Good morning! The FTSE is set to open up by another >1% this morning, over 8400, as the recovery continues.

1pm: I'm wrapping this up for now, thanks everyone!

Companies Reporting

| Name (Mkt Cap) | RNS | Summary | Our view (Author) |

|---|---|---|---|

Reckitt Benckiser (LON:RKT) (£33.7bn) | “We maintain our outlook for full year 2025 whilst recognising the more challenging macro outlook.” | ||

Fresnillo (LON:FRES) (£7.7bn) | Started 2025 in line. Full year guidance unchanged. Q1 silver production -8.4% vs Q1 2024. | ||

Babcock International (LON:BAB) (£3.8bn) | FY March 2025 “strong”, rev £4.83bn (organically +11%), adj. operating profit £363m (+17%). Contracted backlog of £10.1bn at 31 Mar 25, versus £9.5bn at HY25. | AMBER/GREEN (Roland) [no section below] Today’s update confirms FY25 results should be largely as expected, with a modest improvement in margins. The FY26 outlook seems positive, with £1.8bn of recent contract wins highlighted. | |

Croda International (LON:CRDA) (£3.8bn) | Rev +8%, Q1 PBT in line. FY25 outlook unchanged, adj. PBT £265-295m (FY24: £260m). Local manufacturing is expected to mitigate tariff impact, but there will be a tariff surcharge for customers where needed. | AMBER (Roland) [no section below] I’ve been waiting a long while for signs that this chemicals group may have reached a turning point. I wonder if today could be that time. Reiterated FY25 guidance suggests a return to profit growth, after two years of declines. The Q1 update highlights sales growth in all three divisions, with improving factory utilisation. I wonder if Croda’s Falling Star styling could soon shift to a neutral or positive style. I’m going to take a neutral view today to reflect the forward P/E of 18 and macro risks, but I’m encouraged by this update. | |

Quilter (LON:QLT) (£1.9bn) | AUMA broadly unchanged during Q1 at £119.6bn. Net inflows £2.2bn offset by market declines. | ||

Hochschild Mining (LON:HOC) (£1.6bn) | Peru: solid performance. Argentina: easing of FX controls to improve cost position in long-term. | ||

Ibstock (LON:IBST) (£688m) | Core revs in line. EBITDA margin fell as expected. Full year exps unchanged (incl. H2 weighting). | ||

PayPoint (LON:PAY) (£458m) | FY March 2025 in line with adj. EBITDA c. £90m, adj. PBT in line and net debt <£100m. | GREEN (Graham) [no section below] A brief, comforting update. The stock is nearly 10% cheaper than it was when I covered it in January. I was positive on it then and I see no reason to change my stance after an in line update. With a moderate debt load (£109m) and a highly cash-generative set of businesses whose collective profitability is growing, I remain a long-term fan of this one. The StockRank is 96; making it a “Super Stock”! | |

Hollywood Bowl (LON:BOWL) (£452m) | H1 revenue +8.4%, LfL revenue +2.1%. Net cash £23m. 2035 target for 130 centres unchanged. Confident in outlook for FY2025. | AMBER/GREEN (Roland) Despite some concerns about weak LFL growth and possible margin pressure in the UK, my overall impression of this update is positive and I'm opting for a moderately positive view. If current profitability can be maintained and the group can achieve its growth targets for the next decade, I think the shares could be worth a closer look at current levels. The StockRanks are neutral. Interim results are due next month. | |

Nichols (LON:NICL) (£440m) | Q1 rev +1.2%, in line. Net cash £60m. Expectations unchanged (rev £178.9m, adj. PBT £33.1m). | ||

