This stock seems to be taking off. Although it doesn't pay a dividend it has a great "moat". It is a world leader in several areas such as photoelectronics and wafer manufacture. Links to several helpful reviews have been posted on the LSE discussion board under IQE.

I am long in this share.

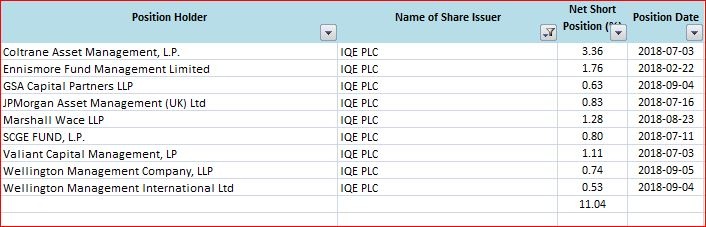

Recent post page 4 LSE discussion board for IQE

"Investor interest is growing - the CFO has recently been presenting in the USA and says that many analysts have been very interested in hearing what IQE have to say. Interestingly the American analysts appear to understand the proposition better than their UK andEuropean counterparts, but also in the UK there has been a recent clamour to meet and discuss the company. I have long held the notion that the recent SP growth has been driven in large part by US investors, that would appear to be a situation that's growing, certainly IQE is going from a proposition that was uninteresting to a situation where IQE are literally inundated with interest from the analyst and investment communities :-)

I asked about utilisation rates which were quoted as being 50% last year and also the ability to respond to surges in demand. As expected no direct answer was given to utilisation other than its obvious the rate has gone up significantly :-) , Interestingly in response to Hammerd's question it only takes 9 months from reactor install to it being fully productive.last years CAPEX increase was to supply to the demand they knew was coming folks, I expect that R+D and CAPEX will have to increase to supply the demand- which is great. There are no plans for acquisitions, but of course no- one should ever say never, just in case an opportunity arises, but none is imminent.

Lots can be gleaned from body language, All The board were present, it's blindingly obvious unless they are the best actors in the world ( and why would they) that things are going extremely well.

The point was made that the political shenanigans and Brexit have no impact on investment in the CS cluster . Simon Gibson made the point that the influential MIT publicly state that the Compound Semiconductor industry led by IQE is WORLD CLASS compare to its completion :-)

Links from LSE pages…

The issue with IQE (LON:IQE) as I see it is that too many people focus on the demand side of the equation and speculate about Apple in particular. The reality is that there is no shortage of demand for the wafers IQE produce. The problem is the supply side where the board have been fairly cautious in the number of machines they have deployed. They are working at reducing down time by moving productions between factories, so machines will not have to switch between photonics and wireless, but the real challenge for me is whether they can demand higher premiums and/or work their way up the value chain. Until that happens they are a little stuck with the volumes they can produce, and while that is growing, each machine procured reduces profit, which enables the shorters to cry manipulation, and a large PI base to be manipulated. Also, it just seems that every set of results there is something exceptional that stops profits being all that was hoped for: customers reducing inventory, extensive product development for major customer etc. I hold, for my sins!