Good morning!

Dialight (LON:DIA)

Share price: 732p (up 10.8% today)

No. shares: 32.5m

Market Cap: £237.9m

(disclosure: I have a long position in this share at the time of writing)

Final results for the year ended 31 Dec 2014.

It strikes me as odd that the market has reacted so positively this morning (the share is up nearly 11% today) to results which are only slightly above expectations. Indeed, the company flagged on 16 Jan 2015 that it was trading in line, and I reported on the company that day, saying I thought it looked good value at 789p. So it was utterly perplexing why these shares took a dive down to around 600p in recent weeks, only to come back up again!

I know shares fluctuate in price all the time, but that is usually driven by changes in the company's performance or outlook. There haven't been any such changes here to warrant such price gyrations, so I remain perplexed!

Actually, thinking about it, I wonder if the recent change in CEO might have given some shareholders the willies? Judging from today's results, there doesn't appear to be any underlying problem.

Earnings - up 20% to 36.8p (broker consensus is for 35.9p, so a small beat there). Note that the company has been a bit cheeky in classifying a £2.8m inventories writedown as non-recurring. This means prior year profits were effectively overstated by £2.8m. I generally find the accounting policies at this company a little too aggressive, e.g. they capitalised £3.5m in development spend in the year, which was well above the £2.3m amortisation charge for the year, thus providing a boost to profits.

Valuation - at 732p the PER works out at a rather warm 19.9. However, with EPS forecast to rise again to 45p this year, then the PER would drop to a more reasonable 16.3. If earnings continue rising in subsequent years, then the shares might end up looking cheap in a couple of years' time. Although if there are any nasty surprises between now & then, the price could take a tumble. This is the problem with almost everything at the moment - valuations look pretty full, and don't factor in any downside risk.

Balance Sheet - Dialight sails through all my balance sheet tests with plenty of room to spare, so it looks a safe share in terms of financial strength. Borrowings are low at £7.3m, and are offset by cash of £7.9m, so it ended 2014 with net cash of £0.6m.

Dividends - total divis for the year were hiked a modest 4%, to a total of 15.0p for the year. That's a yield of 2.0%. With such a strong balance sheet, the company has scope to pay more, I would say.

Outlook - sounds positive, but with no specific detail;

My opinion - I quite like this stock, as it is operating in a growth area of LED lighting, for industrial use. So they supply the very bright lighting that you now see at overnight roadworks, for example - those huge, very bright overhead lights which make it almost as bright as daylight on a cloudy day.

The shares have been much more highly rated in the past, and the strong growth being demonstrated now surely justifies the historic PER of just under 20. It's financially sound, and pays a growing divi. Not exactly a bargain, but seems reasonable if the growth is set to continue. As you can see from the two year chart above, the shares have been in a downward trend, scrubbing off a previous over-valuation, whilst the market as a whole has risen over the same period.

Naibu Global International Co (LON:NBU)

I'll keep this brief, as the shares are suspended, and unlikely to return, in my opinion.

If you recall, this is the Chinese company where the UK Non Execs recently said that management were not responding to their request for information about the company. Well the reason might be because it is alleged by investigative journalist Tom Winnifrith, on ShareProphets, that the CEO is in prison!

Apparently the Chinese authorities are cracking down on businessmen who damage China's reputation by behaving badly abroad. Is that a stable door I hear swinging off its hinges?! The horses are long gone!!

It will be worth waiting for the next comedy announcement from the Non Execs to explain this one away. People cannot say they were not warned.

Coms (LON:COMS)

Resignation of CEO - another saga here, that I reported on last week, so an update today. The CEO has withdrawn his EGM requisition, and himself resigned. It sounds a tricky situation. My reading of the accounts suggests that a fundraising is extremely urgently needed, so expect news of a discounted Placing in about 3 or 4 weeks't time maybe?

