Good day!

I see Dialight (LON:DIA) is down again, to 409p at the time of writing (mentioned in yesterday's report). It just shows that, when something goes wrong, selling quickly is a good idea. This is where we private investors have a massive advantage over institutions - if anyone buys more than about 1% of a small cap, then when something goes wrong, they are left high & dry. They often can't sell, even if they want to. Whereas you and I can just ditch a bad company unceremoniously. OK it might mean taking a loss, but we live to fight another day, and can make up the loss on something else.

So my thought for the day is that forming an emotional attachment to a bad share, and hesitating over selling, is the biggest unforced error that most of us make. If/when something goes badly wrong, then ditching it on the opening bell is usually the best thing to do. I like to get my sell order into the market, and executed, whilst the institutions are still worrying about what to do, ahead of their first committee meeting of the day. I'm long gone by the time their sell orders come in, and smash the price. That's the theory anyway.

Apparently we're all meant to be terribly worried about China. I'm not. According to someone on Twitter, the UK exports less than 1% of GDP to China. Lower commodity prices makes everything cheaper, thus boosting a services based economy like the UK. So the way I look at things, investors in resources stocks might be getting massacred, but that doesn't affect me. It won't affect the number of conservatories that Entu are going to sell, nor the number of frocks that BooHoo shift. All in all, it's just background noise for a long-term UK small caps investor, in my opinion. There's always something that people fret about. Bottom line for me, if I hold good value shares in decent UK companies, then what the Chinese stock market does is completely irrelevant.

There's not much in the way of news today, hence the ramblings.

Somebody in the flats over the road (I'm in Islington) is obviously smoking a joint, as the pungent aroma of cannabis is wafting into my room. Who needs sniffer dogs when it stinks to high heaven like this?!

McColl's Retail (LON:MCLS)

Share price: 160p (up 1.3% today)

No. shares: 104.7m

Market cap: £167.5m

Interim results, 26 weeks to 31 May 2015 - this convenience store operator seems to have been successful in eking out a modest profit margin again, despite LFL sales being down by 1.9% against last year. Pre-exceptional operating profit came in at £9.6m versus £10.0m in H1 last year.

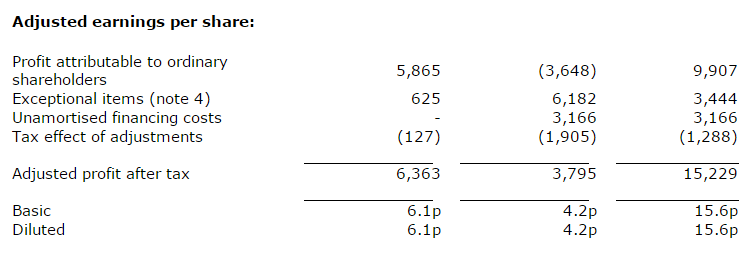

Adjusted EPS is up 45% to 6.1p, which seems odd - why would EPS be up, when profits are slightly down? It must be down to cost-cutting, which is mentioned in the narrative. Here is note 11, giving the reconciliation of adjusted to normal EPS:

Dividends - note that the interim dividend has been doubled, from 1.7p to 3.4p. That's impressive.

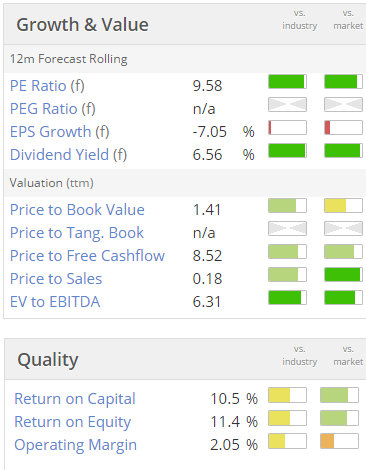

Valuation - the usual Stockopedia graphics are below, and as you would expect from this type of business, it's on a low PER, and pays a cracking dividend yield.

Balance sheet - looks bad to me. Net assets are £117.2m, but that includes intangibles of £141.8m. So write that off, and net tangible assets is negative, at -£24.6m. That's not necessarily a problem for a retailer, as they sell for cash, and get credit from suppliers, so retailers can operate fine with a relatively weak balance sheet.

However, in this case I am concerned about the level of debt. You have to be so careful with any business which was formerly owned by private equity ("PE"). In my view, PE is a scourge - they're parasites, who load up businesses with debt, in order to reduce taxable profits to as close to zero as they can get.

The sole purpose of PE is to make a profit buying and selling businesses, and they often leave a trail of destruction behind them, in my experience - businesses can be starved of capex, in order to generate short term profits, and they nearly always float the company back onto the market with far too much debt remaining.

Net debt has gone up here from £36.3m to £47.3m, but then the company also presents "underlying net debt" of £35.3m! That's a new one for me - underlying net debt!! A (sort of) explanation is given in note 10:

This makes me uneasy - it's reinforcing the reality that debt is too high, although I suppose being given an explanation for swings in net debt is helpful. I don't like this "certain..." debtors and creditors. Why can't they just say payroll, and money paid to us by the Post Office?! That would be my guess of what items have caused this issue.

