Good morning!

A quick whizz through this morning, as I have to head into London for meetings this afternoon.

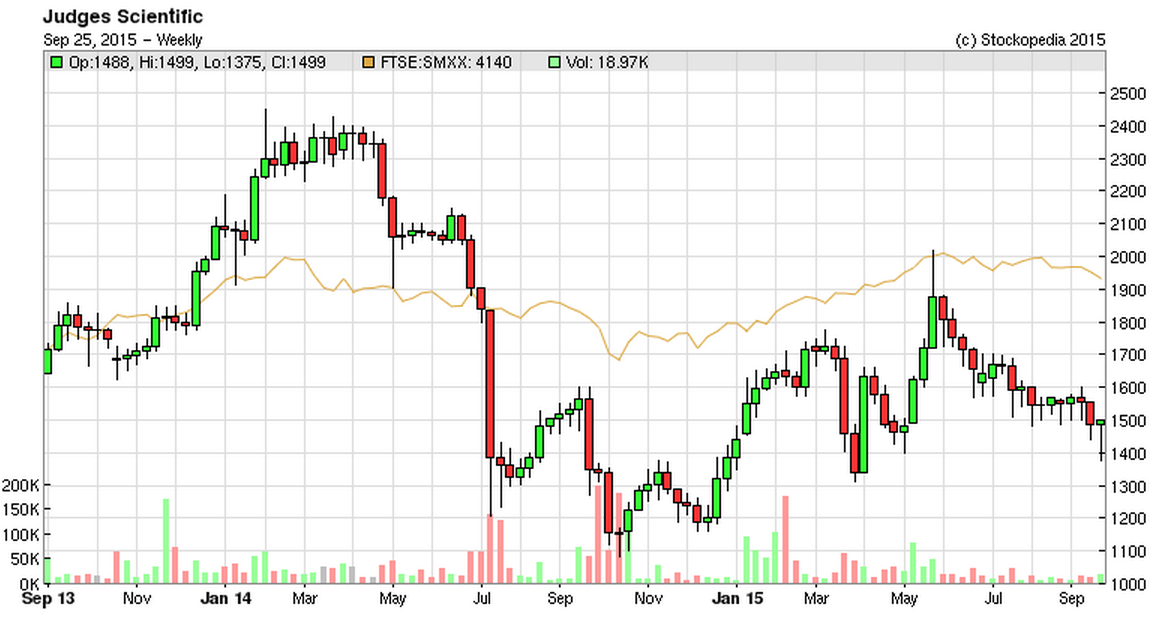

Judges Scientific (LON:JDG)

Share price: 1475p (up 2.6% today)

No. shares: 6.1m

Market cap: £90.0m

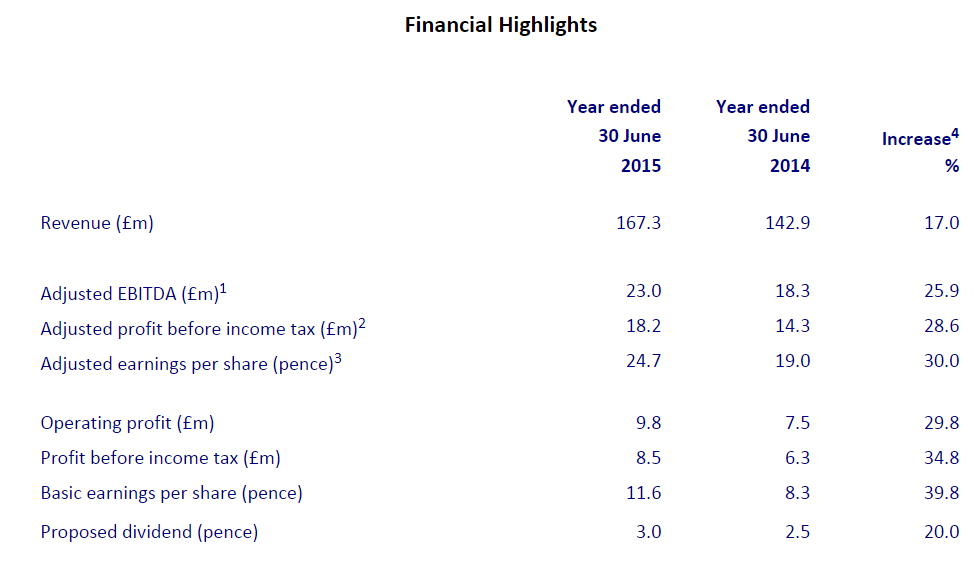

Interim results to 30 Jun 2015 - this is an acquisitive small group of scientific instrument companies. Results today look rather poor, with adjusted pre-tax profit down 18.5% to £3.3m, and adjusted EPS down 18.3% to 41.1p, despite turnover being up 13.7% to £24.9m (note that the profit margin is still good though, at 13.3% of turnover).

However, the outlook comments are more positive;

"These mid-year figures reflect the weak order intake experienced throughout much of 2014 and the first quarter of this year. I am pleased to report, however, that order intake in the last six months has shown a significant improvement which will bear fruit in the second half. Meanwhile, the acquisition of Armfield illustrates Judges' continuing ability to execute its growth strategy, utilising the Group's cash generation. As a consequence the Board remains confident in the ability of the Group to meet market expectations for the full year."