THG (LON:THG) (£420m) | £400-600m bid for Myprotein from Selkirk (LON:SELK) was “wholly unsolicited, largely unfunded”. Rejected. | PINK (offer rejected) RED (Graham) I remain RED on THG for reasons explained previously. As for Selkirk, it raised £7.5m in November 2024 with a view to making an acquisition (it currently has no business operations). The unfunded approach to THG appears to me to be an exercise merely in creating publicity, as they search for a more realistic deal. There is a complicated web of relationships to be aware of, e.g. Kelso group (LON:KLSO) owns 18% of Selkirk, and 25% of Kelso’s portfolio also consists of THG shares. Additionally, THG's CEO is the second-largest Kelso shareholder. I would be extremely cautious when it comes to touching any of these shares as an outside investor. | |

Ab Dynamics (LON:ABDP) (£394m) | Rev +11%, adj. op profit +21%. Potential macro disruption but adj. op profit for FY2025 to be in line. | AMBER (Megan) | |

B.P. Marsh & Partners (LON:BPM) (£263m) | BPM has taken £10m/8% holding in iO Partners, a buy-and-build operator in private credit. | ||

Supreme (LON:SUP) (£199m) | FY25 results to be in line with market expectations, with revenue of £235m and adj EBITDA of “at least” £40m. Net cash at year end. Outlook for FY26 is also in line with expectations. | AMBER/GREEN (Roland) Given SUP’s reasonable valuation and decent track record, I’m going to maintain our moderately positive view. | |

Foxtons (LON:FOXT) (£172m) | Q1 rev +24% with sales revenue +73% ahead of Stamp Duty deadline. Confident outlook. | ||

Capital (LON:CAPD) (£137m) | Q1 rev -10.5%, in line with exps. H2 weighting. FY25 rev guidance of $300-320m unchanged. | ||

| Serabi Gold (LON:SRB) (£132m) | Placing & Board Change | Two of Serabi’s major shareholders (Greenstone and Fratelli) have collectively sold 15.7m shares, raising £21.2m. The sale is equivalent to 20.7% of SRB’s share capital. Fratelli retains a 9.99% holding, Greenstone no longer has a position. Board directors representing both investors have now stood down. | AMBER/GREEN (Roland) [no section below] Serabi shares have risen fivefold in two years. It seems that these two substantial shareholders have decided to take some profits. Of course, there are investors on the other side of this deal, notably Brazilian PE firm Starboard Asset Ltda, which recently took the other 20% of Greenstone’s former 25% holding. With Serabi trading on a P/E of 3 I took a moderately positive view on this Super Stock on 14/4, while highlighting the possible downside risk if the gold price weakens. That view is unchanged today, although personally I am inclined to be cautious re. gold. |

Anexo (LON:ANX) (£72m) | Possible offer from DBAY in the form of loan notes and shares in new entity. No details provided yet. | PINK | |

System1 (LON:SYS1) (£68m) | FY25 rev +25% to £37.4m. Adj PBT +68% to £5.2m. Outlook: growth could slow due to macro. | AMBER/GREEN (Graham) Downgrading my stance on this one notch to reflect a cloudy outlook with lower growth and some risk to forecasts. On the plus side of the equation, I'm much less concerned by the company's valuation here than I was previously. | |

Ten Lifestyle (LON:TENG) (£58m) | Net rev +3%, PBT +£0.8m to £1.1m. Net cash. FY exps unch, new contracts underpin growth. | ||

Argentex (LON:AGFX) (£52m) | Liquidity worsened y’day, Seeking “immediate cash injection”. In bid discussions with IFX Payments. | PINK (RED) (Graham) I doubt that IFX will need to pay much to pick up Argentex's existing equity. If the potential deals fall through, I suspect that this is a zero. | |

iomart (LON:IOM) (£29m) | FY25 to be in line, adj PBT £6.5m. Outlook: margin dilution, broker FY26E EPS “break even”. | ||

First Property (LON:FPO) (£18m) | PBT to significantly exceed exps due to one-off events. Underlying trading now profitable. | ||

Finseta (LON:FIN) (£17m) | Rev +26%, PBT +7.7% to £1.4m. Active customers 17% to 1,059. Outlook: strong YTD, in line. | ||