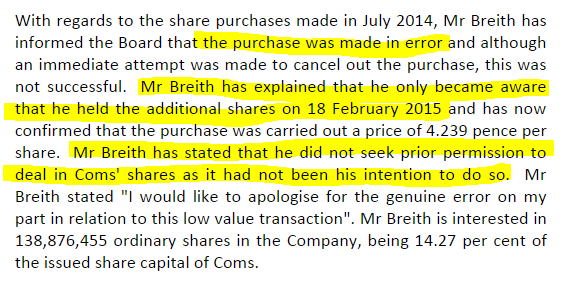

The matter of the former CEO making a shares purchase when he shouldn't have done is updated, with this bizarre "explanation", which doesn't make any sense at all to me. Is he perhaps hinting at having been in some kind of transcendental trance when he instructed his broker to buy the additional shares, and thus his conscious mind was not aware that he had bought these shares?!

Nothing that happens on AIM surprises me any more. It's getting more ridiculous by the day.

Seeing Machines (LON:SEE)

Share price: 5.25p

No. shares: 941.0m

Market Cap: £49.4m

(disclosure: I have a long position in this share at the time of writing)

Interim results for the six months to 31 Dec 2014.

This is a tricky situation to assess, because the company is mainly jam tomorrow. However, it is also delivering a little jam today! Its eye and face tracking software (which prevents accidents by alerting drivers who are falling asleep, or distracted) is currently being sold to the mining sector - a limited market, for the very large yellow trucks that are used to move large quantities of earth & rock.

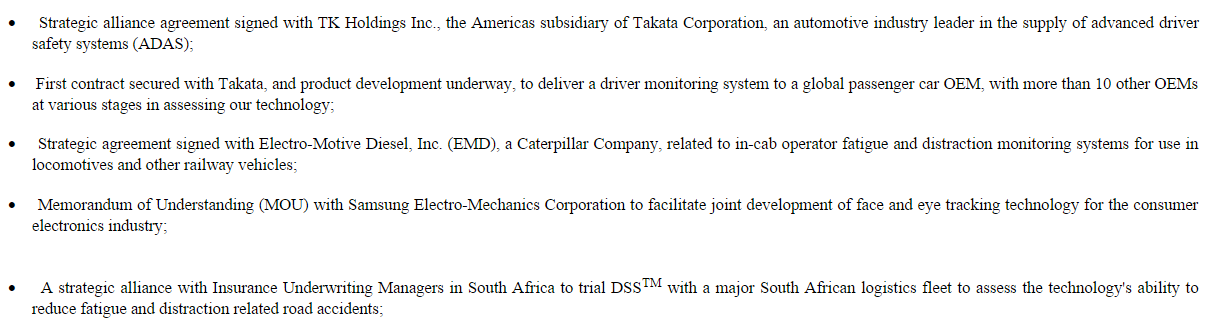

However, the jam tomorrow potential is across multiple markets, mainly trucks & coaches, trains, aircraft, and the biggest one of course in due course could be cars. On top of that, the company also has a deal with Samsung to develop the product for consumer electronics.

So how on earth do you value it? In my view the only rational way is to guess what sales might grow to in these sectors, and then try to estimate a value based on that. This makes the current figures almost irrelevant, although I'm wary of saying that, as last time I thought that was with Tungsten (LON:TUNG) and the shares then dropped heavily, as investors took fright at heavy short term losses, and opaque future potential.

Results - turnover rose 41% to £4.8m (I am converting these figures using Aus$1 = £0.51) for the six months, although it's worth noting that a good chunk of the top line has come from forex gains, and what looks like R&D tax rebates. Excluding these items, turnover was quite small at about £2.8m for the six months. Still, it's a start - and in my view, the product clearly works, and if they can generate that level of turnover from a relatively small sector (mining trucks) which is in the middle of a big capex squeeze, then what might the potential be from the vastly bigger road transport markets?

Loss - this works out at £2.2m loss for H1, and the narrative refers to increasing development spending. I would prefer two columns for the results - one showing the trading in the mining sector, and the other showing development spending for other sectors, as merging them doesn't really tell me very much - the loss can be anything management want it to be, as it depends mainly on what pace they crank up development spending.

