Good morning!

There seems to be a problem this morning with live prices, and news. The usual site many of us use for RNSs doesn't seem to be working. When this problem occasionally arises, I go direct to the London Stock Exchange website, to read RNSs. Although its user interface is pretty lousy.

For alternative sources of live prices, which work nearly all the time, I use a watch list on IG or Spreadex accounts.

By the way, if you want a good laugh, then click here to see a short video of my epic fail on this holiday, trying to jump into a rubber ring in the swimming pool. Apparently it's already going viral on Facebook! You've Been Framed next possibly?! Some serious dieting is needed once I get back to the UK.

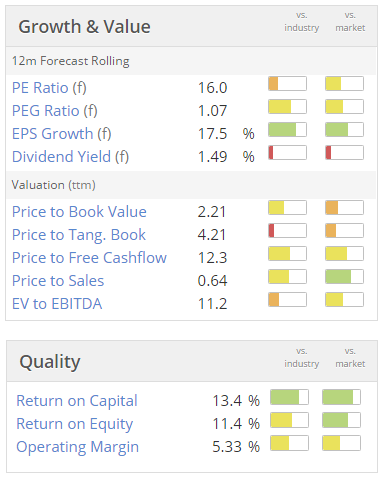

Braemar Shipping Services (LON:BMS)

Share price: 370p (down 8.9% today)

No. shares: 30.1m

Market cap: £111.4m

Trading update (profit warning) - a fair bit of detail is given, but the crux is that it's a profit warning;

...while the results for the year ending 28 February 2017 will be materially lower than 2016, the structural management changes and cost reduction measures we have put in place (the costs of which will substantially fall in the first half of the current year) will result in an improvement in business performance.

The market seems to have reacted gently to this profit warning, perhaps because the company says (above) that it's already taken action to improve performance.

The StockReport shows that consensus earnings forecast is currently for a 5.4% rise this year. So the company now saying it will be "materially lower" than last year - materiality is usually 10% or more - means this is quite a significant downturn in profit.

Dividends - the forecast dividend yield is now about 7%. So if the divis are held at 26p, where they have been static for the last 6 years, then this could be a good opportunity to pick up a high yielding share.

The downside risk is that the divis could be cut. In my experience, a static dividend payout for several years is indicative of a company that is struggling to maintain that level of payout, and sooner or later a cut may happen. Or re-basing, as management usually call a cut!

It's crucial to consider the balance sheet strength at high yielding companies, to see what capacity the company has to continue paying generous dividends. In this case, Braemar has a fairly strong balance sheet with net cash, so that's encouraging.

At a guess, I would be inclined to factor in a 50% possibility of the divi being cut by perhaps 20-50%, to be on the safe side, when valuing this share.

My opinion - I don't understand the dynamics of the shipping industry well enough to be able to give a firm view on this. Profits have been quite volatile in the past, and today the company mentions various negative factors in the sector - e.g. over-supply of dry cargo ships, and falling demand for tankers. Also the oil & gas sector doldrums is hurting Braemar's technical division.

To invest in this company, I think one would need to understand the sector well, and be able to anticipate a positive turning point in freight rates, etc.. At that point in time, there could be good upside here, as it looks a fundamentally sound company.

Decent divis are also an attraction, if they are maintained.

Overall then, it might be worth a closer look, although I imagine EPS forecasts for this year will probably be coming down from 33p to perhaps 25-28p. So with the shares at 370p, it doesn't currently look a particular bargain (that's a PER of about 13-15, based on my guesstimate of likely EPS this year).

So it all hinges on whether you think this year's earnings are the low point (in which case the share might be a good buy), or whether there's more bad news to be expected further down the line (in which case the shares are probably best avoided). I don't have any idea which it is, so I'll pass on this one.

