One of the challenges of investing in the stock market’s smallest companies is that many lack good quality research coverage. For some investors, this sort of information vacuum is enough to send them running for the hills. But for those prepared to do their homework, it can offer a chance to profit where others fear to tread.

To illustrate the potential power of smaller companies, it’s worth looking at the performance of a simple micro-cap strategy tracked by Stockopedia in recent years. Since 2012, the James O’Shaughnessy-inspired Tiny Titans screen has delivered consistently strong returns, including a 74 percent gain in the UK over the past two years. It’s achieving those results with shares that are valued at less than £150 million (and often much less) - so they’re right at the smallest end of the market. We’ll explore this strategy further in a moment.

The case for small-caps

There are some strong arguments in favour of having a small-cap allocation in a portfolio. Research into long-run investment returns shows that small-caps generally outperform large and mid-caps over time.

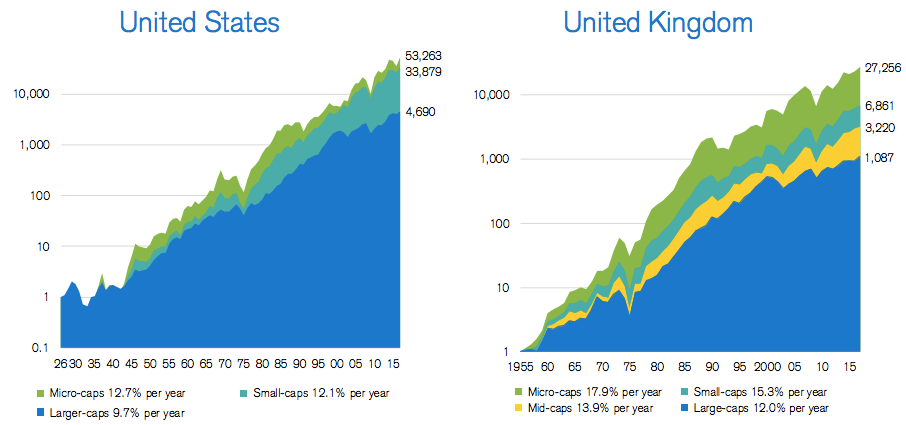

This is regularly shown in analysis by Credit Suisse and academics from London Business School. Their charts below show that between 1926 and 2015 in the US, and 1955 and 2015 in the UK, the smallest stocks beat the rest of the market overall.

Source: Credit Suisse

Findings like these tally with the views of academics that smaller stocks outperform over time - even though, individually, they tend to be more volatile.

Luminaries like Eugene Fama and Kenneth French first argued this in the early 1990s. And as recently as 2015, researchers at the the hedge fund AQR showed that you could profit from the small-cap size premium by focusing on high quality.

But O’Shaughnessy’s original Tiny Titans strategy takes a different approach to finding the best prospects among small, under-researched stocks. In his 2006 book, Predicting the Markets of Tomorrow, he set out the case for investing in small-caps with a strong blend of attractive value and strong price momentum.

O’Shaughnessy’s strategy focused on companies that were cheap based on their price-to-sales ratio (which has to be less than 1.0x). He argued the P/S was a harder ratio for management to manipulate than other…