Share price: 47.4p (-1.3%)

No. shares: 106.2m

Market cap: £50.3m

Half-Year Report (six months ended 31 October 2016)

The

market is slightly underwhelmed with interim results from this

insolvency practitioner, results which the statement describes as

"solid".

The

market is slightly underwhelmed with interim results from this

insolvency practitioner, results which the statement describes as

"solid".

Over the past twelve months, Begbies has been diversifying into property services. The insolvency market was taking too long to start moving again, and so the company decided to move into a related service where it hoped there would be synergies (property auctions often taken place during an insolvency process, for example).

The Exec Chairman anticipates that 30% of revenue and profit will arise from the property services division, in the current financial year.

Outlook:

"For the year as a whole, we anticipate growth in

earnings, in line with expectations, with the benefits of our investment

in property services complementing our market-leading, profitable and

cash generative insolvency business. We will continue to look for

opportunities to develop and enhance the group, both organically and

through selective acquisitions.

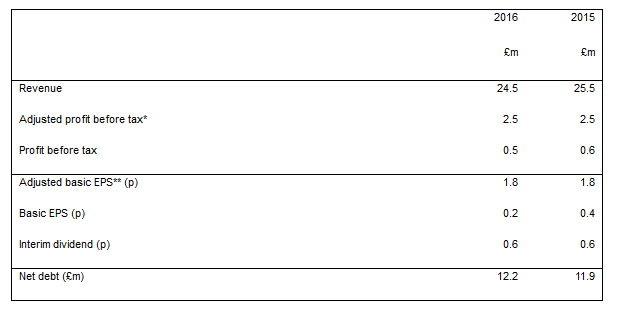

Dividend: interim dividend maintained at 0.6p.

The dividend payout has been flat since 2012, but the company would like to return to a progressive policy when possible:

The board remains committed to a long-term progressive

dividend policy, and to increase dividends when more confident of both

the market outlook and potential for sustained earnings growth..

Macro Conditions: The company is not predicting any improvement (i.e. for everyone else, a deterioration) in economic conditions. In terms of the total number of corporate insolvencies, it says "the market appears to have stabilised at this lower level", and "there are no expectations of an increase in insolvency levels".

No. of employees is reduced to 328 from 355, keeping the cost base under control.

Net Debt:

The company has a £30 million facility with HSBC. Net borrowings are £12.2 million, with total balance sheet borrowings of £17 million offset by £4.8 million of cash.

My opinion:

Overall, it looks like more of what we've come to expect from Begbies - a flattish result and a stable dividend.

While I've generally had a positive outlook on this company, which has been stable around the current share price for two and a half years, I am increasingly reluctant when it comes to investing in professional services companies - personal experience, and recent events at Fairpoint (LON:FRP), have shown me how dangerous to an investment portfolio they can be. Perhaps they are simply more suited to the partnership model.

In this case, £17 million of gross borrowings (nearly £50,000 per employee), combined with a series of acquisitions do make me a little nervous. Although that could be some recency bias talking, after what just happened at Fairpoint!

At least the founder Ric Traynor remains on board here. That is a very good form of reassurance for investors, especially considering that he owns 26% of the company.

Carpetright (LON:CPR)

Carpetright (LON:CPR)

No. shares: 67.9m

Market cap: £136m

Interim Results (26 weeks ended 29 October 2016)

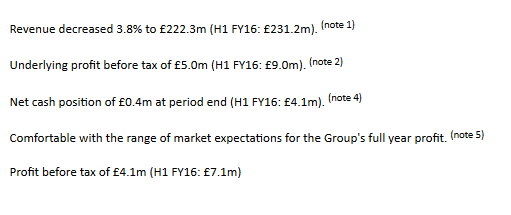

Tricky conditions for Carpetright, reporting "uneven consumer demand in an increasingly competitive market" in the UK. Like-for-like sales are down 2.9% in the UK and 1.5% in the Rest of Europe (local currency).

Outlook

The

outlook comments start off very bleak, talking about various

"substantial trading headwinds": Brexit uncertainty, consumer demand, a

competitive market and, of course, currency movements.

But then:

We have made an encouraging start to the second half with a return to like-for-like sales growth in both businesses. As we enter the important January trading period, we remain comfortable with the range of market expectations.

So things are not so gloomy, although it sounds as if investors might need to brace themselves for results in the bottom half of the range of expectations.

Those expectations are for "underlying" profit before tax of £16.1 million, with a £13.9 million - £18.5 million range. (The definition of underlying sounds reasonable to me).

My opinion:

(Please note that I own shares in a competitor, United Carpets (LON:UCG) )

I like this sector and I think that this could be a very interesting buying opportunity.

The flooring business can be an absolute cash cow, though it does have a tendency to move in fits and starts. Competition can suddenly spring up out of nowhere, and margins rise and fall with a range of macro-economic variables.

Management is key. Carpetright have been investing considerable cash sums (in this most recent period, spending £4.5 million out of the £5.9 million generated by operations) on capex, primarily on modernising its estate.