IG Design (LON:IGR)

Share price: 236p (down 2.3% today)

No. shares: 62.3m

Market cap: £147.0m

(at the time of writing, I hold a long position in this share)

Trading update - a solid, in line update today from this maker of gift packaging & related products. As it has a 31 Mar year end, today's update is for Q1 of the current year ending 31 Mar 2017.

Key points;

- Q1 trading in line with management & market expectations, both sales & order book.

- "opportunities for incremental growth" in H2 - sounds promising. Presumably they mean in excess of existing forecasts?

- Record order book.

- Growth from increased international geographies - e.g. sales in Mexico have doubled.

- Growth from new products too (e.g. party ware)

- US acquisition (Lang) has "hit the ground running"

Outlook comments sound bullish to me, which makes me wonder whether broker forecasts might be raised as the year progresses. Companies don't usually sound this bullish early in their financial year.

Paul Fineman, Group CEO, commented:

"The Group has made a most encouraging start to the year with our order book at record levels and an excellent blend of sales activity across categories, regions and brands, both with new and existing customers.

"We are also pleased to have 'hit the ground running' with the integration of our new business in the US - Lang Companies Inc. Early indications are positive and we are confident of future growth opportunities. This is particularly pleasing alongside the robust organic growth that we are achieving throughout the Group."

Valuation - this share has risen strongly in recent months, which is reflected in a valuation that probably looks about right for now;

My opinion - this group is clearly on a roll, and I'm sitting tight on the position I hold.

Shares don't rise in a straight line forever, so I think it would be healthy for this one to pause for breath, maybe even drop a bit on profit-taking.

Longer term though, this share very much looks to me as if it's heading up, because the group seems to be firing on all cylinders. Management are highly rated here, by several fund managers and serious private investors that I've spoken to, although have not met them myself.

So in my view, this is a nice long-term share that's probably heading higher, although maybe not immediately.

A couple of quickies now to finish off with:

Pressure Technologies (LON:PRES) - it's another profit warning. Key points;

Some positive developments, e.g. order intake for alternative energy, division - which they expect to be a major profit generator from 2017 onwards.

Overall trading continues to be in line with expectations.

However, a number of factors (contract delays, R&D spending, and a legacy issue) will together have a material impact.

FY result will now be a loss.

Bank covenants will be OK in Oct 2016, but cashflow sounds tight.

My opinion - I'm tempted to nibble here, but the balance sheet is too precarious for my liking - I'm worried about bank debt, and the risk of it having to do a discounted placing.

That said, there seem positive signs for the future, so the market might begin to see the glass half full at some point perhaps?

I think they'll have to pass on the divis for a while, given that bank covenants sound too close for comfort. So I would not rely on there being any dividend yield at all for the next year or two, possibly. This is definitely a situation where I would not hang my hat on the apparently high dividend yield, since it's likely to be cut, or passed altogether in my opinion. I actually think it would be quite reckless of management to continue paying divis in the current circumstances.

At some point though, this share could start to look interesting, so I'm going to keep an eye on it. If they fix their balance sheet, with a fundraising, then I would have the confidence to buy some.

Satellite Solutions Worldwide (LON:SAT) - an interesting company - which is doing a roll-up of fragmented small companies in the satellite broadband space. I like management here. However, the business model is cash hungry. It's not yet profitable, and needs to keep doing equity/debt fundraisings to buy more bolt on businesses. The trouble is also that customer acquisition involves up-front costs, then a long tail of revenues. So again, cash hungry.

It reached EBITDA breakeven in Jul 2016. I think this company will succeed, even though it's still a bit jam tomorrow. The valuation strikes me as a tad too warm, for where it has got to so far.

That's all for today, see you tomorrow!

Regards, Paul.

(usual disclaimers apply)

See what our investor community has to say

Enjoying the free article? Unlock access to all subscriber comments and dive deeper into discussions from our experienced community of private investors. Don't miss out on valuable insights. Start your free trial today!

Start your free trialWe require a payment card to verify your account, but you can cancel anytime with a single click and won’t be charged.