Graham did a great post on yesterday's SCVR on Hargreaves Lansdown (LON:HL.)'s interim results. He and I seem to have come to pretty much the same conclusion. But we certainly got there taking different route's :-). Here's my reading of the results after sitting in on the analyst presentation yesterday.

Interim results were 'meh'. But make no mistake, the (relatively new) CEO is implementing a big shakeup. The opportunity is there. This is all about execution.

Hargreaves Lansdown’s interim results for the six months to 31 Dec 23 (H1-24) were badly received by investors. The share price fell over 7% on the day of the release.

But I reckon too much of a focus on some disappointing metrics in the short term might be a mistake. The real meat of the release and the analyst presentation was in CEO Dan Olley’s changes to HL, and his plans for future. There was a refreshing honesty about HL’s weaknesses, a clear message that big changes are underway, and signs that the ‘old way of doing things’ is under some pressure.

I’ll tackle the results first, then dive into the updated strategy and execution.

Slow-ish growth, but not THAT bad

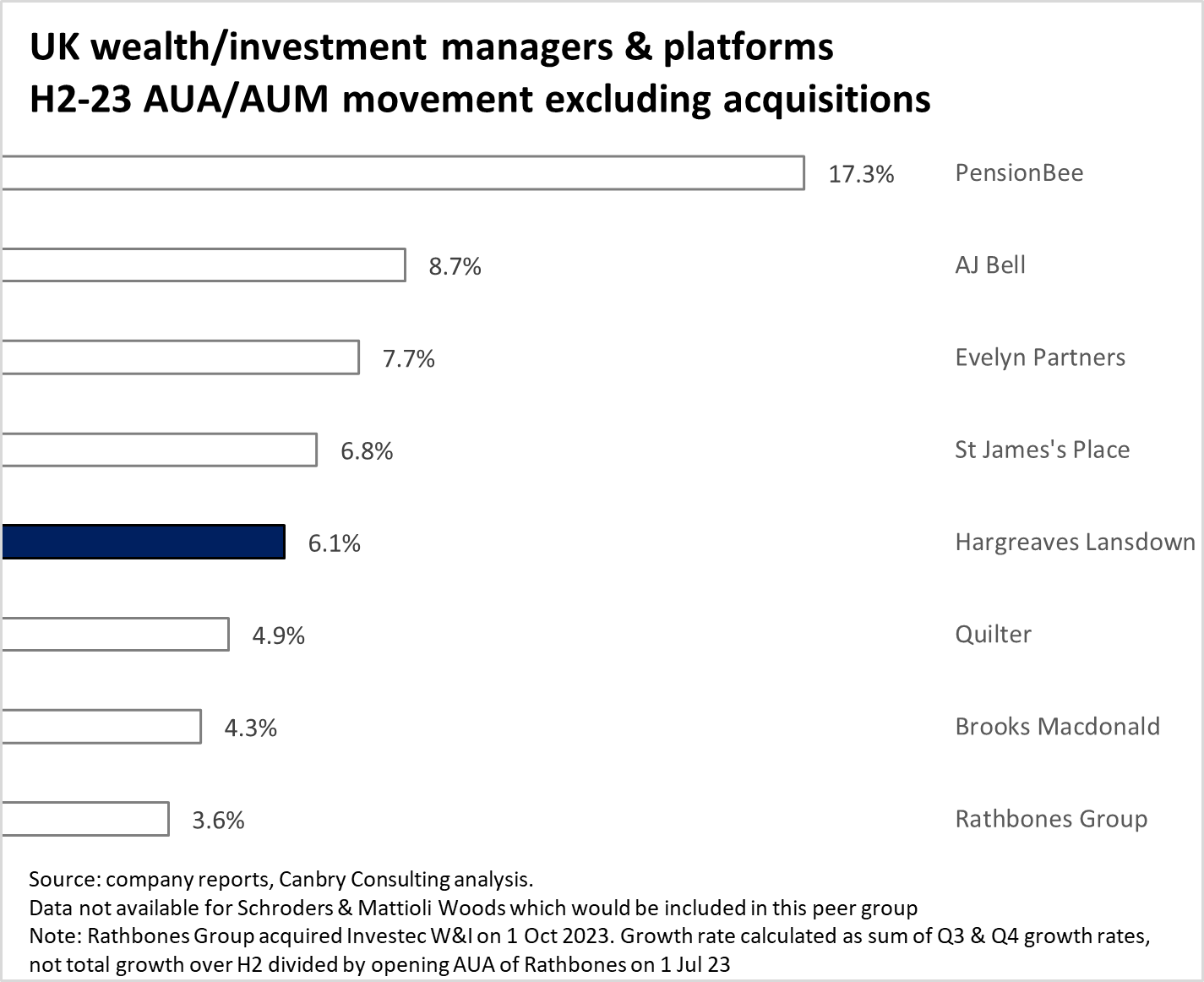

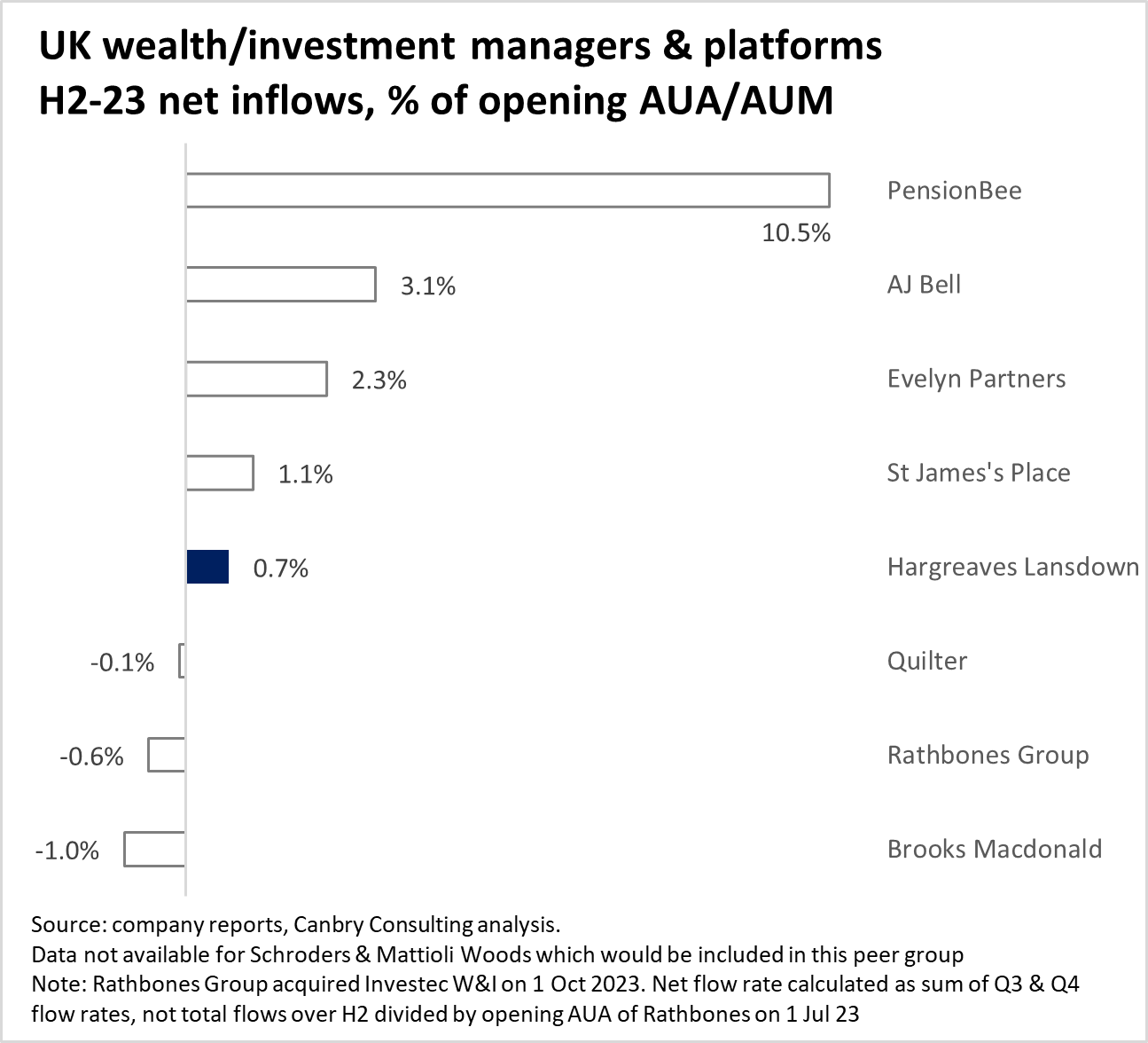

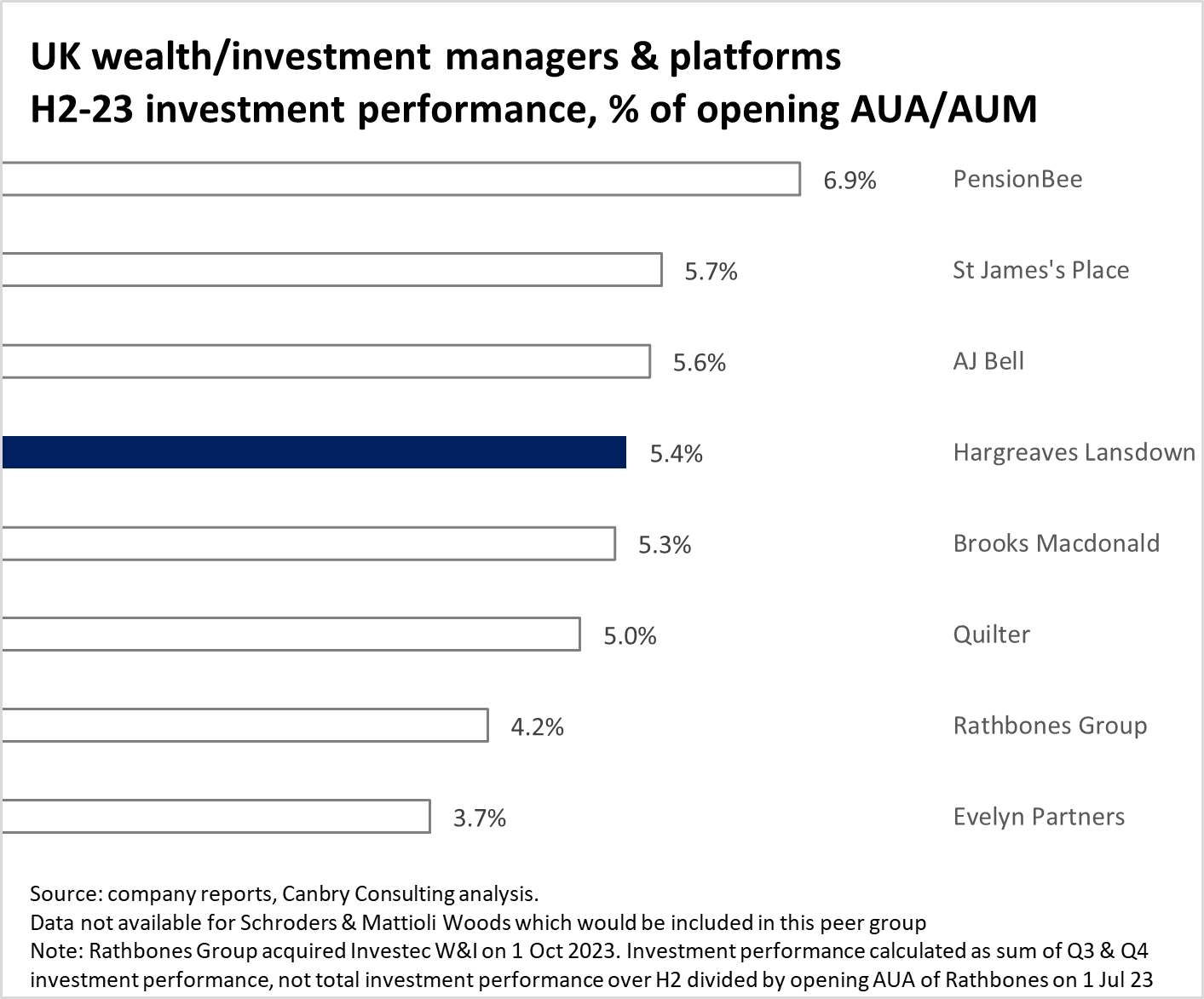

Net new business AUA for the six months was +£1.0bn. Markets were a tailwind which added £7.2bn, bringing total AUA to £142.2bn (up 6% over six months).

The new business number was probably the biggest disappointment for investors, which was down 38% year-on-year and Q2 (+£0.4bn) was down on Q1 (+£0.6bn).

But in fairness, it was a period of tough trading conditions with a grim macro-economic environment, and nervous investors. For a large incumbent, the growth rates weren’t that bad compared to peers. (Note: H2-23 used in the charts below refers to calendar H2-23, and equates to FY H1-24 for HL).

Additionally, net new clients were substantially higher in Q2 (11.9k) versus Q1 (8.2k), although still well below the quarterly average of FY23 (16.8k). Over the half-year period HL attracted more net new customers (20k) than competitor AJ Bell (18k), although AJ Bell’s customer growth rate is far higher as it has a smaller customer base (484k vs the 1.8m of HL).

There is some nuance to HL’s net new business flows though.…