Good morning! Today's SCVR will be slightly later than usual. This is due to me beginning to make the transition to Las Vegas time, in advance of my flight on Monday, in order to prevent jet lag*. Yes, I've decided to chance my luck against those hapless Yanks - rumour has it they are terrible poker players. So I'll be flying out economy, and hopefully coming back first class! Am spending next week in Vegas, enjoying a bit of sun, lots of cocktails, and hopefully separating some low standard poker players from their money. Sounds harsh, but they are willing participants, and seem to enjoy losing money - not a million miles away from AIM actually, when you think about it. I wonder if bulletin boards for poker are also populated with the foolish & inexperienced hurling abuse at experienced & successful players? Anyway, the end result is the same - money flows from the hapless to the disciplined.

* = most creative excuse ever?!!!

Next week's SCVRs - as I will be 8 hours behind UK time next week, my reports will be published in the evening UK time, rather than the morning. Sorry about that. Also they will probably be a little shorter too, as Balance Sheet analysis is not really what you want to focus on when sunbathing, gambling, or watching Mariah Carey mime to a soundtrack.

Right, on with some company analysis ...

CML Microsystems (LON:CML)

Share price: 268p

No. shares: 16.2m

Market Cap: £43.4m

One of the things I like about small caps, is that there are so many shares to choose from, that you can keep hundreds of companies on your watch list, and then just wait for the price to fall to an attractive level. The only problem is that when the price does fall to an attractive level, it's usually due to bad news having been issued.

I've had my eye on CML Microsystems for a couple of years, and it looked potentially interesting, but far too expensive. The price has now come down to a level where I would consider it in more detail, so let's have a dig through it results issued today.

The company says that it;

...manufactures and markets a broad range of semiconductor products, primarily for the global communication and data storage markets.

That scares me a little, as I know nothing about that sector. Although in general terms, I'm already thinking about technology changing quickly, products becoming obsolete in a short space of time, constant need for heavy development spending, etc. However, also big potential upside, if the company hits a sweet spot with an appealing product & hence rapid growth.

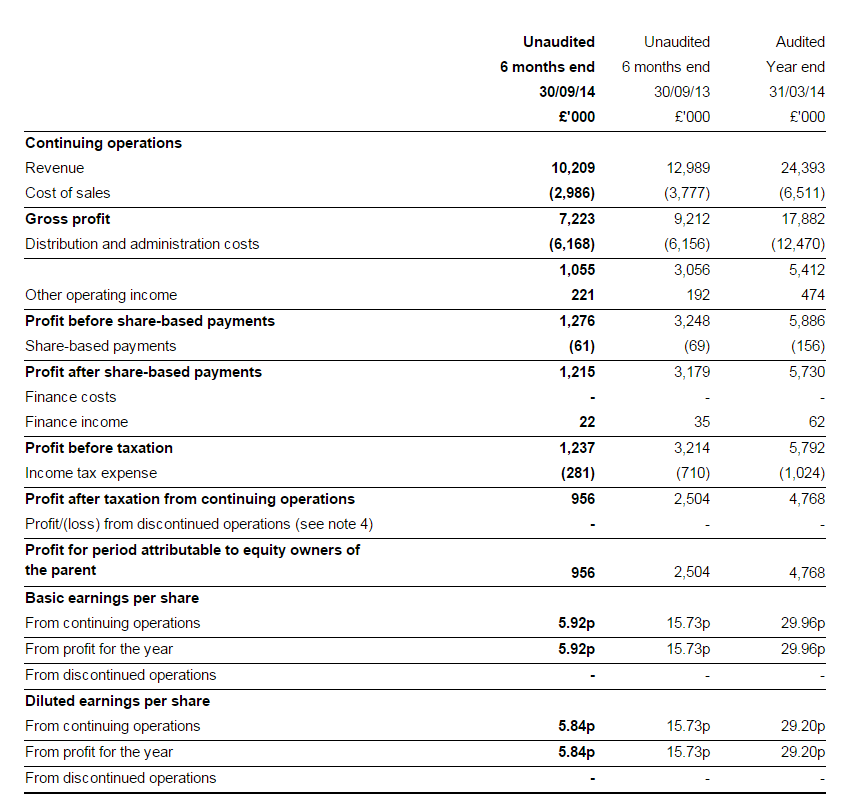

Interim results - for the six months to 30 Sep 2014 are published today.

