MYG FY24 Expectations

Introduction:

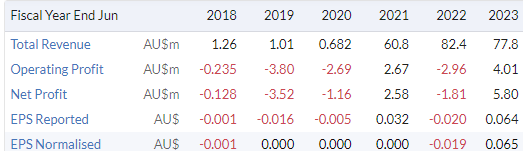

Mayfield group (ASX:MYG) reverse listed on the ASX in 2020 and assumed control of Stream Group and at the time of writing had a market cap of $71m, EV of $64m, and had 90m shares on issue with 62% classified as free float. Lindsay Phillips is their largest shareholder with a 45% holding in the company. He also sits on the MYG board as a non-executive director. MYG reported revenue and profits of $77.8m and $5.8m respectively in FY23.

MYG owns a portfolio of complementary, innovative companies in the provision of electrical and telecommunications products and services. They manufacturer custom electrical switchboards, kiosks and transportable switchrooms, and supplier of related services, for critical electrical infrastructure. A niche provider of wireless telecommunications and power quality solutions. End-to-end capabilities in engineering, integration, construction, project management and whole-of- life support services to renewables, mining, oil & gas, infrastructure, defence, utilities & essential services.

MYG operate as a single business segment for reporting purposes, with the group comprising of three businesses Mayfield Industries, Mayfield Services, and ATI Australia. Total revenue comprises of the sale of purchased products, revenue from services, and revenue from manufacturing products.

Financials:

Since their reverse listing in FY20, MYG have managed to increase sales, earrings and profits. The decline in sales from FY22 to FY23 was due to MYG focusing and expanding their manufacturing capabilities. Which according to MYG is lower revenue generating but higher margin. Which is reflected in their operating profits and net profits increasing.

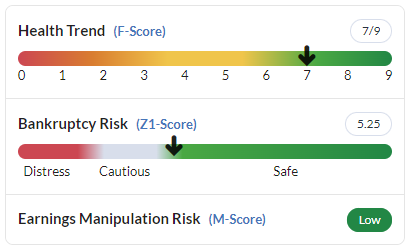

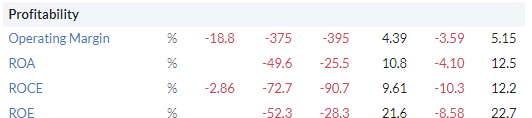

To date MYG’s has been unable to produce consistent earnings and profits but when they have, they do produce very respectable returns and margins for a services/manufacturing business. This can be seen in their return on equity, assets and capital being mostly above 10% or higher.

Also encouragingly to see is MYG’s ability generate operating and free cashflows, which have started to flow since FY22. This is a good sign, as it means MYG’s business is generating sufficient cashflows to fund their own capex, dividends, and growth.

This is reflected in MYG having a gross gearing ratio of 6.2%, interest coverage ratio 19. Indicating MYG are…