You may not be familiar with the company GWA (ASX:GWA), but you probably make use of their products. They make toilets, sinks, showers, tubs and other water products for the bathroom, kitchen and laundry. They are behind such brands as Caroma, Methven, Clark and Dorf. They design their own products and sell them to both residential and commercial customers. The products are manufactured by suppliers in Asia and Europe.

Source: GWA, FY23 Results presentation, 14/8/23

Residential sales are largely driven by new builds and renovations and likewise for commercial. They generate approximately 60% of their sales revenue from the renovations and replacement segment in Australia. Sales are also impacted by the decisions of merchants to increase or decrease their stock of GWA products. About 60% of their revenue comes from their four largest customers, with the single largest customer accounting for 24% of revenue.

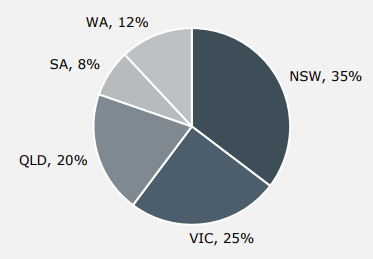

Revenue is predominantly derived from Australia at 82%. 10% comes from New Zealand and a further 8% from the UK. Within Australia, NSW is the largest market at 35%, followed by Victoria at 25% and Queensland at 20%.

Source: GWA, FY23 Results presentation, 14/8/23

In FY23 revenue declined by 1.6% impacted by the general economic slowdown with rising interest rates and inflation causing people to think twice when it comes to renovations and look for value options where possible. All three markets registered declines, with the largest declines coming from New Zealand due to the recession there. Some of the declines in volumes sold were able to be offset by increased prices charged.

You need to dig into the accounting a bit to understand what happened with profits. Reading the presentations from management, they state that FY23 normalised profits declined about 6%. However, statutory profit increased 23%. The reason was a 15m pre tax significant item in FY22. $10m related to a project to upgrade ERP/CRM software and $5m to the closure of the China sales operations. I am sceptical about companies treating software projects as an abnormal item. It is a normal part of doing business. In my view, it should either be capitalised as an asset or put through as a normal expense.

Importantly, the FY23 accounts had minimal significant items and therefore the healthy operating margin of 17% is…