Good morning! Today's report is going to have to be a bit briefer than usual, as the first version has just disappeared due to a computer malfunction, and I have to go out for a lunch meeting shortly. So will rattle through as best I can.

Pubcos

There was big news last night, when a rebellion of some MPs saw an amendment passed, against the wishes of the Govt, to allow tied pubs to buy drinks on the open market. This has put a massive spanner in the works for pubcos such as Punch Taverns (LON:PUB), Enterprise Inns (LON:ETI), and others. Will the takeover of Spirit Pub (LON:SPRT) still go ahead I wonder?

If this measure is not reversed, then it could kill off the tied pub, and would be disastrous for pubcos profits. So this sector could still be a good area to think about putting on some short positions perhaps?

Vianet (LON:VNET) shares have also dropped in sympathy, as their main profit earner is the beer flow monitoring equipment used by pubcos to monitor that only expensive beer bought from them is being served, and not cheaper beer from the open market.

Avon Rubber (LON:AVON)

Results for the year ended 30 Sep 2014 are out today, and look good on a brief skim.

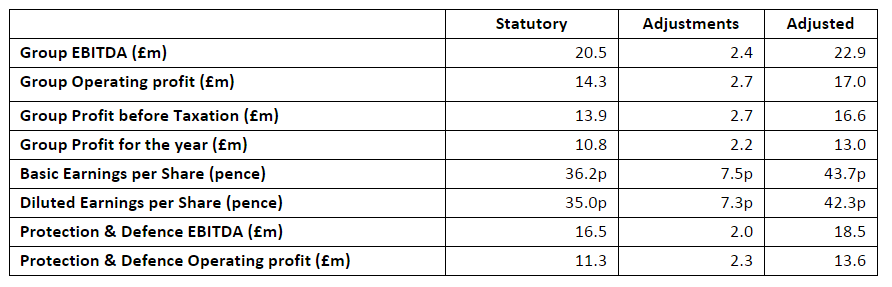

Company results seem to be getting more & more complicated, with companies seemingly inventing their own definition of profit to give the most flattering result possible. Check out this complicated table;

Broker forecast seems to be 40.3p, so using the 43.7p adjusted EPS figure above, the company seems to have beaten expectations.

The company has also moved into a net cash position, of £2.9m, which is good.

There is a pension deficit, but the overpayments are less than 10% of profit, hence it's not material in my view.

Outlook sounds positive;

Our strategy has significantly improved the shape of the Group, reduced the risk profile and improved margins. This is providing continued growth and the outlook for the future remains positive.

Dividends - at under a 1% yield, the divis are very small, and over 7 times covered, which strikes me as being unnecessarily cautious. Shareholders should be reminding management who owns the company, and demanding a greater slice of the cake, in my opinion!

My opinion - I've missed the boat on this one, and don't know enough about the business to determine whether higher profit is sustainable or not. If you think the profit growth is set to continue, then the shares might be worth a look?

I imagine broker forecasts will be increased, so if maybe 50p EPS is achieved this year, then the shares being priced around 700p currently would put it on a PER of 14 - which doesn't look expensive, if that profit growth is sustainable. So worth a deeper look perhaps?

Optos (LON:OPTS)

Results today from this retinal imaging company look impressive.

The outlook comments also seem upbeat;

We expect to see continued new customer growth similar to FY14, delivering low single digit revenue growth in FY15. This would have been higher if not adjusted for the early corporate account renewal in FY14. Gross margin for the full year, on the basis of the anticipated mix of capital sales and rentals, is expected to improve to around 60%, exiting the year at a higher rate as we benefit from the new products. In future years, we anticipate further incremental improvements in gross and operating margins as we benefit from the new product platforms, as well as continued customer growth and continued renewal opportunities. As with previous years, revenue is to be heavily weighted to the second-half of the year with a consequential impact on profit and cash.

With strong sales of Daytona, our new products progressing well, the increasing body of clinical evidence and a broadened geographical reach, the Board is confident that Optos is well placed to drive customer growth, continued improvements in profitability and sustainable cash generation in FY15.

Adjusted profit before tax has doubled to $18.5m (note this company reports in dollars), which is impressive.

Stockopedia shows the forward PER to be about 15, which seems reasonable.

So this one gets another cautious thumbs up from me - looks worthy of doing some more detailed research at least.

AGA Rangemaster (LON:AGA)

Trading update - saying that the company is doing well in the UK, but less well in Europe.

The company doesn't seem to mention anything about profits, so a bit pointless putting out a trading statement without saying how profits are going! I am assuming therefore that there will be no change to market expectations.

I consider this share uninvestable, as the pension deficit & associated overpayments are extremely large, and are likely to consume any cash the business generates for the foreseeable future. Arguably that makes the equity worth little to nothing, since only token divis seem likely.

MyCelx Technologies (LON:MYX)

A fairly grim announcement today, flagging a potential revenue miss, and worse still a need for more cash;

The Company believes project award notifications in regard to three projects are forthcoming in the near term. The total value of these projects exceeds $20 million. However, the award process is specific to each customer and project resulting in unpredictable timing. Should no revenue from these three projects be recognised in the 2014 financial year, the Company would expect the revenue to be no less than $16 million.

The Company remains confident about future prospects in spite of short-term forecasting challenges. Given these prospects, the increased project sizes and the working capital requirements that flow from these, the Company is exploring possible funding options to finance continued future growth.

I'm surprised the shares haven't dropped a lot more actually, they're currently showing a fall of 7%.

Blur (LON:BLUR)

Trading update - which is rather confusingly worded. It starts off sounding positive, then goes on to say that large projects are delayed.

The company says it has $20m cash, and indicates that breakeven is within sight;

...all indicators that EBITDA breakeven will be achieved in Q4 2015 along with positive cash flow from Q1 2016.

I remain sceptical about this company's ability to reach profitability, but who knows? At least it has enough cash to fund losses for the time being.

Shares have lurched down 16% to 61p. The story feels stale to me.

I have to leave it there for today. See you tomorrow!

Regards, Paul.

(of the companies mentioned today, Paul has no long or short positions.

A fund management company with which Paul is associated may hold positions in companies mentioned)

See what our investor community has to say

Enjoying the free article? Unlock access to all subscriber comments and dive deeper into discussions from our experienced community of private investors. Don't miss out on valuable insights. Start your free trial today!

Start your free trialWe require a payment card to verify your account, but you can cancel anytime with a single click and won’t be charged.