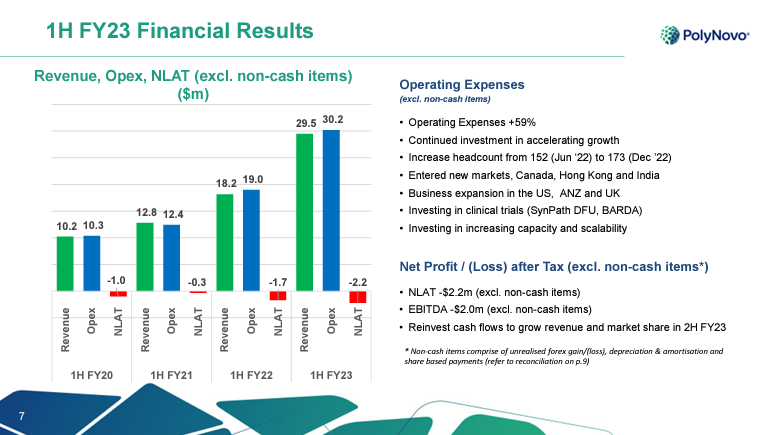

Bit of buzz round Polynovo (ASX:PNV) lately. For the last 3-4 years they have been tipped as one of the next big life-sciene/medical stock on the ASX, with their share price round the $4.00 mark back in late 2020, but retreating to $1.59 currently. They have nearly double their revenue in the last 3-years from $22.2m to $41.m, with estimated revenue of $94m to more than double for FY24 from FY22. Furthermore, they reported record sales growth of 67.5% to $27.3m on the pcp in their half yearly report released back in January 2023 and on June 7th they announced they achieved record monthly sales of $7.2m in May 2023. But (yes here I go again about cash flow) all this has yet to materialise in any cash flow (or profit) for the company and the slied below from their half yearly report presentation explains what is going on.

Expenses are growing just as quick as sales at this stage and is what you would expect from a company developing new medical technologies and expanding on a global scale, while competing for market share. It doesn't look like PNV are expecting a let up in operating expenses either, as PNV raised $53m in 1H23. This is despite revenue estimates set to more than double by FY24. On face value, it does look like they are close to generating positive earnings and cash flow and this would provide investors with some confidence and tangible evidence that profits are not far away and go some way to stabilising their share price.