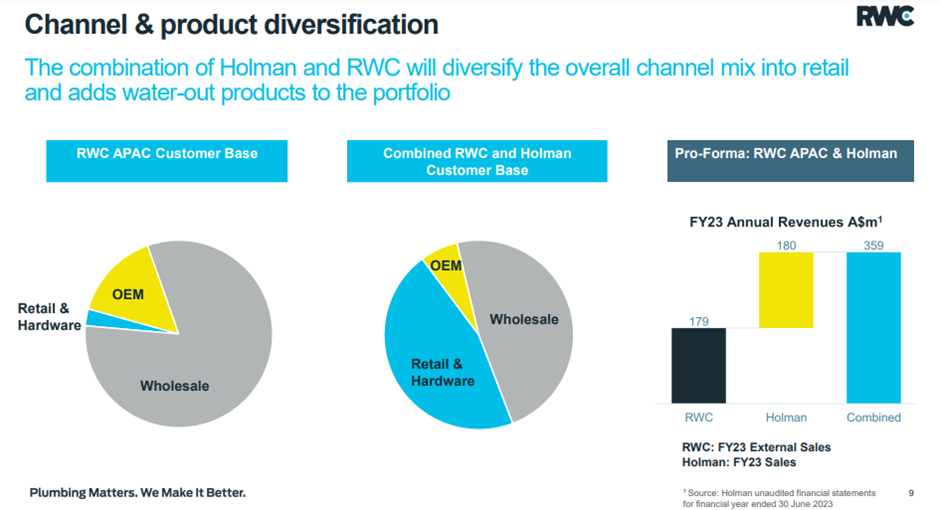

I like the look of the Holman acquisition. RWC will fund the AU$160.0m deal via their existing debt facility. The price tag represents 7 times Holman’s FY23 EBITDA, which is not cheap. So RWC have paid to play here and the acquisition although according to RWC will be EPS accretive in the first year is more of a strategic acquisition than a bolt on one.

The deal will double the size of RWC APAC business segment and substantially increase their retail offering in Australia and expand their wholesale offering too. Doing some rough numbers here. RWC had a profit margin of 11% in FY23. I would expect Holman to be similar. 10% of Holman’s FY23 revenue gives us a AU$19m profit for the business. Consensus has RWC generating a profit of AU$237m in FY25 adding the AU$19m form the Holman question gives us a profit of AU$256m. Which equates to EPS of 32c slightly above analyst consensus of 30c for FY25. Using RWC’s forward PE of 15 and applying this to the 32c EPS gives us a share price of $4.80. (Stock Held)