Good morning! Another quiet day for small cap news, which is handy as that gives me time to properly research Avation (LON:AVAP) ,whose FD is visiting my Brighton Investor Group tonight to give a talk about the company. We're fully booked, although I suppose one or two more could be squeezed in, although it's awkward because our usual section of the restaurant comfortably seats about 25, and when we go over that we get into a halfway house situation, where we over-spill, but not enough to have the entire restaurant to ourselves. Ah well, I'm sure it will be fine. It's really good that we've managed to generate enough interest to establish an investor group on the south coast, so thank you to everyone who supports these evenings.

Teg (LON:TEG)

It's bad news for shareholders here I'm afraid, as the shares have been suspended today, with the dreaded phrase highlighted below;

The Group has requested the suspension of trading of its shares on AIM pending clarity on its financial position.

As @MrContrarian correctly said this morning on Twitter, "Companies rarely recover from this stage."

It's usually a good idea to look at companies which go bust (this hasn't yet, but it looks on the verge of it) to check whether you spotted the warning signs. In this case, it's obvious that things were going badly wrong. The narrative to the interim accounts published on 30 Sep 2014 made it clear that the company needed additional funding.

Also, the Balance Sheet shows that cash had almost run out, plus there was debt on top of that. Yet again though, the big "tell" is excessive debtors, which we discussed yesterday. In this case, debtors of £8.5m (compared with only £5.6m turnover for the six months to 30 Jun 2014) clearly indicated that something was badly wrong - if customers can't or won't pay for goods/services that have been billed, then you run out of cash, which seems to be what's happened here.

The cashflow statement also shows a worsening position.

I see that Peter Gyllenhammar owns 20.1% of the company, so maybe he'll sort out some kind of rescue refinancing? It's difficult to imagine that shareholders would be prepared to stump up more cash, without agreement first being reached with customers over the disputed contracts. Some sort of compromise deal to partially settle outstanding disputed amounts sounds the best way forwards, if there is a way forwards. Good luck to everyone involved, I hope a solution is found.

As you can see from the chart below, some shareholders had the sense to get out at any price after the 30 Sep 2014 announcement.

Sensible screening of the Balance Sheet and Cashflow statements should mean that you never have a company in your portfolio which goes bust. I've made it my mission to never again hold shares in a company that goes bust, as it should be possible to avoid these situations altogether.

Why do people continue holding when something has gone disastrously wrong? Usually because hope overcomes logic, and/or because the losses have already been so heavy, you can't bring yourself to crystallise the losses.

If a company still has enough cash to operate, then it can trade its way out of trouble. The death spirals happen when inadequate cash resources exist - hence why Balance Sheet testing is so important. Also just because something is shown on the Balance Sheet as an asset, doesn't necessarily mean it has any value - a debtor is worth nothing unless & until the customer has agreed to pay it.

Utilitywise (LON:UTW)

Share price: 289p

No. shares: 74.5m

Market Cap: £215.3m

This is a utility cost management consultancy, for corporate customers - to get them better deals on electricity, gas, etc.

Final results - for the year ended 31 Jul 2014 issued today look good at face value.

Organic growth is very impressive - 62% growth in like for like revenues, which has come from adding more headcount. Total revenue grew 93% one acquisitions are included too.

Profit before tax is up a highly impressive 76% to £13.1m, and headline diluted EPS is up 58% to 13.4p.

Historic valuation - this pace of growth won't be cheap, and sure enough the PER is 21.6 based on that 13.4p figure. Although one could argue that such a PER is cheap, considering how strong the growth is, if that growth is likely to be maintained. So let's have a look at the outlook statement to get a steer on future growth prospects;

Outlook - this is somewhat vague;

The new financial year has started well, in line with management expectations. The increasing diversity of our offering and commitment to further broaden our products and services auger well for the future. Our plans remain to continue to grow headcount to support organic growth; we have successfully integrated our recent acquisitions and we continue to show the strength of our proposition with the value we add to our customers.

We are well placed to take advantage of opportunities as we continue to grow.

Therefore, in the absence of anything more concrete, I'll just assume that broker consensus forecast for the current year are realistic.

