South32 (ASX:S32) began life as a listed company in 2015, when it was spun out of BHP

Over the proceeding 9-years S32 has become a global diversified commodities producer with a focus on producing and growing their base metals portfolio. S32 produces a wide range of commodities including bauxite, alumina, aluminium, copper, silver, lead, zinc, nickel, metallurgical coal (used to make steel) and manganese.

Source: 2024 Half Year Results Presentation

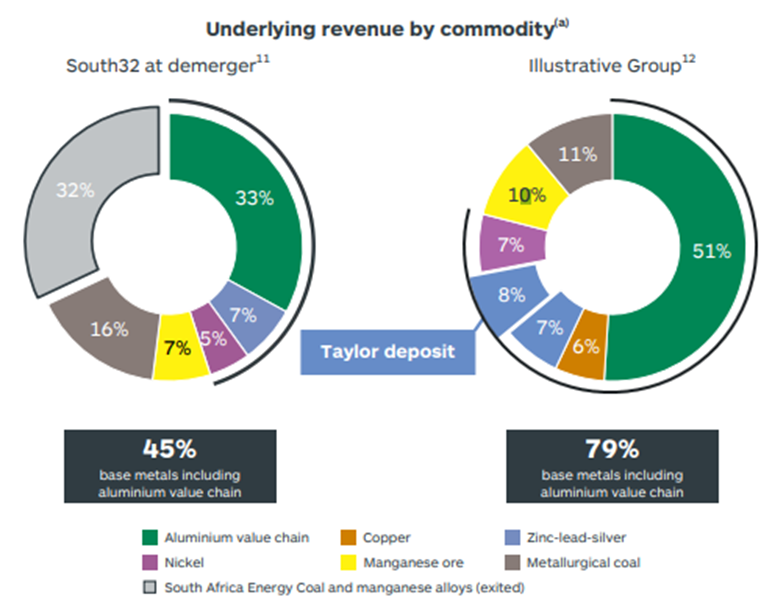

Since listing, S32 has transformed their commodities portfolio from 45% base metals to 79% base metals and added copper to the mix in FY22 by acquiring a 45% non-operational share in the Sierra Gorda open pit copper mine, located in northern Chile. Post the impending sale of their Illawarra Metallurgical Coal asset scheduled for H1 FY25 to Golden Energy and Resources Pty Ltd, their exposure to base metals will be 90%. The basis of this transformation, according to S32, is to increase their exposure to minerals that are critical for a low-carbon future.

Source: 2024 Half Year Results Presentation

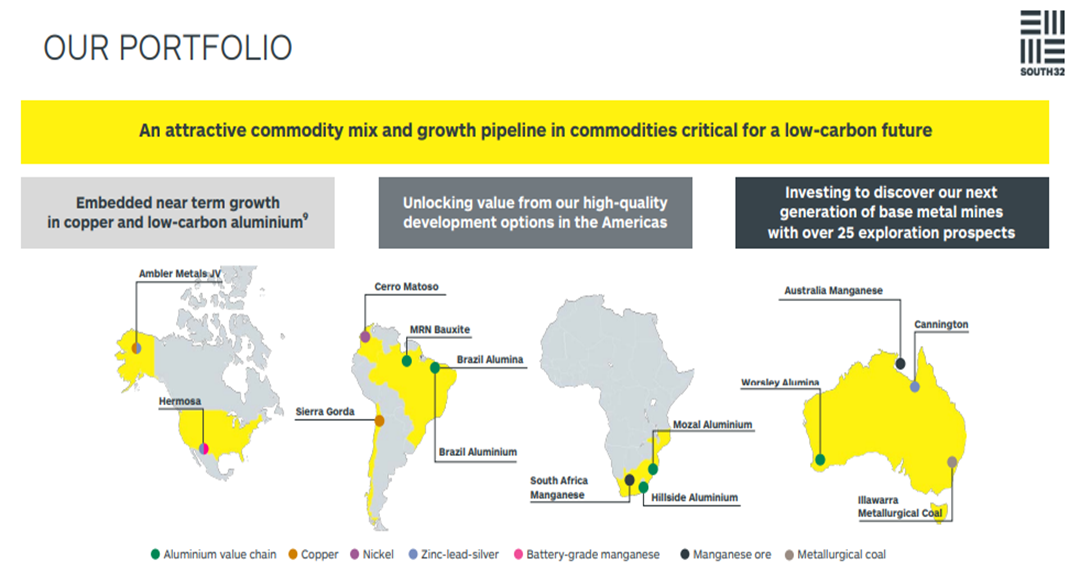

S32 also has two development opportunities in North America and several partnerships with junior explorers around the world. One of their North America development options is the Hermosa project located in Arizona USA. This project is home to the Taylor Zinc Deposit (also containing lead and silver). S32 announced the FID for the Taylor Deposit in Q1 2024. S32 sees Zinc as a critical part of a low carbon future as it is used to weatherproof (galvanise) building materials used in the construction of renewable energy infrastructure. According to S32, there is a supply deficit for zinc due to increased demand:

“With global zinc demand growth expected to outpace production by ~3Mt to 2031, we expect higher incentive prices for zinc as Taylor ramps up to nameplate capacity.”

S32 believe the Taylor mine has quite favourable economics and once up and running in H2 FY27 has a 28-year mine life, will hit nameplate production in FY30, and they have allocated US$2.2bn in capital expenditure to progress the mine into production phase. Once producing at nameplate levels, the mine is expected to generate average annual EBITDA of US$400m at a 50% EBITDA margin and produce US$320m of annual average net…