Infomedia (ASX:IFM) are a global player in the automotive industry providing SaaS (Software as a service) and DaaS (Data as a service) products to car manufacturers, dealers, and OEM’s.

Over the years their business has evolved from mainly a parts and inventory software provider to offering a full suite of SaaS and DaaS products that provide analytical, marketing, predictive servicing, parts inventory, and maintenance solutions.

All this is aimed at capturing the global trend in connected cars and allowing car manufacturers and dealers to own the lifecycle of a customer/car relationship by providing pre-emptive servicing, repair/maintenance and resale solutions and recommendations.

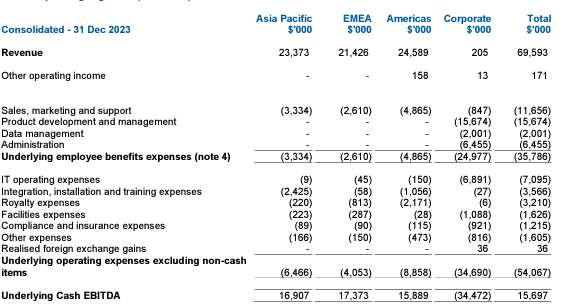

Source: IFM Interim Report 2024

The last time I looked at IFM they were riding high off the back of their 2023 interim results, and it looked like they had shaken off the effects of COVID, as they continued to implement their new strategic business direction. This change of direction was needed when one looks at a long term (5 year) chart.

ASX:IFM 5 year Weekly chart

Given IFM have just dropped their 2024 Interim Report. I thought it time to have another look under the hood and take them for a test drive.

IFM comprises of three business segments Asia pacific (APAC), EMEA, and Americas. Each of these business segments was basically responsible for generating a third or revenue and earnings for the half.

FY23 revenue came in at the top end of guidance at $130m, up 8% on the previous corresponding period (pcp), and they reported a net profit of $9.5m up 16% on pcp. Moving forward to their 2024 interim, IFM reported total revenue of $69.6m, up 11% on pcp. Annual recurring revenue accounted for 99% of 2024 interim revenues, and before one off costs net-profit for the half was $9.6m (reported $5.1m) up 35% on pcp. Based on these results, it would seem IFM are heading in the right direction.

StcokRank:

Once again, the quality of IFM is on show for all to see, with quality sitting at 96. But as noted the last time I looked at IFM, (and this is no secret) the challenges are reflected…