

Market is relieved at some signs of things stabilising/improving at this troubled company. It's taking self-help measures to tackle excessive debt, but talks with the bank on covenants have not yet been finalised. Sounds like there's a hint about a possible placing too? So I'm steering clear until the finances have been repaired.

Paul’s Section:

Renewi (LON:RWI)

Down 18% to 540p y’day (£434m) - No takeover bid - Paul - AMBER

Renewi plc (LSE: RWI), the leading international waste-to-product company…

Investment giant Macquarie announced on 28 Sept 2023 that it had proposed a cash takeover at 775p to Renewi, but Renewi management rejected this approach as undervaluing the company.

It seems that Renewi management have continued to rebuff Macquarie’s approaches, so they announced yesterday that they’re not now intending to bid for Renewi, causing an 18% drop in share price. It sounds like they might have been prepared to pay more than 775p too -

Macquarie confirms that, following multiple attempts to engage with Renewi's Board, including a revised proposal, all of which were rejected, it does not feel it is in an informed position to make an offer for Renewi.

So here we are with the share price now back down to 540p, or 30% below the price Macquarie initially indicated.

Paul’s opinion - I thought 775p was a good offer for Renewi - a highly indebted company with rather patchy performance, and very low margins.

Maybe shareholders need to quiz management about what they plan to do, to create equivalent or better shareholder value, since the share price is now a long way below the proposed offer.

We were discussing in the reader comments yesterday, as to what approach to take when shares shoot up on a takeover approach. I sometimes like selling half immediately, to hedge my bets. That’s particularly the case when it’s not actually an agreed bid (as in this case), just a suitor wanting to bid, which has been rebuffed by RWI management.

Do we have any RWI holders in the house? If so, what’s your view? Did you bank any profits after the 28 Sept announcement of the bid approach? Are you happy for the company to remain independent, or annoyed that management rejected the bid premium?

I wonder if bid approach(es) might resurface? It’s an unusual business, there’s nothing on the UK market similar to Renewi that I’ve seen anyway. And a previous waste recycling company, Augean, was taken out by a bidder, so this type of company does seem attractive to buyers.

Strix (LON:KETL)

Down 3% to 57p (£121m) - Corporate Update - Paul - RED

Strix Group Plc (AIM:KETL), the AIM quoted global leader in the design, manufacture and supply of kettle safety controls and other complementary water temperature management components, announces a corporate update covering the planned CFO retirement and leverage ratio covenant relaxation.

This is odd. It says above that the CFO’s retirement is “planned”. Then it says this contradictory phrase -

Strix announces that after over twelve years with the business, Raudres Wong, Chief Financial Officer ("CFO") has advised the Board of her intention to retire as CFO, effective immediately.

If it was planned, then surely she would have previously advised of her intention to retire? I’ve done a quick search of the last few RNSs, and I cannot find any reference to the CFO planning to retire. Can I ask if any shareholders here were aware that the CFO was intending to retire, and whether this had been previously announced, as I might have missed it? So far (at 08:26) only a 3% drop in share price suggests this has not caused a panic amongst shareholders.

A NED has taken over as CFO temporarily whilst they look for a replacement. Again, not something that happens when a departure is planned - when it’s done the other way around - the replacement is found, then the incumbent does a handover period, then retires.

Why does this matter? I don’t like an abrupt departure of a CFO, because it can be a sign that something’s wrong (or Wong, in this case!)

She is thanked, and provides her own pleasant quote, wishing the company well.

Debt covenant - is relaxed, for Sept 2023, which seems strange as that’s retrospective. It does however reinforce what we already knew - that Strix has taken on too much bank debt (used to fund divis, heavy capex, and dubious acquisitions) . It confirms again today that debt reduction is a priority. Yet it’s still paying (reduced) divis. I think divis should be stopped altogether (and usually are), at any company which is struggling with excessive debt. I’m surprised the bank let it pay divis at all, considering a covenant relaxation was necessary. The H1 divi is 0.9p, down from 2.75p LY H1.