...The second half has commenced positively, aided by the strong mid-year order book. Organic order intake in the third quarter is well ahead of last year, albeit less buoyant than in Q2 2015. Overall order intake since the beginning of the year is consistent with the Group's sales budget and your Board remains confident in the ability of the Group to meet market expectations for the full year.

When assessing outlook comments, you have to think about the specific company, and how reliable/trustworthy the management are, based on what they have said & done before. Do they tell it like it is? (good). Or are they always bullish, but often disappoint? (bad). I've followed JDG for years now, and am very satisfied that management commentary can be relied upon as being truthful, and straightforward.

Also think about the outlook comments themselves. Is it a general fuzzy warm feeling they are expressing, with no specifics (bad)? Or are they giving facts & figures which justify optimism (good) - e.g. quoting order book figures, or increases.

So in this case, whilst I am usually sceptical of companies which have a bad H1, and promise to make it up in H2, in this case I'm inclined to believe that the company is indeed likely to hit its full year numbers.

Valuation - the full year 2015 forecast is 102p EPS, which won't be easy, given that H1 was 41.1p, therefore requiring a big uplift to 60.9p in H2. Management think they can do it, and they are reliable management, so on balance I'm happy to base the valuation on this forecast, but maybe to not go crazy with the PER, since there is some risk of them not reaching it.

Net debt needs to be considered when deciding what PER to use. This is reported as £7.5m at 30 Jun 2015, which looks quite modest, and is only 8.3% of the market cap, so I would trim my PER only slightly to take debt into account.

Balance sheet - is just about OK, I would say. NTAV is only £524k, since the balance sheet is dominated by intangibles, as you would expect from a group that has grown through acquisitions.

My opinion - I like this share, and whilst the price has got ahead of itself in the past, it looks priced about right to me now, on about 15 times. That may seem high, but it's a quality company with good operating margin, and also it deserves a management premium - since David Cicurel has done such a terrific job in finding & bolting on sensibly-priced acquisitions. He doesn't seem to have put a foot wrong, with multiple acquisitions (it must be about 10 by now, at a guess?).

You don't get much in divis, about 1.8% yield, but that's something anyway.

The upside from this share is that Mr Cicurel might well announce more sensibly-priced acquisitions in future. I see the last one was in Jan 2015, called Armfield, bought for £9.6m. The good thing about JDG is that the acquisitions are spread out, so that cashflows can pay down debt to reasonable levels before further acquisitions are made. I like that approach, as it avoids taking on the excessive gearing that some acquisitive groups do, and often come a cropper in the next recession, or if interest rates shoot up.

So overall then, it's a nice share, and looks priced about right, in my view. Probably more upside than downside in the long term - although note from the chart that it's best not to get too carried away with the valuation here, as it came crashing back down to earth in 2014 after a period of shareholder euphoria got a bit out of hand!

The other thing to consider is this - if a group can buy its constituent parts for relatively modest prices, as in this case, then should the combined group of such companies (with little synergies) be put on a high rating? I would argue not. Otherwise there's a danger that you might be putting 2 + 2 together, and valuing it at 8.

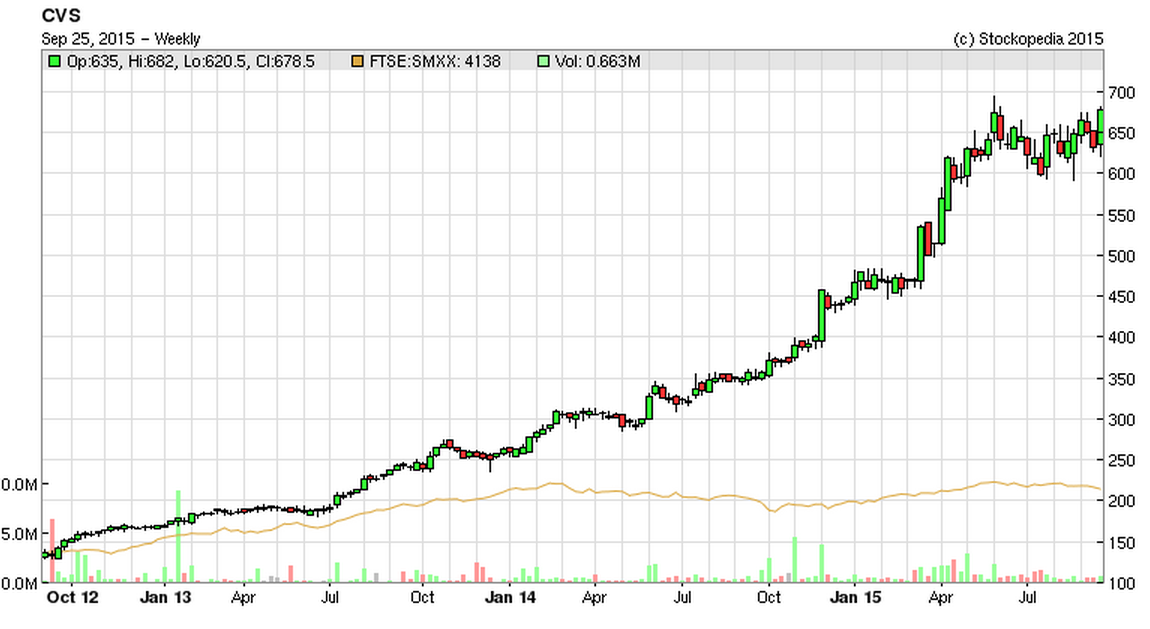

CVS (LON:CVSG)

