Good morning.

These seems to be a lot of turmoil & uncertainty at the moment, what with Brexit, and the associated sharp movements in forex. Then more recently another appalling terrorist attack on France. On top of that, we also saw what seemed to be an attempted coup by a faction of the military in Turkey on Friday night, with considerable bloodshed.

It seems to be the case that we're just having to get used to a more dangerous world - no level of security could be high enough to prevent every would-be attacker. It seems to me that attackers are fitting a pattern - loners, disillusioned with life, easily led, attracted to extremist ideologies, that are being radicalised on the internet. Our counter-measures, on top of improved security, surely need to be more covert surveillance, primarily of the internet activity of "at risk" people. Plus of course, finding, and imprisoning the people doing the radicalising.

Certainly the market seems to be becoming increasingly immune to geopolitical events. Although I can't help feeling that, after the strong recent rebound, this might be a good point to take some money off the table perhaps? Or maybe to hedge longs with an index put option, or index short (but only if you really know what you're doing, in terms of managing the risk).

I'm also becoming increasingly worried about what looks to be a looming Italian banking crisis, with some alarming statistics coming from good sources on Twitter, about the very high level of non-performing loans.

ARM Holdings (LON:ARM)

Recommended acquisition of ARM by Softbank - Counter-acting the gloom today, is remarkable news of what is apparently the largest ever investment in the UK by an Asian firm. Japan's Softbank is offering 1700p per ARM share, in an agreed cash takeover bid.

That's a 43% premium, and values ARM at £24.3bn. Remarkable stuff, and congratulations to holders of the stock.

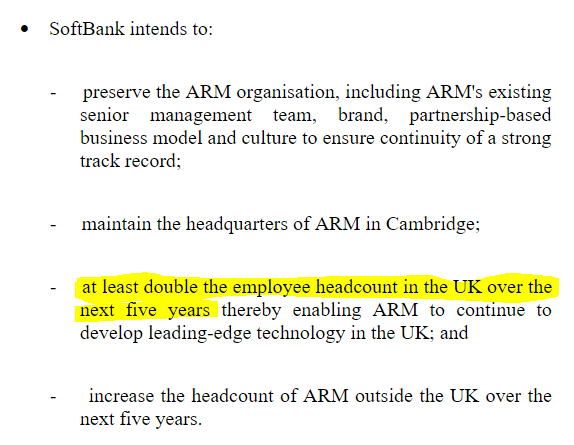

Also note the stated intentions of the acquirer;

It should of course be borne in mind that acquirers do not always actually do what they previously stated an intention to do! So a bold statement of supporting & increasing UK investment & jobs would certainly help the deal go through without the Government putting any obstacles in the way.

However, if the above quotes are taken at face value, then it certainly seems like a very welcome boost to post-Brexit UK. Remember we were recently told by many supposed experts that inward investment into the UK would dry up if we voted Brexit.

A cash takeover of this size is likely to have a knock-on positive impact - investors and analysts are likely to be looking for the next UK target company for a foreign takeover bid. After all, sterling's recent fall makes UK companies with international earnings very attractive right now. So expect a lot more takeover bids for UK companies, from overseas.

Faisal Islam pointed out on Twitter today, that Softbank have been able to buy ARM £5bn cheaper, due to sterling's 21% fall against the Yen since the start of 2016.

Shares in other tech companies are likely to get a boost, as £24bn of fresh cash is likely to come into the market for other tech companies, once ARM shareholders have been paid out.

Begbies Traynor (LON:BEG)

Q2 Red Flag Report - I reported on insolvency practitioner Begbies Traynor last week. However, it's also worth keeping an eye on the firm's quarterly red flags report, which outlines the health of corporate UK, particularly smaller businesses. Trends spotted by Begbies can be useful background for us as investors.

Here are their key conclusions today;

Research shows British businesses are in a strong position to face Brexit challenges,but expect at least six months of turmoil ahead.

Levels of financial distress fell 4% ahead of the Brexit vote, but more than 240,000 SMEs still in a dire state.

UK Property and Construction sectors expected to bear the brunt of Brexit, with nearly 50,000 firms at risk

This ties in with other information I'm hearing, that apparently big scale new proposed construction projects are, in some cases, being put on hold. Although we've heard from housebuilders recently, that it's seemingly business as usual. Therefore I think it makes sense to steer clear of contractors and advisers to the commercial property building sector, for now.

