SHARE PRICE: £6.82 (DOWN 16%)

Trading Update

Dialight is on the wrong end of the stick this morning with the shares down 16% (as of 9 am).

Their trading update was short as management stated that: “Due to short-term production challenges, we now expect EBIT for the year ending 31 December 2017 to be in the range of £13.5m to £15.5m.”

But they have made significant technology upgrades in their two largest product lines: Area Light and High Bay.

Going back to their full-year results, Dialight saw no improvements in unadjusted EBIT. Operating profit came in at £13.1m, but the exceptional costs caused an operating loss of £3.3m.

Maybe, short-term production challenges are code for “expect a big writedown.”

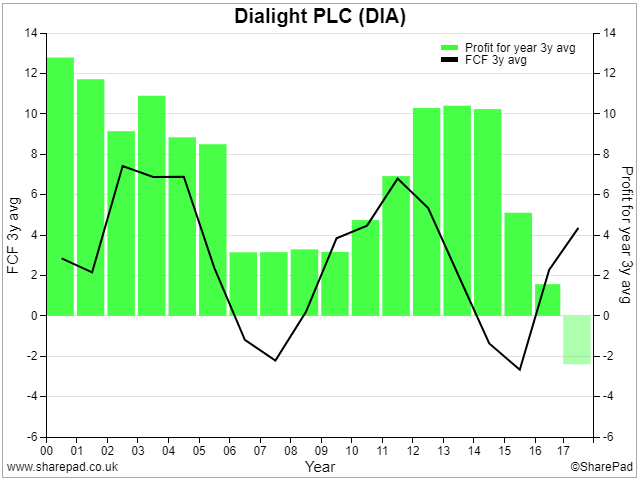

Historical Performance

It has recently regained their sales level that was last seen in the early 2000s. That’s because it disposed Roxboro Group back in 2005.

If you assess their historical profits and free cash flow trend, using 3-year average, then Dialight is a cylindrical business.

Balance sheet and cash flow

Good to see it has zero borrowings, which leaves them with net funds of £8m. Although peak funds were £15m in 2013.

Unfortunately, it has stopped paying dividends.

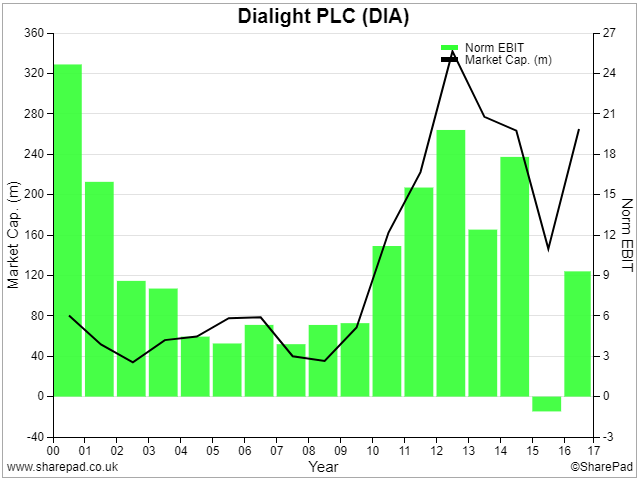

Market capitalisation four-times higher

If we are going to compare apples with apples, we got to look at profit earnings back in their heydays and compare it today by averaging out earnings over a decent period.

Investors may not realise this, but between 2000 and 2004, their average market capitalisation was £50m when average profit was £10.5m.

Contrast this to the past four years, their average market capitalisation is £230m with average profit of £3.5m.

So, between 2000-04, Dialight average PER is 5 times, whereas 2012-2016 gives a PER of 75 times.

Brokers’ forecast

According to Investec, N+1 Singer and Peel Hunt, all three are forecasting turnover to grow from £180m to £220m by 2019.

Meanwhile, they see pre-tax profits rising from £10m to between £30m and £40m.

And finally, they envisage EPS rising to 80 pence from the current normalised EPS of 30 pence.

Are their truths in these forecasts?

One…