Future valuation - another big jump in EPS is forecast for this year (ending 31 Jul 2015), to 17.6p, so that would bring down the PER to 16.4, which looks a sensible valuation to me.

Dividends - A big increase in the dividend is good to see. A 2.7p final divi has been announced, taking the full year payout to 4.0p (up 54% on prior year), a not very exciting yield of 1.4%, but it is at least growing fast.

My opinion - as mentioned before, I have some concerns about this company. The main one is that profits may prove to be unsustainable in the long run.

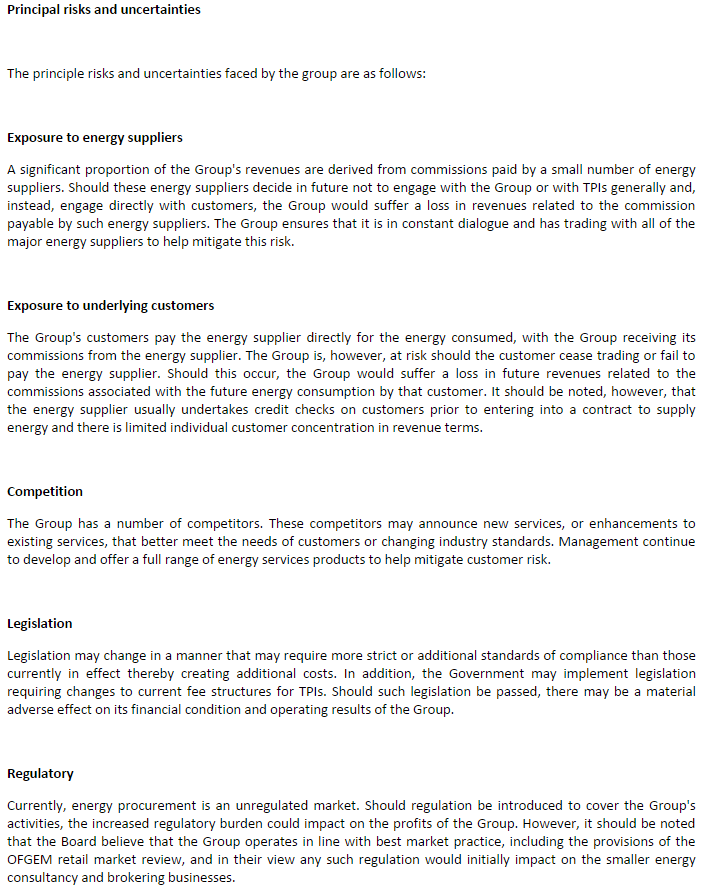

It's worth reading the "principal risks and uncertainties" section of today's announcement, which I've put into a screengrab on the right (click to enlarge).

The following risk in particular shows that the company is on potentially shaky ground;

"A significant proportion of the Group's revenues are derived from commissions paid by a small number of energy suppliers. Should these energy suppliers decide in future not to engage with the Group or with TPIs generally and, instead, engage directly with customers, the Group would suffer a loss in revenues related to the commission payable by such energy suppliers. The Group ensures that it is in constant dialogue and has trading with all of the major energy suppliers to help mitigate this risk."

There are also regulatory risks, although in my opinion the Govt won't usually interfere in commercial arrangements between companies, as opposed to consumer-facing companies.

These risks, combined with the very high profit margins being achieved by Utilitywise, make me feel that this company is probably making hay whilst the sun shines - i.e. arguably making super-normal profits. At some point the utility companies could move the goalposts, and suddenly this type of work could overnight become a lot less lucrative. I've seen that happen in other similar areas in the past, hence generally why I avoid this type of company unless it's dirt cheap, which this isn't.

Balance Sheet/ Revenue recognition - another concern I have here is that the Balance Sheet shows a debit entry of £13,068k within non-current assets (and presumably an additional amount will be included within current assets, inside debtors), relating to "accrued revenue". So the double entry here would be Cr turnover (i.e. goes straight through to profit), and Debit accrued revenue on the Bal Sheet. No cash has been received for this part of turnover, which is quite material. Instead the cash will be received over time, indeed over a year in the future, for the £13,068k within non-current assets.