That could have a knock-on effect too, pulling down support services companies facing the construction sector. So this area needs to be monitored carefully. Also we need to watch out for signs of a more general slowing of the economy, which seems to me very likely in H2 of this year. Whether it turns into a full-blown recession? Personally I suspect probably not, but that's based on generally quite reassuring updates from most companies so far. That could change of course, so vigilance and an open mind are critical for investors right now.

Matchtech (LON:MTEC)

Name change - I've decided to create an informal new award. It's called the "What on earth were they thinking?" award. The inaugural winner is Matchtech, who decided they need a name change, because after acquisitions, the group name doesn't fit well with the enlarged group, and has apparently caused some confusion.

Fair enough. So what is the brilliant new name for the group? It is "Gattaca". My first thought is that it sounds like the noise my Mini used to make in the 1980s, when I tried to start the engine on a cold day with a nearly-flat battery. After several gattacas, it would then progress to just a humming noise, and then complete silence after each turn of the ignition key.

Perhaps I've missed some significance of the new name? So I've googled it, and the page of top results all focus on a 1997 film called Gattaca, which was a box office flop, but achieved a low level of cult status. Its main theme is a future world where eugenics are used to improve the gene pool. Is this really a good message for a recruitment group to focus on? Perhaps the firm has become frustrated at low quality candidates, and is sending a message that it wants genetically superior candidates only?!

No explanation is given in today's RNS as to why the name Gattaca has been chosen, nor what it is supposed to mean. Shareholders are required to approve the name change - it will be interesting to see if they approve this bizarre new name or not.

Christie (LON:CTG)

Share price: 78p (down 9% today)

No. shares: 26.5m

Market cap: £20.7m

Trading statement (profit warning) - this business services group says that 2016 profits are likely to be lower than expected;

Christie Group plc (CTG.L), the leading provider of Professional Business Services and Stock & Inventory Systems & Services to the leisure, retail and care markets, announces that in the light of softer than previously anticipated trading in its Professional Business Services division, operating profit for the year ending 31 December 2016 is likely to be lower than previously expected.

OK, so what has caused this softer trading? It sounds as if Brexit uncertainty may have had some impact on transactions;

Within its Agency business, a small number of transactions were lost upon announcement of the European referendum result, after which point the business sales market is continuing its function.

I don't understand what they mean by "after which point the business sales market is continuing its function". What the hell does that mean?!! At a guess, I think they're trying to say that things are getting back to normal, maybe?

The company gives a rough idea on likely revenues;

While our first half revenue to 30th June is expected to be broadly in line with the corresponding period last year, we anticipate a growth in second half revenues year on year.

So it doesn't sound like a disaster. What about profit though?

Nevertheless, after recouping the expected first half loss referred to by the Chairman at the June AGM, this growth in second half revenues is now expected to be insufficient to achieve the level of full year profit that was previously anticipated.

I didn't report here on the company's AGM statement on 15 June. However, looking at it now, it seems the company was expecting (not unreasonably at the time) a Remain vote, triggering an improvement in H2 trading;

"As I recorded in my statement in April at the release of our 2016 results, 2016 started quietly, but gathered pace in spring. Whilst progress has continued, we expect to record a first half loss. Thereafter, we reasonably anticipate a post-EU referendum acceleration of billable activity resulting in full year profitability. (NB. this is from a previous RNS on 15 June 2016)

So it seems that the Brexit vote has undermined this company somewhat.

My opinion - unfortunately, I don't yet have any revised broker forecasts, so can't really take this any further, as there's too much uncertainty over earnings.

Given that the company was loss-making in H1, then I wouldn't put too much faith on it necessarily performing much better in H2.

Looking back, profit here has generally been lacklustre, with 2 better years in 2014 & 2015. So perhaps we're now likely to see profits go back to previous more modest levels? That's what the share price seems to be telling us (see below).

I can't really see much attraction at all in this share, even though the price has halved recently. It is serving retailers, and the leisure & care sectors. These sectors are facing considerable pressure from Living Wage, and margin erosion (especially next year when forex movements will kick in, meaning higher input prices). Therefore a group providing professional services to those sectors is also bound to come under pricing pressure.

It's not for me.

Finsbury Food (LON:FIF)

Share price: 115p (flat today)

No. shares: 130.4m

Market cap: £150.0m

Pre-close trading statement - this bakery group has an end June year end, so today's update is for the full year just finished, and it looks solid;

The Board is pleased to report that, following the positive half year trading performance, strong trading has continued in the second half and the Group is confident of delivering profits in line with market expectations which were upgraded following the strong first half year.

