Market Musings 070123:

Off to a good start

So 2023 starts well for stock market investors after a terrible 2022

Weekly Podcast - 2022: Annus horribilis

In this podcast, Edmund Shing discusses the link between the unprecedented events in 2022 and the difficulties in financial markets.

1) What was the main trigger of the annus horribilis for financial markets?

2) Why does unexpected inflation cause so many problems in financial markets?

3) How bad was bad last year?

4) What were the challenges for central banks?

5) “Things can only get better”: is there hope for 2023?

Summary

Stock, bond markets benefit from weaker inflation prints

Weaker employment, wage momentum helps

World ex US stock markets generally in rising trends, above 200-day moving average

Emerging Markets back in focus: Hong Kong/China, Mexico, Indonesia

Sectors with strong momentum: European/UK Banks, Insurance, Gold and Copper Mining, US and European Industrials

How persistent can the post-2022 rally be?

Can this continue? In my view the key factor to watch at the moment inflation and associated wage growth in the US

inflation rates are clearly falling from admittedly very high levels, both in the US which has been happening for some time incidentally, but now also in the Eurozone.

Spanish inflation falls quickly Eurozone to follow

Source: Steno Research Bloomberg

Spanish inflation seems to lead Eurozone inflation by two months. I note from the graph above h that Spanish inflation has started to fall really quite sharply over the last couple of months. This suggests that eurozone inflation should follow suit in the very near term.

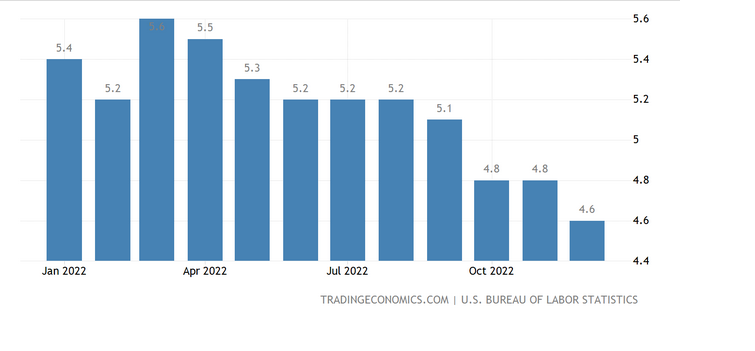

Friday’s good news on the US wage, employment front

In addition, the second associated factor to inflation is of course, wage growth. Here again, we are seeing incrementally better news in the US.

The first data point to note is that average hourly earnings growth, which is one measure of wage growth, has been steadily declining from its highs. Yes, it still registers just under 5%. Which is of course uncomfortably high for the US Federal Reserve. But it is falling and consistently.

US average hourly earnings continues to ease