Paul’s opinion - I don’t like this share. I’ve raised concerns about its accounts in the past, and generally I avoid anything with close connections to China, due to the terrible history of China stocks on AIM back in c.2015 (almost all of them turned out to be frauds). Remember Camkids, and Naibu (whose Directors disappeared). There’s still stuff about Chinese frauds in our archive here. I put a blanket view of “I wouldn’t buy any of them” in my reports here, which turned out to be a very good move! The discounts to net cash, and super-low PERs did suck in some investors though, but the trouble was that none of the figures were real! There’s a fascinating article I wrote here in Feb 2014 about Chinese frauds, and also interesting that back then we were worrying a lot about the Chinese real estate boom bursting, which is a similar concern to the present day.

I’m not saying Strix is necessarily fraudulent. It passes two of my “probably genuine” rules, (1) it’s been listed for a long time, since Aug 2017, and (2) it’s paid decent divis over the years. I just don’t like a lot of exposure to China.

Also my concerns over its accounts are that there doesn’t seem much genuine cashflow, once finance costs and capitalised development spend are taken into account.

The balance sheet is heavily negative NTAV, with way too much debt.

Overall then, why would I want to get involved, when I can take my pick for higher quality, more soundly financed companies on cheap ratings? We’re spoiled for choice at the moment, so we don’t have to guess, or take any unnecessary risks at all.

Strix ran up the debt making a series of peculiar acquisitions, and heavy capex, which I don’t think have added value.

If I’m not 100% happy with the accounts, then I decline to invest, which is my view here. Good luck to holders, let’s hope it works out for you.

Looking back at our previous notes, I’ve viewed it as RED (due to high debt, and the accounts), whereas Graham is more lenient at AMBER, so it depends who is writing the report on the day.

I’m going to stick with my RED view, mainly due to the excessive bank debt, signs of stress with a covenant relaxation being required, that big divis are now a thing of the past, and that I think management have wasted a lot of cash on acquisitions and capex, funded by debt. So it’s definitely not for me. What looks like an abrupt CFO departure today, is another reason to steer clear for me. Obviously I’m happy to correct that if it transpires that the company had previously mentioned the CFO departure.

XP Power (LON:XPP)

Up 9% to 1094p (£216m) - Q3 Trading Update - Paul - RED

XP Power, one of the world's leading developers and manufacturers of critical power control components to the electronics industry, is today issuing a trading update covering the third quarter, and October to date, as well as detailing the significant actions being undertaken to reduce costs and preserve cash.

This previously looked a really good company, but it took on too much debt (which we warned about in Jan 2023), and got embroiled in an expensive $40m legal case.

The bigger bombshell happened on 2 Oct 2023, when it warned on profit, and flagged a potential bank covenant breach, causing shares to collapse from c.2400p to below 800p at one point.

There’s been a modest recovery in recent weeks, and as you can see, the market has reacted positively to its Q3 update today.

It sounds as if trading has at least stabilised -

Revenue in the third quarter was £75.1m (2022: £79.4m) with operating profit slightly ahead of our prior expectation due to a better outturn in September. Trading in October has been at least in line with our expectation. Our full year expectations are unchanged.

Although this is the context for today’s in line update -

Other points -

Cost reduction & cash preservation measures taken, £8010m benefit for FY 12/2024.

Inventories being reduced by £10-20m over the next 2 years, to free up more cash.

Other measures to preserve cash, such as no divis, minimum capex, etc.

Bank talks ongoing, and are they hinting at a placing here I wonder? -

The Group is also in advanced and constructive discussions with its lending banks regarding future covenant requirements and other near-term actions to strengthen the balance sheet. These discussions are proceeding as planned and we will provide a further update shortly.

Paul’s opinion - it’s had a nice bounce from the recent disastrous lows, but it’s clear that XPP is not out of the woods yet. So personally, I won’t be investing due to the risk of dilution in a discounted placing perhaps. Given the ongoing financial risk, it has to remain at RED for the time being. Once funding talks are resolved, and the position is clearer, then I’m happy to look at it again with fresh eyes. The purpose of our RED view is to flag up risk. You can make your own minds up whether you are happy or not to take that risk.

See what our investor community has to say

Enjoying the free article? Unlock access to all subscriber comments and dive deeper into discussions from our experienced community of private investors. Don't miss out on valuable insights. Start your free trial today!

Start your free trialWe require a payment card to verify your account, but you can cancel anytime with a single click and won’t be charged.