As you can see from the P&L below, this is a perfect case study in operational gearing. Overheads of £6,168k are virtually identical to last year's H1, However, the 21.4% fall in turnover to £10.2m, on a high gross margin of 70.8%, causes a much greater % fall in profit. Profit before tax has fallen 61.5% to £1,237k as a result of this operational gearing.

It's fun when sales are growing, but operational gearing is savage when things are deteriorating, as you can see below.

Development spending - It's always worth checking the cashflow statement to see what development costs a company is capitalising and amortising, as I like to work on a cash basis, not parking costs on the Balance Sheet temporarily. Incidentally, the cash basis is how nearly every company works for internal budgeting purposes too. Cash is king, whereas a P&L is telling a story.

In this case, the company amortised £1.4m in previous development spending through its P&L for H1, but capitalised £2.7m in fresh development spending onto the Bal Sheet in H1. So reversing those transactions to get at the cash profits, you find that there aren't any! In fact it made a £0.1m loss for H1! Not good, is it?

Balance Sheet - this is wonderful. The current ratio is tremendously strong at 4.86, which includes £11.6m in net cash, which is just over a quarter of the market cap. Very comforting indeed. Makes you wonder why the company is hoarding cash, instead of returning it to shareholders?

Unusually, for a technology company, there is pension deficit shown on the Bal Sheet of £2.7m, which reduced sharply from £6.1m a year ago. So that needs looking into, in case it's an iceberg deficit - i.e. seemingly small, but with a much larger problem lurking under the surface.

Note there is also some property in fixed assets, which I like.

Outlook - this sounds quite encouraging;

Whilst it is disappointing to report interim results that interrupt the Group's sustained growth record over recent years, operating performance through the opening six-month period has progressively improved and the results delivered meet both management and market expectations.

In addition to a promising order book at 30 September 2014, new order bookings since that date serve to reinforce expectations that second half revenue should exceed the first.

The Group continues to make good progress with its numerous engineering, selling and market-related activities that are directed at widening the product range, the customer base and the addressable market areas. Whilst these activities are not expected to contribute meaningfully to the current year, I am confident that the product and management strategies being followed should allow the Group to return to growth beyond this financial year.

Quite a few bits for me to bold above, and I think there's enough red meat in there to believe that maybe the worst is over for these shares? (famous last words!)

My opinion - it seems to me that shares in CML are a straightforward bet on the company getting back to previous years' level of sales & profitability, or not. I'm not able to make a judgement on that, as I don't understand the company's products or markets.

However, I am flagging up the potential opportunity here to readers, as being something you might like to look into. If you understand the sector, then I would be very interested to hear your prognosis. My job here is just to flag up potentially interesting opportunities based on the numbers, but it's then up to readers to do your own research to decide whether it's an investing opportunity, or a risk.

(please refresh this page from time to time - am running late today, so will finish this article about 4pm. First cup of tea has now been imbibed, so things are already improving. Yorkshire Tea tastes spectacularly good here in North London, but tastes revolting in Brighton. Must be something to do with the water. I must bottle some & take it home with me)

Flowgroup (LON:FLOW)

Share price: 43p

No. shares: 239.5m

Market Cap: £103.0m

The market cap here looks nuts, but I am told that the company has interesting potential. It makes a new type of domestic boiler, which generates electricity as well as the usual function of heating radiators and tap water.

Production has started, as announced today.

I need to do more research on this company, but it looks potentially interesting, as a speculation.

Sepura (LON:SEPU)

Share price: 137.5p

No. shares: 138.1m

Market Cap: £189.9m

An interesting company this one - it claims to be a world leader in sophisticated radios as used by the emergency services.

Interim results - for the six months to 26 Sep 2014 are out today.