It also flags up the problem with having a 26, and 52 week year end cycle, as opposed to calendar month accounting. If your major outgoings (e.g. payroll) is paid on the last day of the month, then the accounting periods need to reflect this. I had this problem back in my days as a retailing FD. I inherited calendar monthly accounting, but it was fiddly to get the cut-off right at month end, so in a eureka moment, I decided to alter the accounting to 4 or 5 weekly cycles (instead of calendar months).

It was a complete disaster - the 4-week periods were loss-making, and almost scared the bank into withdrawing our overdraft. Then every now and then a 5-week period would happen, and show a big profit. Then when it came to year end, if the 52 weeks ended before the 31st of the month, all was fine, because the payroll was paid on the 31st, so the year end on (say) 28th January, showed a big cash balance.

However, we had to do a 53 week period every now and then, which threw out all the comparatives, and suddenly the year end was on the 3rd February, just after payroll had been paid, so the overdraft was maxed out!

After a while, I realised that 52 or 53 week accounting was a complete nightmare, and went back to calendar months, as that meant that each month and year reported the same cashflow cycles. It seems to me that McColls need to have a think about this, and maybe switch to monthly reporting, instead of 4/5 week reporting.

My opinion - I can't shake off the feeling that this is a cigar butt business - squeezing out a small profit margin, but probably doomed to eventual failure.

With such a weak balance sheet, it should be conserving cash, not paying out big divis, in my view. You have to be so careful with high yield stocks, as they can often be dying businesses made temporarily attractive by a big divi yield. Remember that HMV paid out bumper divis until shortly before it went bust.

Having said that, McColls has done well to remain profitable, which suggests to me that they might be benefiting from reduced rents on lease renewals. Another issue to consider is the planned increases in Min Wage, which are likely to affect companies like McColls - with a profit margin this low, I imagine they are only paying Min Wage, or marginally above, in many locations. So a 3-4% annual rise will hurt. Wetherspoons were belly-aching about this recently, in their results statement.

Overall, I think this stock is high risk, and the big divi yield could lull people into a false sense of security.

InternetQ (LON:INTQ)

Share price: 300p (up 2% today)

No. shares: 39.9m

Market cap: £119.7m

Trading update - in my view, this company is almost a carbon copy of Globo, at least in terms of its accounts, if not its activities. In particular, the bumper profits reported never turn into cash, but instead the debits on the balance sheet just pile up into ever larger amounts - especially intangible assets and debtors. That's essentially a sign of fictitious profits, the way I look at things, which is confirmed by a negligible tax charge.

Every trading update is positive, so naturally today's is positive. The company says;

The Company has a strong pipeline with good visibility for the coming six months and is on track for even better growth in the historically stronger second half. The Company remains confident for full year results to be in line with market expectation

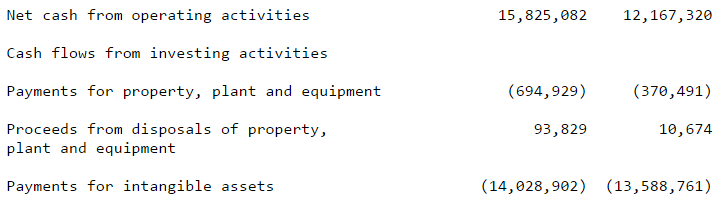

Cashflow - consider this small excerpt from the cashflow statement, showing what I consider to be the crux of things for calendar 2014 and 2013:

So in other words, if you're being kind, all the cash profits are re-invested into intangible assets. If you're being unkind, what this means is that they happen to call some costs "intangible assets" in order to by-pass the P&L, thereby creating fictitious profits.

I was reading up on Warren Buffett's shareholder letters whilst on holiday last week, and his approach cuts through all the nonsense. In his view, you can ignore costs if they are just (largely meaningless) accounting book entries, such as goodwill amortisation. However, you absolutely must not ignore business costs, of whatever kind - whether you capitalise them or not, a cost is a cost.

So a business such as this, which generates nothing in real cashflow, is not profitable at all, whatever the accounts purport.

Investment by Tosca - there was an interesting announcement on 9 Jul 2015, saying that Tosca has invested E17m to buy a stake in INTQ's Akazoo music streaming business. It says the post-money valuation is E104m, of which INTQ owns 69.1%, or E71.9m, about £50.9m.

This third-party validation of a key service of INTQ certainly strengthens the investing case. Although how this music streaming service is going to compete with Apple's new offering, and existing services from Spotify and YouTube, is the big question.

My opinion - overall, I don't think this company is profitable at all, but it clearly has some value, as it has been successful in securing outside investment into Akazoo. Therefore as a glamour stock, it might attract a high valuation if it can get people excited with big growth numbers perhaps?

It's definitely not for me, but as a complete punt, I would say this is nowhere near as bad as Globo.

(article in the process of being updated, pls refresh the page from time to time)

See what our investor community has to say

Enjoying the free article? Unlock access to all subscriber comments and dive deeper into discussions from our experienced community of private investors. Don't miss out on valuable insights. Start your free trial today!

Start your free trialWe require a payment card to verify your account, but you can cancel anytime with a single click and won’t be charged.