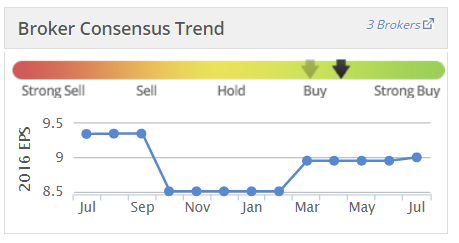

So in line, but with raised forecasts. So a decent result. Mind you, checking the terrific little Stockopedia graph for how broker consensus has moved over the last 12 months, forecasts were really only edged up back to a bit below where they had been previously;

Sales growth has benefited from acquisitions. However, note the decent organic growth of 5% too;

Total Company sales revenues grew to £319.7m, an increase of 24.8% on prior year (for the 52 week period, sales revenues were £313.5m, an increase of 22.4%), following the successful integration of the prior year acquisitions of Fletchers and Johnstone's.

This includes like for like growth of £12.8m, an increase of 5.0% versus prior year. The UK Bakery division grew by 3.0% on a like for like basis and the Overseas division, the Group's 50% owned European business, grew by 25.7%. Our sales to the foodservice channel accounted for 21% of total UK Bakery sales revenues and grew by 5.3% on a like for like basis.

Brexit comments don't really tell us much, but they don't sound too worried about it, which I find encouraging;

Whilst it is too early to fully understand the impact of the exit of Britain from the EU, the Board believes that as a strong multi-channel business and a large diversified speciality bakery group, it is well equipped to manage the potential effects of this outcome and continue to deliver growth and improved shareholder value over the coming years.

Outlook comments are vague, but with a clearly positive tone, e.g.;

"This growth is underpinned by capital investment and our continued focus on innovation, maintaining our position as one of the UK's largest speciality bakery groups. More than ever we are well placed to continue our solid performance and drive growth."

This sounds like a business on a roll (geddit?!)

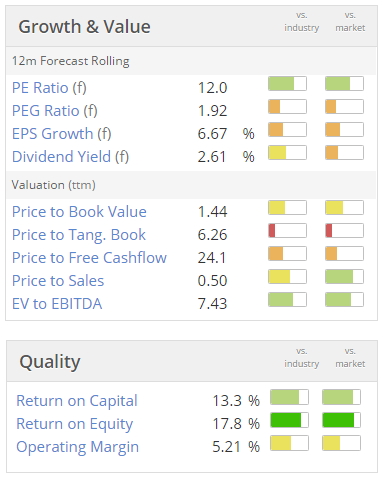

Valuation - looking at the Stockopedia graphics, the current valuation at 115p per share looks about right to me, for now;

My opinion - this seems to be a well-managed group, which is growing well, despite what must be considerable pressure from customers to erode their margins.

The trouble with groups which grow by acquisition, is that the balance sheet can be degraded, with intangibles piling up at the top, and debt piling up at the bottom. So far, FIF seems to have kept its balance sheet fairly sensible, although it's not as strong as I would ideally like.

This is the sort of share that I would certainly have on my shortlist to consider for a long-term buy & hold type of portfolio. So overall, a thumbs up from me, but I'm not really seeing any immediate compulsion to buy any.

Watkin Jones (LON:WJG)

Video of recent Mello Beckenham meeting - this is the company which presented at Mello last week, which I attended. Management came over really well, and it looks a very interesting company.

If you were not able to attend, the presentation was videoed by my friends Tamzin and Tim at PIWorld.co.uk (a terrific website, with in-depth video content on mainly good quality companies). Here is the link. It's a long video, but if you're going to risk thousands of pounds on a share, then I suggest it's time well spent to watch a video like this.

The format at Mello is to have a company presentation or two, and then we go downstairs for a nice meal & everyone can chat about the companies we've just met. Very friendly & enjoyable evenings, I must attend more in future.

I should add that we had a long Q&A session after the formal presentation, and the Directors spread themselves around the room afterwards for dinner, so everyone had a chance to ask all the questions they wanted.

I'll sign off for now. Possible update later for one more company, will Tweet if I get round to it.

Regards, Paul.

See what our investor community has to say

Enjoying the free article? Unlock access to all subscriber comments and dive deeper into discussions from our experienced community of private investors. Don't miss out on valuable insights. Start your free trial today!

Start your free trialWe require a payment card to verify your account, but you can cancel anytime with a single click and won’t be charged.