Northcoders (LON:CODE) (£8.7m) | Rev +24%, adj EBITDA in line at £1.0m. 3,976 people trained (FY23: 2,852). Outlook mixed. | ||

Pebble Beach Systems (LON:PEB) (£7.5m) | Order intake +24% to £13.6m, rev -7% to £11.5m. PBT loss £1.3m. Outlook: YTD trading in line. |

Graham's Section

Argentex (LON:AGFX)

Suspended yesterday at 43.2p (£52m) - Response to Media Speculation & Financial Position - Graham - RED

Following on from yesterday’s bombshell announcement we have an update today on the unfolding situation at Argentex.

Yesterday, it was clear that the company was in some difficulty but it wasn’t clear exactly how serious it was - whether it was something less serious that could be overcome with a little luck and a little patience, or whether it was something that the company could not recover from.

Today’s update spells it out: the company needs cash now and a fire sale is on the cards with multiple suitors having already contacted the company.

A brief outline of today’s update:

Three potential offerors have made non-binding proposals.

The offerors are

A vehicle owned by Pollen Street (LON:POLN)

IFX Payments (another payments/FX firm catering to businesses and private clients), and

Terry Clune (a fintech entrepreneur) and Harry Adams (founder-CEO of Argentex who unceremoniously left the company in October 2023).

The Pollen Street and Clune/Adams proposals have been rejected already, but discussions with IFX are “at an advanced stage”.

Unfortunately, the financial emergency has deteriorated further in the last 24 hours:

As detailed in the announcement on 22 April 2025, Argentex has been exposed to significant volatility in foreign exchange rates which has resulted in a rapid and significant decline in its liquidity position as a result of increasing margin calls on its FX Forward and options book. This liquidity position further deteriorated yesterday and the Company remains in regular discussions with its Liquidity Providers.

This further reduction in liquidity necessitates an immediate cash injection to ensure the Company's continued solvency, without which the Board would have to take immediate steps to secure the Company's future and protect value in the business for the Company's creditors and other stakeholders.

Whenever “creditors and other stakeholders” are being prioritised, equity owners have to be braced for the possibility of a zero return.

Due to the liquidity crunch, Argentex needs “an initial bridging loan in addition to further ongoing liquidity support over the near term”.

They again refer to “creditors and other stakeholders”:

The Board cautions that there can be no certainty that the Bridging Loan will be finalised and made available to the Company. In the event that such Bridging Loan is not agreed, then the Board will take immediate steps to protect value in the business for the Company's creditors and other stakeholders.

Graham’s view

This is almost the worst possible outcome for shareholders.

The need for “an immediate cash injection” rules out buyers who might be unwilling or unable to offer this, even if they valued the existing equity higher than other buyers.

And the time-sensitive nature of the situation undermines Argentex’s ability to negotiate an attractive deal for shareholders. Given that there are creditors and other important stakeholders who have an interest in the outcome (e.g. employees, HMRC), the outcome for shareholders becomes relatively less important in this situation.

Therefore, I do not expect that IFX will feel obliged to offer very much at all for Argentex’s existing equity.

And if the deal can’t be pushed through quickly enough, then the existing equity should be presumed worthless in my view.

I’m very sorry for anyone who was holding this over the Easter weekend - they have been very badly let down by management.

1pm update: the drama continued this morning with Lumon Acquisitions, the Pollen Street Vehicle, stating that they remain prepared to make a cash offer for Argentex which will include a bridging loan and liquidity support. They urge the Argentex board to resume working with them to make this happen. Let's hope that the competition between IFX and Pollen can result in a safe outcome for all stakeholders and perhaps a slightly higher bid for the equity!

System1 (LON:SYS1)

Down 14% to 458p (£58m) - Trading Statement - Graham - AMBER/GREEN

System1, the marketing decision-making platform www.system1group.com today issues an update on trading for the quarter ("Q4") and financial year ended 31 March 2025 ("FY25").