I'm not keen at all on this accounting treatment. It may be perfectly permissable, but it seems to me that the company is anticipating future profits, and booking them in advance, which is never a good thing. Personally I would reverse out these entries, and account for profit as the cash is received. That would greatly reduce profit of course.

Another slightly odd item on the Bal Sheet is that the company has increased loans from £5m to £6m in the year. Why would they do that, when the company also reports £15.8m in cash? Surely that is inefficient in terms of interest cost? It just makes me wonder whether the cash figure has been window-dressed for the year-end, and might be a lot lower throughout the year (which would explain why the company has increased its borrowings).

Director Selling - check out the huge scale Director selling, they've banked about £52m selling shares all the way up from 75p to 290p. True, Directors also spent about £4m buying shares in a flurry from Nov 2013 to Feb 2014, but the weight of money overall is massively on the selling side. That's another big red flag to me, and reinforces my view that the company is in a sweet spot for profitability which may not last long term.

Conclusion - I don't like it. There are too many red flags, the accounts look odd to me, and I'm not at all convinced that profits will be sustainable in the long run. Combined with a high valuation, that makes these shares uninvestable in my opinion. It's just an opinion, and I fully expect to get shot down in flames by existing shareholders in the company!

Macfarlane (LON:MACF)

Share price: 35p

No. shares: 124.6m

Market Cap: £43.6m

I spotted an article in the Scottish press today saying that this company has come up with the idea of making packaging materials for online sales, which fit through a standard sized letterbox. This seems such an obvious idea, but appears to have eluded the entire packaging industry until this point. Therefore such a cutting edge innovator is worth investigating as a possible investment.

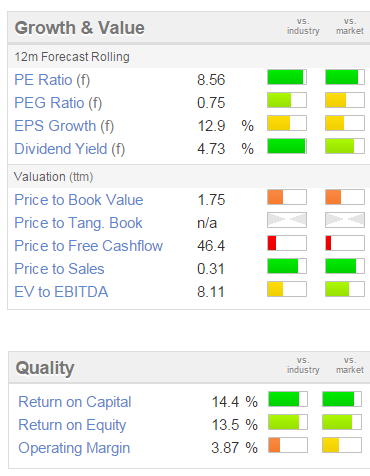

It scores quite well on the Stockopedia value & two of the three quality scores too:

The company did a small Placing in Sep 2014, to supplement enlarged bank facilities, and has done an acquisition which looks sensible in terms of price paid, and terms (an earn-out if profit increases by 40%).

My interest waned when I worked out the that gearing is rather too high for my tastes, and the company has a significant pension deficit, and has just paid £2.5m into its pension fund, suggesting that more will be required to play the £13.2m deficit at 30 Jun 2014.

Although the dividend yield looks good. I note that these shares have come down from a peak of 49p in May 2014, to 35p now, but on balance the debt & pension deficit put me off.

Has anyone else looked at this one at all? I'd be interested in any views on it.

Fitbug Holdings (LON:FITB)

Share price: 7.26p

No. shares: 168.5m

Market Cap: £12.2m

This has only just caught my eye - the shares are up 89% today on an RNS that its product (a wearable fitness device) is to be sold at major US retailer Target, and Sainsbury's. Impressive stuff.

Looking at the last set of results, the company is clearly insolvent, and being propped up with loans. So I'd say it's a racing certainty that a Placing will take place to refinance the Balance Sheet now that there is some good news out.

Also note that the company is taking legal action against a competitor product called FitBit.

As a speculation, it might have further to go, who knows? Check this out for an insane chart!! A 15-bagger in two days!!!

On that note, I shall sign off. I'm looking forward to hosting tonight's Brighton investor evening, so see some of you there, mine's a Peroni!

Regards, Paul.

(of the companies mentioned today, Paul has no long or short positions.

A fund management company with which Paul is associated may hold positions in companies mentioned)

See what our investor community has to say

Enjoying the free article? Unlock access to all subscriber comments and dive deeper into discussions from our experienced community of private investors. Don't miss out on valuable insights. Start your free trial today!

Start your free trialWe require a payment card to verify your account, but you can cancel anytime with a single click and won’t be charged.