Good morning! A quick report today, as I have to jump on a train shortly for Peterborough, to spend 2 days at Mello Workshops. I did my presentation slides last night, and woke up this morning with some more good ideas, so a few last minute amendments to do still.

Crawshaw (LON:CRAW)

Share price: 49p (down 9% today)

No. shares: 79.6m

Market Cap: £39.0m

Final results - for the year ended 31 Jan 2015. This is a difficult company to value, as its stated aim is to do a substantial roll out of its butchers & hot food shops. Therefore it should be a very much larger business in years to come (200 shops are planned, about 10 times the current size of the business!), and the share price is anticipating that. Therefore it looks expensive on the current size & performance.

Balance sheet - is very strong. The key figure is £9.1m cash (with no debt, all was repaid in the year), which came about due to a Placing. Therefore almost a quarter of the market cap can be adjusted out, as being the cash pile. I seem to recall new shops costs about £400k to fit out, so the cash pile is enough to roughly double the size of the business, about 20 new shops.

Profitability - turnover rose from £21.0m last time, to £24.6m this time, and growth should accelerate as new shops are opened by the new CEO (a former top guy from Lidl UK - so someone who is familiar with the sector, and has already been part of a major store roll-out).

Operating profit rose 15.1% to £1,137k. So not an exciting level of profitability yet, especially when you consider the £30m enterprise value. EBITDA was £1,573k, which ignores the £436k charge mainly for depreciation.. Therefore the EV/EBITDA valuation multiple looks very aggressive at 19 times. A figure of about a third of that would seem more reasonable to me, so the valuation is really one third the current business, and two thirds future growth expectations.

Current trading - LFL sales in the first 10 weeks are actually down, by 4%. That's got to be a bit of a concern, although they are up against very strong comparatives (up 19%). Even so, I would not expect sales to be going backwards.

Outlook - "short term profits will be held in check for a while as we add infrastructure costs ahead of the curve... as we build scale as quickly as practically possible".

My opinion - I can see both points of view on this one. Bulls are anticipating a successful roll-out, and taking a long term view. They may well be right. However, the problem is that the valuation is too high in the short term, given where the company actually is right now.

So investors just have to weigh up those issues, and decide accordingly.

There's a lot of competition too, from supermarkets. The company points out that all its shops are profitable, which is a very good position to be in - most retailers have some loss-making shops, so if all your shops are profitable, that is a very good sign that the business model is a good one, since it appeals to customers in all locations where it's been tried.

As the two year chart shows, the shares have had an amazing run, and now seem to be trending sideways/down, as bursts of excitement come and go. Thinking about valuation, I'd say an EV of about £24m would be the maximum price I'd be prepared to pay at the moment, which equates to about 30p per share. Anything above that is factoring in too much future upside for my taste.

Trakm8 Holdings (LON:TRAK)

Share price: 112.5p (up 15.5% today)

No. shares: 28.9m

Market Cap: £32.5m

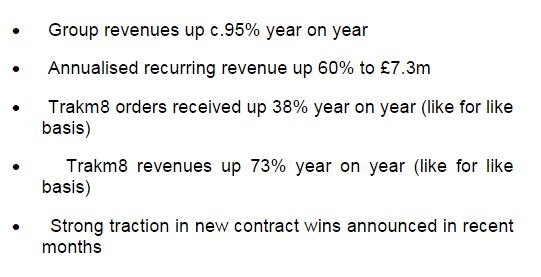

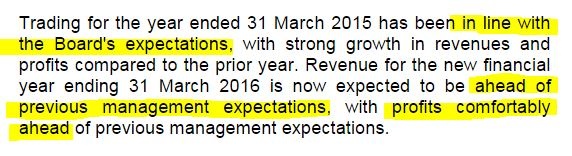

Trading update - it's difficult to make sense of this update, as the headline figures look so good, although some of the growth is due to an acquisition;

The key part says;

Valuation - broker consensus is for 5.72p for y/e 31 Mar 2015, giving a rather high PER of 19.7. However, it's the comments about 2015/16 which sound more interesting - broker consensus is 7.98p, so "comfortably ahead" suggests to me perhaps 9-10p EPS might be on the cards for this year? If that's correct, then the PER drops to between 11 and 12.5, which looks good value for a company growing impressively.

My opinion - the Directorspeak sounds so positive, that it's tempting to throw caution to the wind here, and buy some stock, despite it having risen greatly already. I've been thwarted in the past, trying to buy this stock (I recall there being none available when I tried to buy some at about 19p a couple of years ago!).

I need to do some more research on the products, and what is driving the growth, but it certainly looks an interesting company, and a positive update today. It's very difficult to buy after this sort of price rise has already happened (see two year chart below), but if the fundamentals justify it, which they do seem to here, then previous price rises don't really matter.

Have any readers looked at this company? What do you think of it?

Sweett (LON:CSG)

Update - the group traded in line with market expectations for the year ended 31 Mar 2015. The new CEO has decided to put its Asian business up for sale, to reduce debt. This is about a third of turnover by the looks of it.

The two big problems with this company are that debt is too high, and the ongoing investigations by the authorities in the UK and USA, into fraud allegations made by the Wall Street Journal. The accounts for y/e 31 Mar 2015 will include a £1.6m exceptional charge for this issue.

My opinion - these shares cannot be considered investable, in my opinion, until the WSJ allegations issue has been properly closed down. So it remains on my bargepole list - it's much too high risk for the time being - why take that risk, when we don't have to?

All done for today, see you tomorrow.

Regards, Paul.

(of the companies mentioned today, Paul has no long or short positions. A fund management company with which Paul is associated may hold positions in companies mentioned)

See what our investor community has to say

Enjoying the free article? Unlock access to all subscriber comments and dive deeper into discussions from our experienced community of private investors. Don't miss out on valuable insights. Start your free trial today!

Start your free trialWe require a payment card to verify your account, but you can cancel anytime with a single click and won’t be charged.