Updated 22nd April 2021

Gear4Music Holdings - Balancing Covid-19 boost to longer-term structural trends

Gear4music Holdings (LON:G4M) hit a new low at 140p in March 2020. (lowest buy price 170p, New buy at 821p ). ( I hold a long position)

$G4M year-end results https://www.stockopedia.com/sh..., show 31% revenue growth and estimated ESP growth at 349% (based on EPS of 55p) as gross margins improved to above 29%. Clearly, Covid lockdown has contributed to this boost and accelerated the structural change to online retail. Brexit seems to have strengthened UK market dominance and warehousing and logistics Investments in Europe has accelerated overseas growth.

My forecast shows a slow down of growth in 2022 before picking up in 2023 as structural changes continue. (see below).

Sales Estimates FY21-25

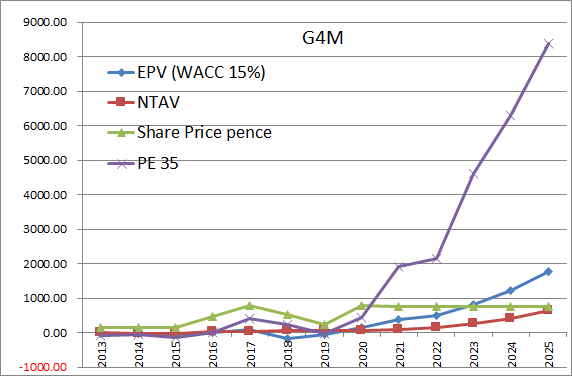

Evaluation model suggests 1280-2000p valuation for year-end 2021, (6800p upper end target for 2025). See the graph below

DYOR

BSV

22nd Oct 2020

Gear4Music Holdings - Online Retail

Gear4music Holdings (LON:G4M) hit a new low at 140p in March 2020. (lowest buy price 170p ). ( I hold a long position)

Gear4music Holdings (LON:G4M) half-year report shows continued top-line growth and margin and profit expansion, Sales growth of 42%, profit growth 60%.

With a growing dominant market share in the UK (24%) and growing sales in Europe, the company has overcome its logistics problems reflected in the share price rise. With operations in the UK and Europes, the company is well-positioned for Brexit, and with the continued trending of online retail, there seems like plenty of upside runway.

Sales Estimates FY21-25

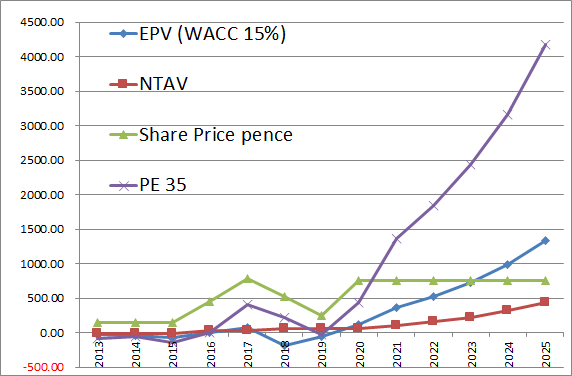

Evaluation model suggests 1100p valuation for year-end 2021, (4000p upper end target for 2025). See the graph below

As always DYOR, don't trust blogs like this one.

.jpg)