A common theme heard among podcasts and the financial press is that the UK stock market is incredibly cheap against a US market that’s looking overvalued . A cursory look at the valuation of the market averages seems to back this up.

At Stockopedia, we publish the median ratios for the index constituents on each index page. Looking at the numbers is telling:

- The FTSE 350 index (the largest 350 stocks in the UK) has a P/E ratio of 14.5x, with a prospective growth rate of 8.5%.

- The S&P 500 index (the largest 500 stocks in the US) has a P/E ratio of 21x, with a prospective growth rate of 11.5%.

This suggests that the typical S&P 500 stock is on a 45% premium to UK stocks. That’s certainly eye-opening. A value investor could easily jump to the conclusion that the UK is a better hunting ground.

But life is rarely so simple.

While I am a huge skeptic of the accuracy of analyst forecasts, these US stocks are forecast to grow at a 35% higher rate (11.5% to 8.5%). So at least some of the US premium is justified.

Alas, all is not as it seems

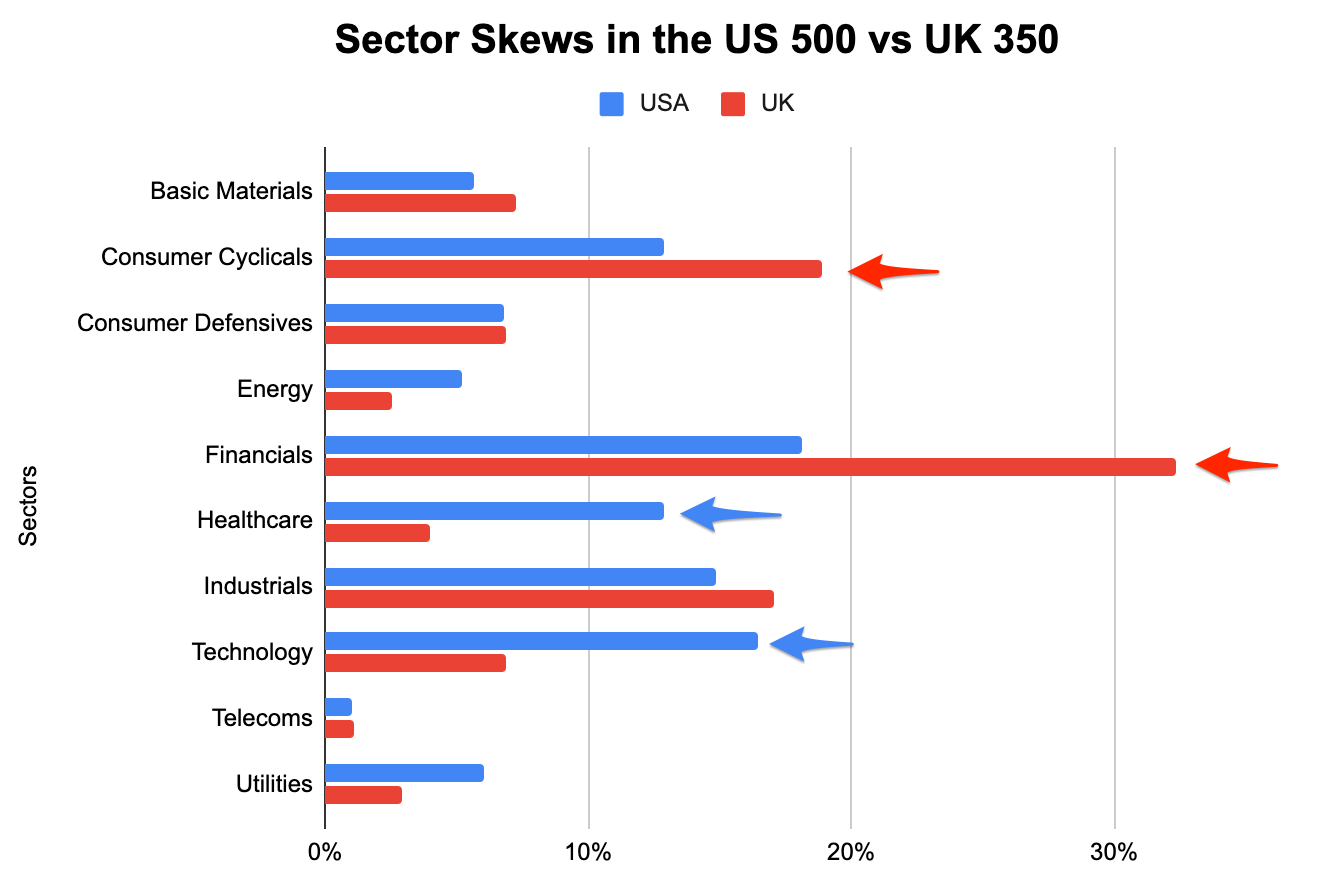

These numbers hide the fact that the indices contain very different sector compositions.

