Revisiting RWC

This is the first stock we have revisited since its original publishing, with its products lasting longer than our review. Some see it as a boring stock, I get it. But it just keeps delivering strong results, despite the tougher environment, so I can’t ignore Reliance Worldwide (ASX:RWC)

RWC design, manufacture and supply premium branded water flow, control and monitoring products and solutions for the plumbing, heating, and remodelling industries. The company comprise of three business segments Americas, Asia Pacific, and EMEA.

The last I wrote about RWC on 15th March 2023, I was concerned about the build-up of inventory levels, high input costs hurting margins, and the jury was still out on their EZ-Flo acquisition. But I was confident RWC was managed well, and the enduring quality of the business would prevail. Also, RWC had given guidance that they expected both inventory levels and input cost to decrease throughout 2023, and the lingering effects of COVID on their supply chain would dissipate also.

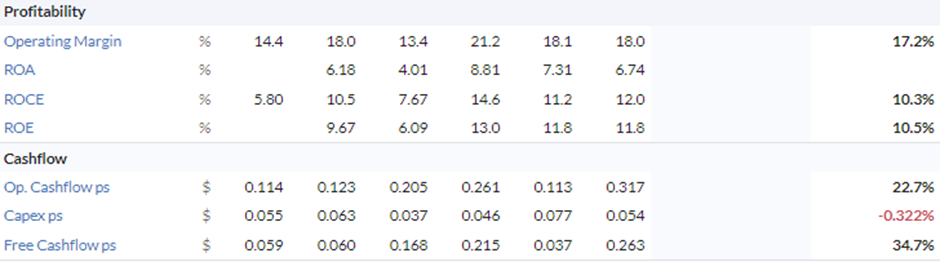

With this backdrop, RWC reported an increase in revenue, earnings, cash flow, and profits (underlying NPAT declined 4%) for FY23. While maintaining profitability ratios. However, more encouraging was that RWC reduced inventory levels from $316.0m in FY22 to $289.0m in FY23, on the back of two new product releases in the Americas.

Furthermore, margins were higher in the second half of FY23 on the back of lower input costs and RWC increased cashflow from operating activities by 110% to $250.0m. This was due to the reduction of inventory levels, realisation of cost savings, and synergies from the EZ-Flo acquisition.

Source: RWC 2023 Annual Report 21/08/2023

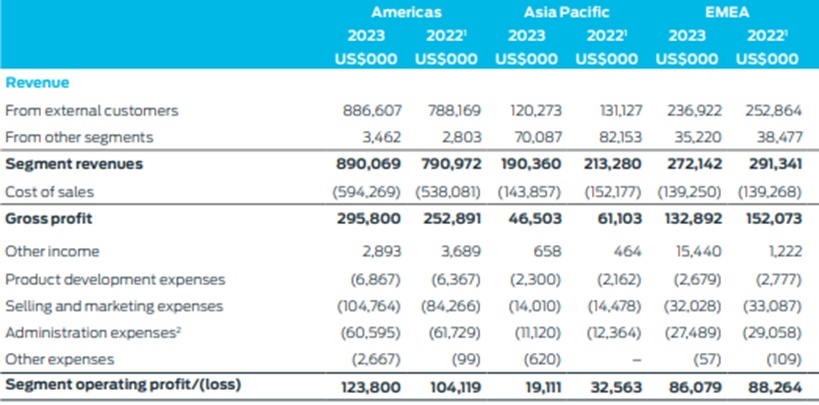

Looking at RWC’s segment breakdown for FY23, it was the Americas doing the heavy lifting as it was the only segment to report an increase in revenue and earnings. Revenue was up 13%, which includes a full 12-months contribution from the EZ-Flo acquisition. Excluding EZ-Flo revenue for the Americas was up 4%. Based on this and RWC maintaining their profitability ratios. It looks like the EZ-Flo acquisition is profitable and creating value for shareholders.

StockRank:

Looking at RWC’s StockRank and individual QVM indicators, most of the increase in their share price…