Total revenue is up 25% for FY25, thanks to strong growth of 39% in “Platform Revenue” to £34.6m.

“Non-platform” revenue falls 45% to £2.9m.

The US growth strategy appears to be working with 49% US growth.

Profitability: full-year adj. EBITDA rises strongly to £6.5m (previous year: £4.4m).

Adjusted PBT isn’t too far behind at £5.2m (previous year: £3.1m).

The adjustments are of no concern this year as actual PBT comes in higher than adjusted PBT at £5.3m. Adjustments were zero last year as well - a sign of nice and clean accounts.

Net cash finished the year at £12.9m.

Outlook

Despite the excellent full-year results, there are indications of a possible growth slowdown incoming.

I note that for Q4, the year-on-year revenue growth rate was only 2% as there was a tough comparative quarter in the previous financial year.

In the outlook statement, the company says:

While it is too early for us to gauge the effect that the current volatility in global markets will have on our clients' budgets, inevitably at this stage there is more downside than upside risk and we will provide a further update in our full year results. While we remain focused on continuing the profitable growth momentum in the business, replicating 40%+ platform revenue growth may be challenging in the current global economic and political climate, however we do anticipate continuing to deliver strong revenue growth. We strongly believe that with 25 years of advertising and innovation experience, and a methodology rooted in behavioural science, System1 is well placed to achieve our long-term goals by enabling the world's largest brands to create with confidence.

Estimates

Thanks to Canaccord for posting an update on their client today.

I note that the revenue result posted today was slightly (1.5%) below their estimate, although thanks to increased automation and higher margins, profits were slightly ahead of their estimates.

For FY March 2026, the current financial year, Canaccord are forecasting sales of £45.1m (+20%) and adj. PBT of £5.9m (+13%). These are the same upgraded forecasts that they published in January.

Graham’s view

The shares are lower by 25% since I covered them in January. Since then, the US economy has become significantly more uncertain and today’s update confirms that we need to lower our growth expectations for the year ahead, and brace ourselves for a period of uncertainty.

In that context, Canaccord’s forecasts appear vulnerable to me although clearly the company has acquiesced in allowing them to be republished.

This Stock is categorised as a High Flyer which is a winning style - high quality and high momentum, although with perhaps limited value on offer. Valuation is something I’ve worried about a lot here, but I’ve been willing to stay positive thanks to the company’s impressive stream of new business wins. Hundreds of new clients have signed up for System1’s ad-testing, idea-testing and brand-testing services in a short period of time, many of them being successful US-based businesses.

On balance, I am going to downgrade my stance on this just one notch, to AMBER/GREEN, to reflect the fact that this is a High Flyer where growth in the current year is uncertain and is likely to be much lower than the prior year. I remain very impressed by their recent sales achievements, but I also need to acknowledge that the outlook is perhaps less rosy in the short-term than it was before.

One nice bonus is the cash balance, covering more than 20% of the market cap at the current share price and reducing the effective P/E ratio. At the latest share price, I think the cash-adjusted forward P/E ratio is only about 11.5x. So after the recent falls, valuation is much less of a concern for me than it was previously.

That being said, there is a high risk that the company fails to hit this year’s forecasts, which will nudge up that forward P/E ratio.

Megan's Section

Ab Dynamics (LON:ABDP)

Unchanged at 1710p (£393m) - Half year results - Megan - AMBER

Investors who have sent shares in vehicle testing company AB Dynamics down in the midst of the Trump tariff saga have probably had good reason. The company generates two thirds of its revenue in Asia and North America, with both the US and China key markets within those regions.

But it’s also fair enough that management currently isn’t sure how badly the tariffs will impact business going forwards, such is the pace of change in the trade war:

The Group's direct exposure to the most significant increases in tariffs announced to date is likely to be limited but the more general inflationary impacts of increasing global tariffs and possible indirect effects will be kept under review and mitigated where possible through price increases

The good news is that the long-term outlook is positive regardless of what is happening in the wider macro environment. And demand for vehicle testing services remains high, especially with the adoption of electric vehicles and development of autonomous vehicles.