Even after removing the funds and trusts from our local UK index, there is a far higher count of financial and consumer cyclical stocks. These sectors often justify lower valuations. In the US, there is a higher skew to Technology and Healthcare stocks, which often justify higher valuations.

A hefty US premium?

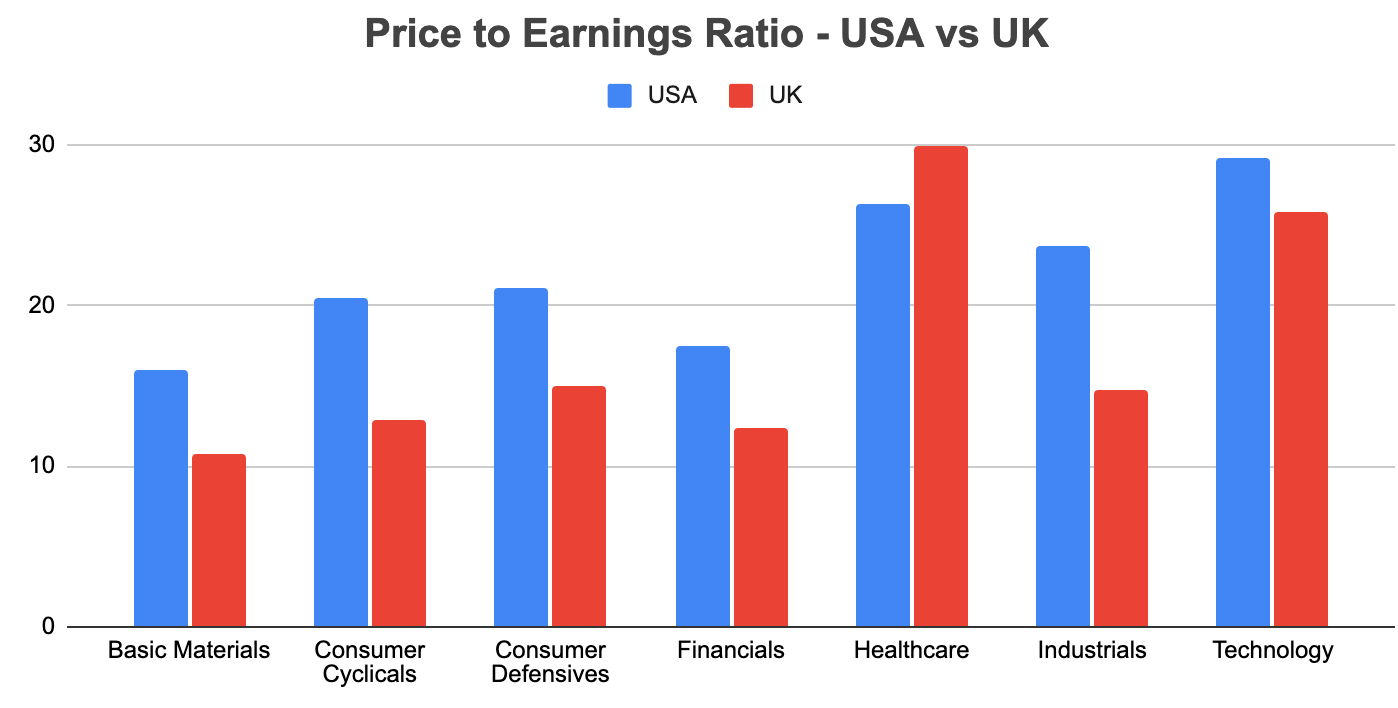

To remove these sector skews, it is instructive to investigate valuations across sectors.

I’m going to ignore the Energy sector (as the average constituent in both regions is forecasting an earnings decline), and also the Telecom and Utility sectors as they are small across these regions. That leaves seven sectors.

On a P/E ratio basis, six of the seven remaining sectors are at a significant valuation premium in the US. Only the Healthcare sector stands tall in the UK.

Backed by stronger US growth?

Some of those US valuations are vertigo inducing, especially in technology with a P/E of almost 30x. But those valuations are backed up by significant earnings growth advantages. The chart below highlights US growth rates well above the UK in…