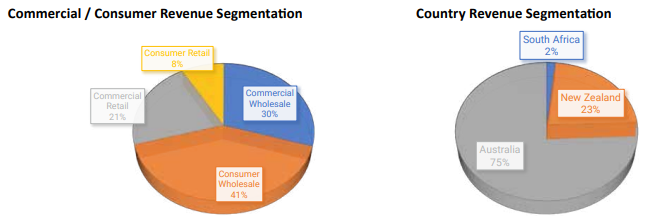

National Tyre & Wheel (ASX:NTD) are a distributor of tyres and wheels. They are the largest independent importer and wholesale distributor of tyres and wheels in Australia and NZ. They also have a presence in South Africa.

They are primarily a wholesaler but also have a chain of retail stores under the Tyreright brand. Primarily the business services commercial vehicles such as trucks and buses as well as agricultural vehicles and four wheel drives.

Source: National Tyre and Wheel, Annual Report 2023, 18/9/23

NTD have experienced strong revenue growth over the last five years. In addition to organic growth, a lot of the revenue growth has come via acquisitions. The acquisition of Tyres4U in August 2020 was a transformative transaction resulting in revenue increasing from $160 million to $460 million. They made a couple of smaller acquisitions in 2021, including Black Rubber, a truck tyre business and Access Alloys. In late September this 2023, they announced a deal to distribute Dunlop tyres in Australia and New Zealand. The deal is expected to be exclusive and they have the right to exit it if another distributor is appointed. The expected impact on revenue is an additional $118 million per year which is a significant jump from the current level of $583 million.

Whilst revenue has been growing strongly, and with this latest distribution agreement, should continue to do so, the path of profits has been a bumpy ride. EPS was $0.17 in 2021 but declined to $0.024 in 2023. Profits were impacted by substantial increases in cost of goods and freight and a disorderly supply chain. In the second half, supplier prices declined, as did international freight prices and the supply chain was more stable. Consequently, the second half of 2023 was much more profitable than the first half. Gross margin increased by 2% from the first half to the second.

The balance sheet remains strong. Net debt to equity is 112%, but this is inclusive of capital leases. The tangible assets to equity ratio, a measure of leverage which forms a component of the Health Trend, declined over the last year. Cash flow also improved over the last year and operating cash flow per share is well above EPS and has been consistently. That is a good sign of the health of a business.