As manufacturers invest heavily in research and development to stay ahead of the competition, they need the likes of AB Dynamics to test their new products, which is why the long-term outlook remains optimistic.

The regulatory environment is also increasingly positive, with greater need for tighter road safety as autonomous vehicles begin development. Management says that this regulatory environment has caused an increase in demand for the testing products division (where the company sells testing robots and simulation machines) which is the biggest contributor to sales. In the first half, revenue rose 7% to £37.5m, equivalent to 65% of the company’s total sales.

The much smaller testing services division is expected to benefit from a new ruling from US regulatory body NHTSA. The ruling will require all light vehicles to be equipped with automatic braking with pedestrian detection from 2029 and was pushed through by the new administration, which tempered some fears that Donald Trump and his team might be a bit more relaxed about vehicle safety.

Improving financial strength

In the last five years, the fundamentals of AB Dynamics have suffered with the combined impacts of uncertain markets and questionable management.

Prior to the departure of the company’s founder Tony Best, AB Dynamics was a lean operation which generated significant cash for reinvestment in organic growth. Since 2019, the company has spent significant volumes of cash on external acquisitions, which haven’t always been integrated efficiently. Operating margins have taken a significant knock, averaging less than 10% in the last four years, compared to almost 20% in the years before that.

And in that time, as shares have stumbled, the senior management team have been busy patting themselves on the back (and filling their pockets) for a job well done. In 2024, chief executive James Routh took a £433k bonus, which took his total pay packet up to 16 times that of the average employee at the company. Both he and the group CFO have been selling the shares rewarded in the incentive scheme of late and own less than 0.5% of the company between them.

But in these interim numbers, there are signs of improvement. Adjusted operating margins are back up to 18.6%, driven by rising sales and operating leverage. On a statutory basis (when the £4.1m of amortisation and acquisition-related adjustments are included) operating margins were 11.6%. Not as strong as the historical norm, but still heading in the right direction.

The company remains debt free with a significant chunk of cash on the balance sheet, which will hopefully be deployed into organic growth and capital expenditure, rather than over-ambitious acquisitions which bulk up the top line, but leave profits in tatters.

Megan’s view:

AB Dynamics is one that I struggle to ‘get over’. It’s a wonderful business in an exciting market, but it hasn’t been well managed and that has cost shareholders in the last few years. It’s not a good sign that many of the larger shareholders have been selling recently, including the company’s founder who sold just shy of £4.5m worth of shares in September. (To caveat, Mr Best still has a 24% stake and is 88 years old, so there could have been some pension requirements at play there).

Selling from Liontrust, Cannacord and Sandford DeLand’s Buffettology fund is less easy to explain away. Perhaps, like me, these fund managers have been disappointed by a company where the investment case (long term compounding growth and lots of cash) no longer stacks up.

But, as I say. I struggle to get over this one because it should be so much better than it is.

It’s a falling star based on Stockopedia’s rankings because the share price has been trending downwards. And it’s not that cheap based, trading on a price to forecast earnings ratio of 22x (although that’s not a bad valuation compared to the company’s history).

If those margins can keep heading in the right direction, I think I would be more tempted. But for now, I am staying neutral and will try and fight my urge to base the investment rationale on the company’s ‘good old days’. AMBER

Tesla (NSQ:TSLA)

Up 6% pre-market to $238 ($746bn) - Q1 results - Megan - RED

Tesla epitomises John Maynard Keynes’ famous advice:

Markets can remain irrational longer than you can remain solvent.

Last night the company announced financial results for the first quarter which revealed revenue from car production down a fifth and earnings per share down 71%. And yet, pre-market activity suggests the company’s shares will open up 6% today.

Why? One explanation could be that Elon Musk has promised to spend more time in his car company and less time dismantling Twitter, disrupting the US government and sending celebrities into space. Such is Musk’s celebrity, the news of his renewed focus on Tesla seems to have been taken as a positive by the market (whether employees feel the same way is a different matter).