That obviously causes a lack

of free cash flow in the short-term, and it needs to provide solid

medium-term and long-term benefits. Based on what I know about

Carpetright, I'd be inclined to have a positive view on management's

ability to squeeze out those benefits. It won't be easy by any means,

but on balance I'd say that they can do it. Let me know if you disagree!

Zytronic (LON:ZYT)

No. shares: 15.4m

Market cap: £60m

Preliminary Results (year ended 30 September 2016)

I'm not running into many positive

news stories, as the market is again not entirely satisfied with these full

year results.

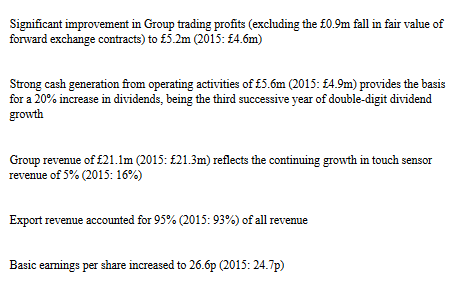

I've not looked at this Newcastle-based company before, but it's in the business of manufacturing touch sensors used in a variety of applications (ATMs, casino games, public informational displays, etc).

Turnover has been creeping higher in recent years.

FX Contracts

Nearly all (95%) of Zytronics revenue is in the export market. With all of the manufacturing facilities in the UK, that makes it a prime beneficiary of the Brexit sterling devaluation.

Note the reference above to trading profits "excluding the fall in fair value of forward exchange contracts".

I'd argue that it's not entirely satisfactory to exclude the losses on those contracts. They are designed to hedge against moves in sterling, so you have to include their gains or losses to get a result which is closer to the constant-currency result.

If the hedges had been profitable (i.e. if Sterling had strengthened), we would likewise want to include them so as to get a result which showed performance based on something closer to the original exchange rates. This is particularly important when it comes to understanding the underlying growth rate of the business!

Volumes:

Excluding the gains from foreign exchange contracts, trading profits were about 6-7% lower, so it is not surprising to find evidence that the underlying growth at Zytronic is rather lacklustre.

The total number of touch sensor units

supplied across all size ranges was 130,000 (2015: 149,000 units). The

single most significant reduction in volume was attributable to a

decrease in medium-sized 15" sensors, associated with vending

applications.

However, as the business has continued to focus on the increasing revenue benefits associated with the ultra-large format markets, with sensors greater than 30", the effects of the reduction in sensor volumes in the smaller size ranges was significantly countered.

So volumes are down overall but the mix is becoming weighted toward the high-end products. Gross profit margin improved to 42.8% from 41.9%.

Outlook:

The year has started well with orders, revenue and

current trading ahead of the same period last year, which provides an

encouraging start to continue to deliver value for our shareholders.

My opinion:

I would like to study it further, but it strikes me as a somewhat

steady, mature business, albeit within a technological niche.

There are no balance sheet concerns, it pays a rising dividend, and so, despite the uninspiring growth, is likely worth the respectable 15x earning multiple at which it trades.

Tristel (LON:TSTL)

Share price: 165p (-7%)No. shares: 42.4m

Market cap: £70m

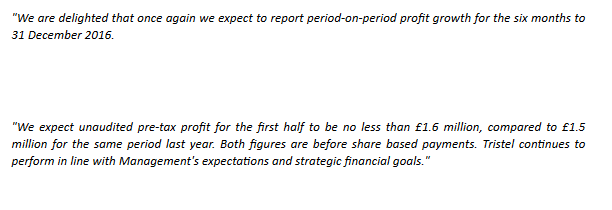

Yet more negativity I'm afraid, but the highly-rated Tristel is under pressure after an AGM statement suggesting pre-tax profit will only show a modest improvement in H1.

The manufacturer of hygiene products has been on a stunning sales growth trajectory, with great imrovements on the bottom line over the past three years.

Brokers have been forecasting pre-tax profit of £3.6 million for this financial year (ending June 2017)

(I am not sure if this forecast includes share-based payment charges, but the company assured the market that last year's charges were "unusually large" and would not be repeated in future years, so perhaps they will not be material anyway?).

These figures imply that up to £2.0 million in PBT will be needed in H2 to match forecasts for the full year. Which doesn't seem out of the question, based on £1.8 million achieved in H2 last year.

My opinion: In a situation like this, I prefer to keep my mind focused on the bigger picture, and not worry about a daily price move. The shares are still higher than they were a month ago.

One thing I'd concede is that the PEG does start to look a bit expensive if you extrapolate this H1 growth forecast ahead for the long-term, so I can understand why a few people might want to bail out at this juncture. But based on the reasonable possibility that it can still hit forecasts for the year, I'd be hard-pressed to say that the value of the company has changed radically in the last 24 hours.

In conclusion: I'd interpret today's pull-back as a healthy correction, nothing more!

See what our investor community has to say

Enjoying the free article? Unlock access to all subscriber comments and dive deeper into discussions from our experienced community of private investors. Don't miss out on valuable insights. Start your free trial today!

Start your free trialWe require a payment card to verify your account, but you can cancel anytime with a single click and won’t be charged.