Cash - as with all loss-making companies, cash is king. The company had £10.8m in cash at the end of the period, and looks to have burned through about £8.0m in the last 12 months (taking figures from the cashflow statement). Therefore it looks to me as if the company will need to look at another Placing & Open Offer late in 2015 or early 2016. That's not necessarily a problem, if it coincides with good progress having been made by the company, and the market being receptive to jam tomorrow stocks.

Outlook - there are interesting developments imminent - especially their DSSFleet product, which is on track for launch imminently, in Apr 2015 - for road transport. This product could end up being pushed by insurance companies, as it should prevent some road accidents, and hence not only save lives, but also reduce claims against insurance policies. We know the product works, as it's being sold successfully in the mining sector.

The third party development agreements look impressive too, giving further third party confirmation of the narrative from the company itself;

My opinion - this looks one of the most convincing jam tomorrow shares I've seen in recent years, because it is already selling a version of the product in a niche sector. How to value it? It's a finger in the air jobbie at this stage I'm afraid. If it takes off, then we could have a multibagger on our hands. If it doesn't, then the company could scrape along, diluting shareholders with more fundraisings at lower prices along the way, and perhaps never make the big commercial breakthrough?

Newsflow in coming months re the DSSFleet product will I think be crucial, and give an important pointer as to what the future might hold.

As the chart above demonstrates, it's all about timing with this type of share. If you buy when everyone is terrifically excited about the potential, then you're more likely to lose money. If you buy when everyone is nervous, and doubting it, then that can either mean the story has become stale, and is going down the pan, OR it can mean that you're getting in at a favourable entry point. Trouble is, we never know which it is until after the event!

I like this one though, hence am happy to hold, whilst appreciating that it has to be considered quite high risk. What do readers think?

Thorntons (LON:THT)

Share price: 70p

No. shares: 68.9m

Market Cap: £48.2m

Interim results - covering the 28 weeks to 10 Jan 2015. It's surprising to note that Thorntons appear to split their results into a 28 week H1, and a 24 week H2. I'm surprised that is allowed actually, and it's not something I can recall ever seeing before.

I have seen companies add an extra week onto a year occasionally to reflect the fact that 52 weeks is 364 days, so roughly every six years you will have ended up slipping back a week, if you report using 52 week periods, instead of 12 months. However, to report different length H1 and H2 every year (I checked back, and they did the same in 2014 and 2013 - 28 week H1) is bizarre - presumably their reason is to make stock-taking easier after new year?

Let's hope this isn't the start of a new trend for companies reporting interim results prepared on any date they feel like?

Trading - the company has already warned on profits, so reporting H1 profit a bit down on last year should not come as a surprise to anyone who has been paying attention!

There is pronounced seasonality here, with H1 approximating to a full year's profit, with H2 around breakeven typically, judging from recent results.

The problem here is that the company's strategy has hinged on them reducing their retail operations, and concentrating on building up being a FMCG supplier to supermarkets & other retailers. That seems to have gone a bit wrong, with apparently two large accounts causing them problems, and resulting in a decrease in the FMCG division's turnover by 11.2%, whilst the retail division seems to be performing quite well, with LFL sales up 2.2% (including an "outstanding" performance over Xmas with sales up 7.8%).

Another 20 stores are due to be closed, which should help profits, as presumably they are all loss-making, otherwise they wouldn't be facing closure. Or rent reviews would perhaps make them loss-making imminently.

EPS - basic EPS fell from 7.8p last year to 7.2p for the most recent year.

Valuation - at 70p per share, the valuation is a PER of only 9.7, which would begin to interest me, if the balance sheet was sound. Trouble is, it's not...

Balance Sheet - two specific problems here - there's too much debt, and a nasty pension deficit.

Net debt - this looks too high to me, at £30.8, which is up a whopping £11.0 versus the same period last year. Both inventories and debtors are up considerable in the last 12 months, which they shouldn't be, given that turnover is actually down. That suggests to me that maybe those pesky supermarkets are putting the squeeze on everything - not just profit margin, but probably also taking longer to pay Thorntons invoices, and requiring them hold more stock for them to call off when they want to.