The movement could also be a response to a shift in short interest. Tesla has substantial short interest and the shorters have had a good year as the company’s share price has plummeted. A tariff war which revolves around the automotive industry was never going to be a good thing for the company, even if its founder has the ear of the president. One Tesla short fund is up 61% in the year to date. Short sellers have reportedly made $11.5bn from the stock so far this year.

Whatever the reason for the share price movement, it makes analysis of the company’s first quarter results feel futile. This is a company which is worth more than all of the world’s car companies combined. It’s trading on over 100x forecast earnings and those earnings are not exactly reliable. There is no fundamental investment case to be made here.

There was a time when Tesla led the way in the electric vehicle market. And when promises like ‘Teslas will be able to drive themselves across America soon’ could just about be believed. Now the rest of the global automotive market is catching up. In 2024, Chinese company BYD was the most popular brand of electric vehicle, selling more total units than Tesla. In Europe, the range of models from Volkswagen, Audi, Skoda and Volvo have encroached on Tesla’s potential market share. Even in the US, there are now competitors.

Tesla says that the decline in car sales is largely the result of updates made to the hugely popular Model Y, which were disrupted in production. But the company has also reported a decline in average selling price, which suggests competition is having more of a negative impact than Musk would like to admit.

Megan’s view

This is a company whose entire valuation seems to be based on the promise of things to come. While enigmatic management can keep making those promises, there will clearly be investors who keep believing them. And there are times when there is money to be made in the madness, both long and short.

But I have no idea how to monitor those times or understand what on earth makes this such an expensive stock. So I am staying well clear. RED

Roland's Section

Hollywood Bowl (LON:BOWL)

Up 3.5% to 276p (£466m) - Half-Year Trading Update - Roland - AMBER/GREEN

Hollywood Bowl Group, operator of the UK's and Canada's largest ten-pin bowling brands, is pleased to announce a trading update for the six months ended 31 March 2025.

Today’s update from this bowling operator looks fairly positive to me. The company’s expansion into Canada appears to be progressing well and may address any concerns over UK market saturation.

Headline numbers highlight the strong contrast between the two markets:

Group revenue +8.4% to £129.2m

UK revenue +4.7% to £108.2m

Canada revenue +40.8% to £21.1m (at constant FX)

UK: the picture here is relatively straightforward. Like-for-like revenue rose by 1.3%, with the remaining increase coming from three new centres. This takes the total UK estate to 75.

This is an improved LFL performance from FY24, when UK LFL was flat, but it should probably be seen against a backdrop of cost inflation.

The company says this year’s National Insurance rise will add £1.2m in costs (i.e. 1.1% of UK revenue), which it’s “well positioned to mitigate”. However, all else being equal, this suggests to me that BOWL could do well to maintain flat margins in the UK.

Four refurbishments were completed in H1. Two new centres + one refurb are on track to open in H2.

Canada: Hollywood Bowl’s expansion into Canada started in May 2022, when the company acquired Splitsville (5 bowling centres plus Striker Bowling Solutions, an equipment supplier).

The estate has now reached 15 centres, with 2 new centres and two refurbs opened during H1.

In H2, a further four refurbs are due to complete, while another new centre is due to open in H1 FY26.

Two like-for-like growth figures are provided for Canada:

Total LFL +13.6%

Bowling centre LFL +3.7%

If I’ve understood this correctly, these figures suggest that Striker may have achieved 10% LFL sales growth in H1. Given that Striker’s FY24 revenue was £4.5m, this seems a plausible assumption to me, given its position as a key supplier for the group’s new centres and refurbishment projects.

The company has previously commented on the benefits of owning a key supplier – it seems vertical integration is coming back into fashion!

However, the Bowling Centre LFL growth of 3.7% is below the figure of 5.9% achieved last year, even after adjusting for the timing of Easter and an extra trading day in FY24.