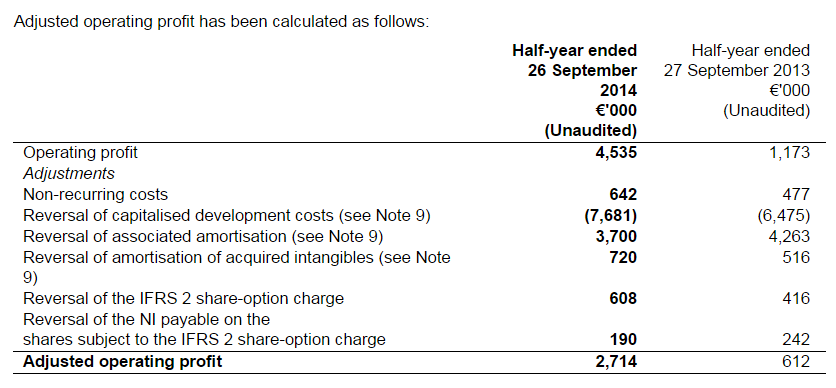

Note that the company reports in Euros. I am struggling to get my head around the numbers, because this company does something bizarre, which I've never seen before - it reports normal profit, but also adjusted profit which is lower than normal profit!! Normally companies adjust the profit figure in order to show a more flattering result, but this company does the opposite.

So within the highlights section of today's RNS, it says;

- Adjusted operating profit1 €2.7million (H1/14 €0.6 million)

- IFRS operating profit €4.5 million (H1/14: €1.2 million)

A helpful table is provided to reconcile the adjusted and non-adjusted profit figures. As you can see below, it's the treatment of development spending which is the big issue here;

So again, I'm really scratching my head as to why the company reverses its policy on capitalising development spending, and presents a more conservative adjusted profit figure? Top marks to them for doing so, I applaud the company for focusing investors on the most conservative profit measure.

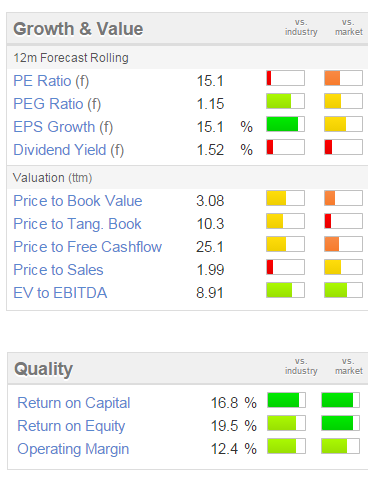

Valuation - quality scores are high, and the forward PER is not excessive, so it looks priced sensibly to me.

Outlook - this is where it starts to look interesting;

There is little doubt that the pace of analogue to digital migration of Professional Mobile Radio ("PMR") users is accelerating. Governments and businesses are investing in increasingly complex solutions that utilise a range of devices, accessories and software applications. The investments we have made to broaden our product portfolio and geographical footprint have ensured that we are positioned to address more of these opportunities, and also deliver more of the individual components required.

Our core markets continue to perform well and we have made encouraging progress on our recent initiatives to address the highest growth segments of the PMR market: DMR, North America and Applications. Our DMR portfolio, launched last year, is beginning to gain traction and has been expanded by the acquisition of Fylde. Whilst the market is at an early stage of development our TETRA terminals are now operational on all but one of the TETRA networks deployed in North America, the world's largest PMR market. We also have a growing pipeline of Applications opportunities as end-users look to achieve efficiencies through the use of data on networks they have already deployed.

While each of these strategic initiatives currently makes a modest contribution to the Group's results, we are confident they will contribute to the expected increase in revenues and earnings in FY15 and FY16 in line with our recent guidance. We look to the future with growing confidence, reflected in a 17% increase in the interim dividend from 0.59p to 0.69p.

That all sounds good to me.

My opinion - this company looks worthy of further research, in my opinion. The outlook sounds positive, and the current valuation seems reasonable, hence I am flagging up the idea for readers to consider researching yourselves.

See what our investor community has to say

Enjoying the free article? Unlock access to all subscriber comments and dive deeper into discussions from our experienced community of private investors. Don't miss out on valuable insights. Start your free trial today!

Start your free trialWe require a payment card to verify your account, but you can cancel anytime with a single click and won’t be charged.