FTSE 250 oil and gas producer Harbour Energy (LON:HBR) is now the largest independent oil producer in the North Sea. I reckon it could also become a FTSE 100 member by the end of 2024, if the recently-announced $11.2bn deal to acquire the majority of Wintershall Dea’s production assets goes ahead as planned.

Harbour is also currently one of the most highly-ranked UK shares in the Stockopedia universe, with Super Stock status and a StockRank of 98 at the time of writing:

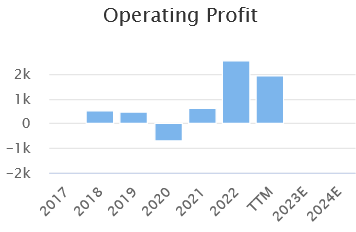

Recent financial performance has been excellent. Soaring gas prices in 2022 boosted profits:

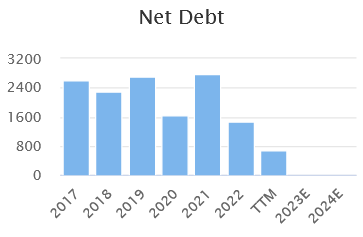

These windfall profits also enabled Harbour to accelerate its planned debt repayments. Net debt fell from $2.8bn at the end of 2021 to less than $800m at the end of June 2023:

The word transformative is sometimes overused in investment commentary, but I don’t think it’s an exaggeration in terms of the potential impact of the Harbour/Wintershall Dea combination.

I looked at Harbour’s smaller North Sea rival Serica Energy (LON:SQZ) in a recent piece, following that company’s own transformative acquisition with Tailwind Energy.

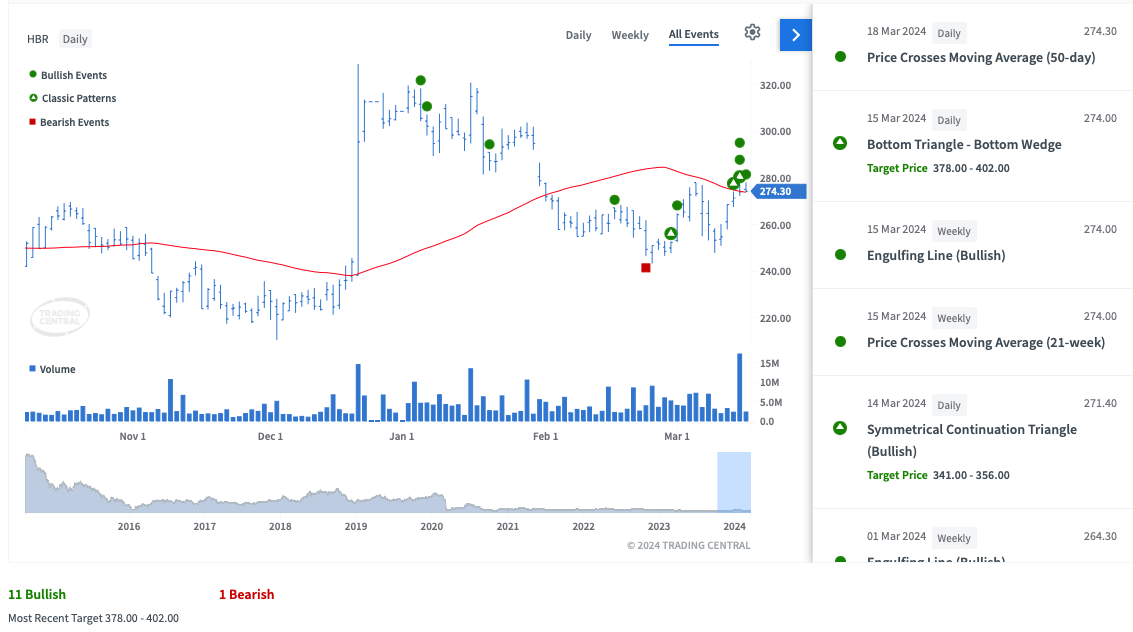

Given the recent news and share price action from Harbour Energy, now seems a good time to take a closer look at Harbour and at the Wintershall Dea deal.

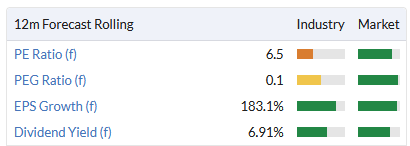

With a rolling forecast P/E of 6 and a dividend yield of nearly 7%, Harbour’s value metrics appear quite attractive:

Does Harbour offer an opportunity here for private investors, or do the apparently favourable terms of this deal hint at pitfalls to come?

Harbour Energy: a big roll-up

Private investors who have been in the UK markets for a while are likely to remember Premier Oil. This business was a well-established North Sea operator and also had assets in certain Asian markets.

My impression was always that Premier was a good operator, but its financial position was weak.

Like a number of others, including Enquest (LON:ENQ), Premier overcommitted to expensive development projects ahead of the 2015/16 oil sector crash. The group was then left with unmanageable levels of debt, but some attractive assets that gradually came…