I had wondered if the application of BOWL’s operating model might support a higher initial rate of growth in its Canadian centres, but if so, this effect seems relatively small.

Outlook: trading in H1 is said to have been strong and included a record revenue month in both the UK and Canada.

New and refurbished centres are said to be performing well and delivering target returns.

The company notes that 70% of revenue is “not subject to cost-of-goods inflation” and believes tariffs will have no material impact.

Full year guidance is unchanged:

The Group remains confident in the outlook for the business in FY2025

Roland’s view

I haven’t looked at Hollywood Bowl for a while now, but I don’t see too much to dislike.

Management say the group remains on track to have a total of 130 centres by 2035, which would imply a further 44% expansion of the portfolio.

My main concern would be the risk of margin pressure, due to the combination of weak LFL growth and possible cost inflation. Today’s update does not tell us much about profitability, but the company’s commentary on costs does seem broadly encouraging.

The StockRanks currently have a neutral view on this stock:

However, I wonder if the half-year results (due on 29 May) could lead to a more positive rating.

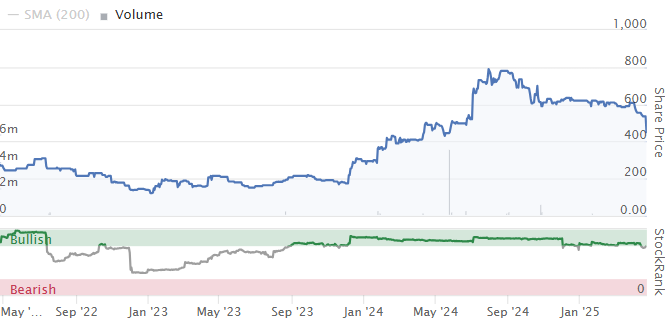

Over the last year, the shares have fallen by more than 15%:

But over the same period, earnings estimates have fallen by less than 3%:

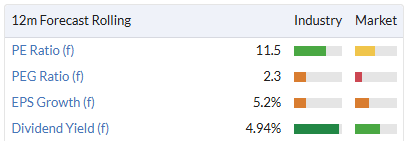

The resulting de-rating of the stock has left BOWL shares on a rolling forward P/E of 11.45, with a dividend yield of nearly 5%:

I think that could potentially be attractive if the group can maintain its steady growth and decent quality metrics:

On balance, I’m going to take a moderately positive stance here today, at AMBER/GREEN. We will check back in May to see if the half-year results justify my optimism.

Supreme (LON:SUP)

Down 7% to 158p (£185m) - Trading Update - Roland - AMBER/GREEN

FY25 results are to be in line with market expectatios, with revenue of £235m and adj EBITDA of “at least” £40m. Net cash at year end.

Zeus has FY25E EPS at 21.2p.

Outlook for FY26 is also in line with expectations.

Zeus has FY26E EPS at 19.4p, implying a c. 8% fall vs FY25.

Roland's View

The market seems disappointed by today’s update, perhaps because today’s unchanged guidance implies an earnings fall in FY26.

Recent acquisitions Clearly Drinks and Typhoo Tea are both said to be performing well.

The big unknown is over how vape sales will change following the introduction of a ban on disposables on 1 June 25. Today’s update states that vape sales remain “in line with internal estimates”, but this isn’t very helpful.

Supreme has invested in rechargeable pod systems and has good distribution reach in the UK retail sector. My feeling is that the company could adapt to this change somewhat successfully, although I don’t see any easy way to predict the near-term impact on sales and margins.

Given SUP’s reasonable valuation and decent track record, I’m going to maintain our moderately positive view.

See what our investor community has to say

Enjoying the free article? Unlock access to all subscriber comments and dive deeper into discussions from our experienced community of private investors. Don't miss out on valuable insights. Start your free trial today!

Start your free trialWe require a payment card to verify your account, but you can cancel anytime with a single click and won’t be charged.