Share price: 680p (up 7.7% today)

No. shares: 59.2m

Market cap: £402.6m

Results year ended 30 Jun 2015 - following nicely on from JDG, this is another acquisitive group, which is buying up veterinary practices. As you would expect, these are very small businesses, so lots of them are being accumulated - 30 were bought last year, 8 more since the year end, so the total is now 298 branches. That must be a nightmare to handle at Head Office from an administrative point of view, since each branch will be used to doing things their own way, and might resist standardisation.

There's no denying that these headline figures look terrific;

The 30% increase in adjusted EPS is probably the figure I focus most on. The growth has not all been down to acquisitions either, as LFL sales were up 6.8%, a really excellent performance.

Skimming through the narrative, the group is doing some interesting things like introducing its own-branded products, such as flea and worming treatments. That should enable them to improve margins, and is the sort of thing that is a genuine synergy - i.e. the profitability of acquired branches can be improved in this way.

Balance sheet - the big problem with growing through bolt-on acquisitions, is that it wrecks your balance sheet - intangible assets balloons, as does debt.

In this case, NTAV is negative, at -£40.1m, which is a concern.

Net debt is £46.2m, about 2x EBITDA, which is not excessive (and within the bank covenant limiting it to 3x ), but probably towards the top end of what is reasonable. Note 7 in today's accounts gives some interesting detail on the bank debt. Everything looks fine for now, but my worry is that companies which rely on bank in order to function on a day-to-day basis (as opposed to funding physical asset purchases) are really a hostage to fortune. What if something goes wrong? What if there's another credit crunch, with banks aggressively shrinking their lending books? I much prefer net cash situations, then you don't have to worry at all about these potential issues.

Valuation - it's always looked expensive, but has grown into the valuation. That said, at 680p the shares are rated at 27.5 times adjusted EPS just reported. That does seem rather extreme, especially considering that there is debt to take into account too, so it's really just over 30 times once you allow for that.

The only question is to look at whether further growth, and improving margins, could mean that such a premium is justified? I imagine vets are a good space to operate in, as the pricing is high, and this group seems to be doing clever things to improve margins (more efficient group buying, etc).

Outlook - sounds positive, although note that LFL sales increases have slowed;

The outlook for CVS remains very promising. Whilst like-for-like sales growth in the Practice Division returned to more normal levels in the second half of the year and has continued at this level into 2016 this still represents a good performance. Other initiatives such at the benefit of our own brand products and the opening of Lumbry Park, our Major Multi-Disciplinary Referral Centre, will begin to deliver significant benefits in 2016. In addition the acquisition pipeline remains very buoyant.

The Board is optimistic about the Group's future. It estimates that CVS only has a 12% share of the UK small animal veterinary market and a negligible share of the equine and large animal veterinary market. This demonstrates the major opportunity for further growth and consolidation and we expect to make further practice acquisitions.

Living Wage - it's interesting to compare what different companies say about this. The salary differentials point is worth bearing in mind;

The summer budget increased the NLW from £6.50 to £7.20 per hour for workers aged over 25, effective from April 2016. The change in legislation also increased the national minimum for apprentices, workers aged 16-21 and workers 21-25. The after tax impact on the Group's profit is £0.3m; however, the potential impact of maintaining salary differentials has not been quantified.

My opinion - I like the business, and these are excellent figures. However, the price is just much too high for me - I think the clever money has already been made on this share, and the trouble is that there's no leeway in the valuation now to allow for anything going wrong.

I don't like the balance sheet either, and would much prefer it if the company took advantage of the very high share price to do a Placing of say £50m, to shore up its balance sheet so that it's not relying on bank debt to operate the company.

Kudos to the investors who saw the opportunity here, and focussed on the growth rather than the short term valuation, as they have been richly rewarded over the last three years. Although how much further it can go from here, is another question. I can't see the point in getting involved at this stage, now the upside is already priced-in:

Right, got to dash! See you tomorrow.

Regards, Paul.

(of the companies mentioned today, Paul has no long or short positions.

A fund management company with which Paul is associated may hold positions in companies mentioned here.

NB. Paul is NOT a tipster, and never gives recommendations or advice. These reports are his personal opinions only)

See what our investor community has to say

Enjoying the free article? Unlock access to all subscriber comments and dive deeper into discussions from our experienced community of private investors. Don't miss out on valuable insights. Start your free trial today!

Start your free trialWe require a payment card to verify your account, but you can cancel anytime with a single click and won’t be charged.