Good morning! Thank you to everyone who ventured down to Brighton last night, for my third investor evening, it was great fun, slightly marred by a very noisy restaurant who serve nice food, but are utterly devoid of common sense - i.e. putting other diners in the area directly next to our enclave, where they disturb us to the maximum extent, and it can't be terribly nice for those other diners either, hearing an unsolicited lecture about aircraft leasing when they are trying to enjoy a hilarious, shrieky night out with their friends.

Work has already started on finding a better venue.

The FD of Avation (LON:AVAP) gave an interesting talk last night in Brighton about aircraft leasing. One point which stuck in my mind is that he said the lower oil price is increasing the value of older aircraft, since airlines are now less concerned about fuel efficiency. Also, that once hedging is stripped out, the lower oil price is having a dramatically positive impact on the profitability of airlines. So whilst investors have perhaps been preoccupied with Ebola, a much more positive factor is working its way through the system, in lower fuel prices. So arguably this might be a good time to think about aviation stocks perhaps? Interesting also to look at the rapid, relentless growth in air travel over many years.

I haven't bought any stock as yet, but Avation is on my watch list now, and is something I might dip my toe into on the next big red day - BLASH and all that!

It's quiet again for results today, I must make a note to schedule a holiday for late October next year.

Quartix

Admission to AIM - FinnCap seems to have successfully got away this IPO, for a telematics company. My last interviewee, Edward Roskill, mentioned this stock as one to watch on Sunday evening's podcast. People seem to like these podcasts, so I'll keep doing them most weekends, they're great fun. I loved the Tweet from MrC, saying that it was like listening to two surgeons chatting whilst they dissect a body!

Plexus Holdings (LON:POS)

Share price: 253p

No. shares: 84.9m

Market Cap: £214.8m

This company's description is as follows;

The Company markets a patented method of engineering for oil and gas field wellheads and connectors, named POS-GRIP which involves deforming one tubular member against another within the elastic range to effect gripping and sealing.

My first thought is whether the company has been impacted by the drop in oil price, and hence reduction in capex from oil companies?

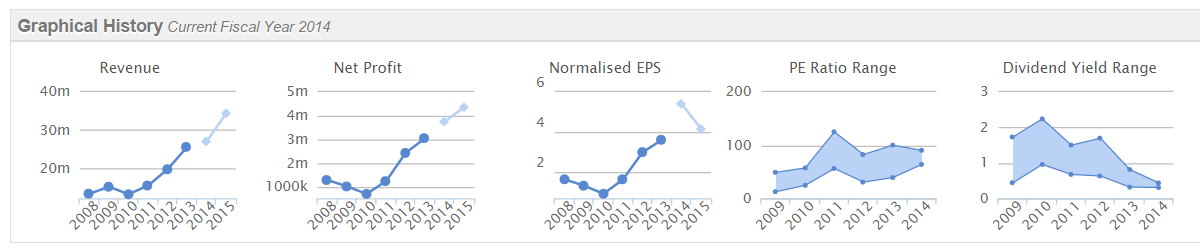

Final results out today look pretty good. Turnover is up 5.7% to £27.0m, and pre-tax profit is up 25.9% to £5.4m - note the high profit margin there too.

Valuation - the price looks very high based on these reported numbers. Going by the reported EPS of 6.0p, the PER is 42.2, which clearly factors in a fair bit of continued growth that investors are paying up-front for.

Outlook - I don't understand this sector at all, so here is an excerpt from today's statement;

In summary our key strategic goal over time is for POS-GRIP wellheads, whether for surface or subsea exploration and production applications, to become a new industry standard which is recognised as a superior method of engineering that delivers a quality of metal seal that cannot be matched by conventional wellhead technology. The science based driver for our ability to achieve this goal is simply that unlike conventional wellhead designs available from all other wellhead suppliers, Plexus is uniquely able to deliver and maintain enough interface stress between the perimeter of a metal seal and the wellhead bore, within Hertzian Contact Stress limits, throughout the life of the well. In line with this strategy, we are beginning to actively explore how best to exploit this simple message with potential partners worldwide.

My opinion - this share looks expensive on the reported figures today, but if they have a strong growth product, then who knows, it might end up being cheap if the company grows profitability to multiples of the current level? For anyone who understands this sector, this company looks potentially interesting in my view, and worthy of deeper research perhaps. I like growth companies which are already decently profitable, which this is.

As the graphs below show, the trend on sales & profitability looks positive. Is it worth the £215m price tag? That's the big question.

Broker forecast was for 5.4p, so at 6.0p the company seems to have come in ahead of forecast.

Photonstar Led (LON:PSL)

Share price: 3.25p

No. shares: 143.8m

Market Cap: £4.7m

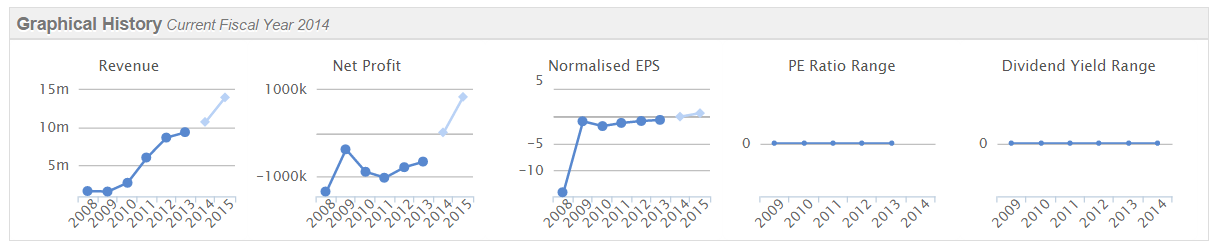

Profit warning - oh dear, not one of my better ideas this one. I held a few of these in my long-term portfolio, but have bitten the bullet & chucked them out today.

Here is the main part of today's profit warning;

The Group now expects sales of fixed white lighting products for the year to be lower than indicated, due to several large lighting domestic and export contracts being delayed into 2015.

The light engines business has also experienced a slow-down in sales with pressure on margins. The Board has now decided to commit no further development resources to this area of business and focus its efforts on expanding the Halcyon product range more rapidly. The Board believes this strategy will offer a greater return on investment in 2015.

The Board now expects that revenues for the year ended 31 December 2014 will be below market expectations which will result in a loss for the year.

Although the message is mixed, in that the company does make positive noises about new products;

As announced on 22 October 2014, PhotonStar is now shipping the HalcyonPro lighting system - the first wave of Halcyon products (servers, lamps and sensors). The Group is seeing significant demand for its connected lighting products and is realigning its sales partners and channels to reflect this. The formal launch of the Halcyon system with additional products, accessories and connectivity needed to deliver a fully connected lighting platform will take place at Lux live on 19 November 2014.

My opinion - it's not clear from the above statement how bad the loss will be for the year, so it's impossible to value the company reliably at the moment. I've lost confidence in the company, so would rather just chuck them out and move on. One to chalk down to experience I think.

I had hoped that new products might transform the company, but there's no sign of that at the moment, and I wonder whether the company might need to come back for more cash, after the amount raised earlier this year wasn't large.

Its track record (see below) is such that the company must be getting close to drinking in the last chance saloon, given that forecasts for this year & next are now looking too optimistic.

See what our investor community has to say

Enjoying the free article? Unlock access to all subscriber comments and dive deeper into discussions from our experienced community of private investors. Don't miss out on valuable insights. Start your free trial today!

Start your free trialWe require a payment card to verify your account, but you can cancel anytime with a single click and won’t be charged.