Pension deficit - a lot of companies are reporting enlarged pension deficits at the moment, as low bond rates mean that liabilities have grown when discounted to present value using the lower interest rate.

Thorntons shows a £36.7m pension deficit on its balance sheet, but the actuarial figure is probably quite a bit worse, they usually are. The company says that cash overpayments are rising;

£3.25m p.a. being paid into the pension fund is a big old lump of cash, and that's money that is not available for paying as divis.

Dividends - no divis have been paid since 2011, and the company today says it wants to resume divis, but not just yet.

My opinion - it's starting to look potentially interesting at 70p, but it's always the balance sheet that puts me off here. Also, the FMCG strategy seems to have hit the buffers, and it's difficult to see them being able to make any progress against the supermarkets. More likely to go backwards, I would guess.

Overall then, with little prospect of sustainable divis happening any time soon (or ever, actually), I'm finding it tough to get excited about Thorntons. If they fixed their balance sheet, with a (say) £30m+ equity fundraising, then I might consider it. Overall though, as a low margin business with limited growth potential, it's probably not cheap, even after the share price falling a fair bit.

Although there could be scope for the shares to come back up again, if trading improves.

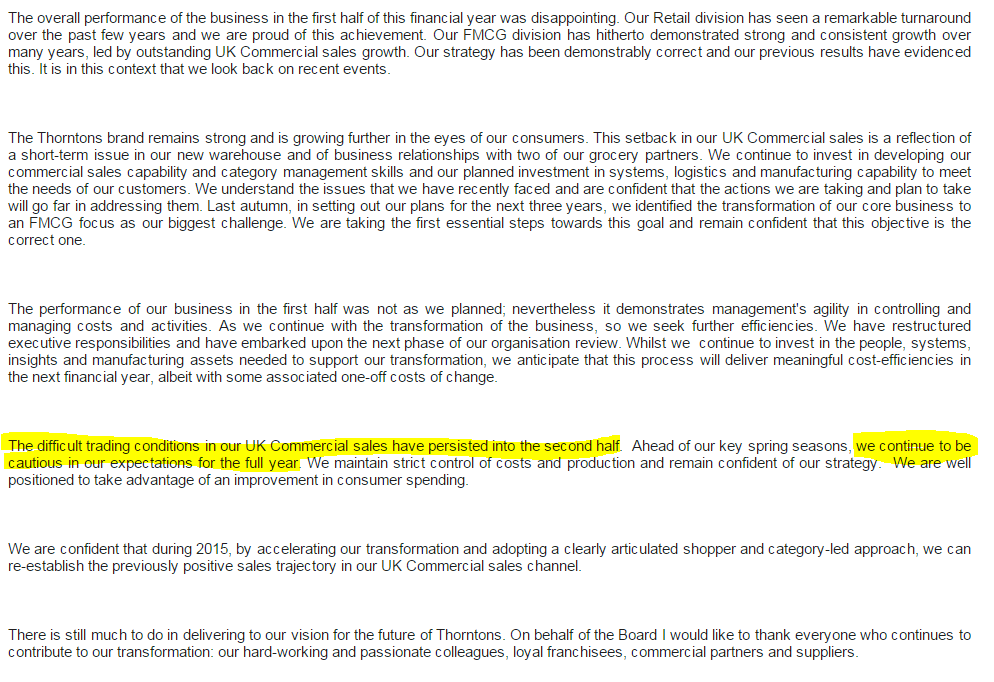

The Directorspeak today doesn't sound very upbeat though, here is the long-winded outlook statement today;

All done for today, see you in the morning, as usual.

Regards, Paul.

(Personal positions held by Paul are as disclosed in the article above. A fund management company with which Paul is associated may also hold positions in companies mentioned)

See what our investor community has to say

Enjoying the free article? Unlock access to all subscriber comments and dive deeper into discussions from our experienced community of private investors. Don't miss out on valuable insights. Start your free trial today!

Start your free trialWe require a payment card to verify your account, but you can cancel anytime with a single click and won’t be charged.