Good morning - Tuesday's Agenda is now complete!

1pm: all done for now, thank you.

Companies Reporting

| Name (Mkt Cap) | RNS | Summary | Our view (Author) |

|---|---|---|---|

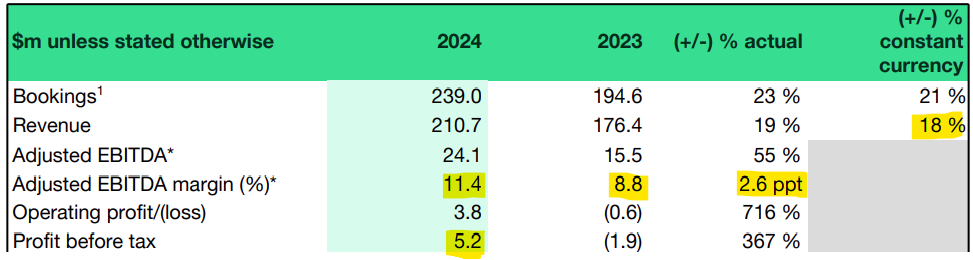

Computacenter (LON:CCC) (£2.4bn) | Full Year Results | “Solid” in context of a challenging IT market. Dec 2024 order backlog significantly ahead of Dec 2023. | AMBER/GREEN (Roland holds) After a weak H1 24, CCC delivered a record H2 and has strong momentum heading into 2025. 2024 results show a 24% ROCE but uncharacteristic drop in profits. Earnings expectations are said to be positive for 2025, but have already been downgraded several times. Without visibility on updated estimates, I’ve moderated my view slightly to reflect the 20% share price rise since January. |

Trustpilot (LON:TRST) (£1.1bn) | Full Year Results | 2024: rev +18%. 2025: expecting high teens growth, adj. EBITDA slightly ahead of market expectations. | AMBER/GREEN (Graham) |

Bytes Technology (LON:BYIT) (£999m) | FY TU | SP +19% | AMBER/GREEN (Graham) [no section below] This is a fabulous update with a confident outlook statement. |

Harworth (LON:HWG) (£541m) | Full Year Results | Official net value per share +8% to 222.3p vs. 165p SP. Outlook: “Well placed to navigate uncertainty”. | |

Close Brothers (LON:CBG) (£520m) | Interim Results | H1 op loss £103m, adj. op profit £75m. Will review dividends after clarity on FCA/Supreme Court. | |

Boku (LON:BOKU) (£465m) | Full Year Results | Revenue +24% at constant FX. Expects >20% rev growth in FY25, significantly exceeding exps. | |

Mortgage Advice Bureau (Holdings) (LON:MAB1) (£441m) | Full Year Results | Revenues +11%, adjusted PBT +38% (£32m). Continuing to gain market share. Mortgage affordability is set to improve in 2025, and the year has begun strongly and in line with expectations. They continue to evaluate a move from AIM to the Main Market. | GREEN (Graham) [no section below] I've been impressed by MAB1 for quite some time. Today I'm impressed to learn that 40% of applications come from customers who've transacted with them before. A new "Mortgage Monitoring" tool has been rolled out across the network, sending alerts to customers when a new mortgage deal would be beneficial. This should help MAB1 keep a grip on the important refinancing segment this year, as high volumes of mortgages are forecast to mature. Overall, 2025 should be a better year for mortgages with lower inflation and lower mortgage rates boosting both confidence and affordability. MAB1's recently-announced medium-term targets suggest an aggressive growth agenda is on the cards for them. I continue to view these shares as offering an attractive mix of both quality and potential growth. |

SThree (LON:STEM) (£341m) | FY25 Q1 TU | Q1 net fees down 15%. Ongoing challenging conditions. FY25 to be in line with guidance (£25m PBT). | |

Sabre Insurance (LON:SBRE) (£310m) | Full Year Results | Gross written premium +5%. PBT doubles to £48.6m. Dividend increased plus £5m buyback. | |

Fintel (LON:FNTL) (£268m) | Full Year Results | FY24 rev +21%, adj EPS +8.2%. Mkt opportunity strong, housing improving. YTD trading in line. | |

Yu (LON:YU.). (£244m) | Full Year Results | Rev +40%, PBT +12%. Meter points +65%, overdue days reduced. “Strong start” to 2025. | GREEN (Roland holds) This small-cap utility maintained strong underlying growth last year, almost doubling its market share. Although margins have weakened, 40%+ return on equity (and net cash) suggest to me that the business continues to generate attractive returns. On a forward P/E of 7, I think Yu looks reasonably priced, with further growth potential. |

Midwich (LON:MIDW) (£237m) | Full Year Results | Rev +3.5% at constant FX. Adj PBT -22%. “Challenging macro”. Outlook unch, but H2 weighting. | |

Fonix (LON:FNX) (£190m) | Interim Results | Gross profit +6.5% to £9.8m, adj PBT +5.4% to £7.8m. Solid contract renewals. Outlook in line. | |

H & T (LON:HAT) (£164m) | Full Year Results | Strong H2, FY24 in line with exps. PBT +10% to £29.1m, pledge book +26%. YTD trading in line. | GREEN (Graham) 26% growth in the pawnbroking pledge book should feed through to significantly higher revenues in the current year. At a PER of 7x I still think this offers excellent value for a market leader. |

Zotefoams (LON:ZTF) (£128m) | Full Year Results | Rev +16% to £148m, adj PBT +19% to £15.3m. 2025: “+ve start”, targeting 18% op margin by FY29. | GREEN (Roland) Today’s results show strong growth driven in 2024, albeit aided by the Olympics. Profitability is on track to improve as expected from 2025 and the company’s plan to focus on broadening its core offer makes sense to me. On a P/E of 9, the shares look good value to me. |

Litigation Capital Management (LON:LIT) (£72m) | Interim Results | Net realised gains $37.4m at 3.67x MOIC. Income $4.7m due to $32m -ve fair value movt. NAV 86.3p. | |

Pebble (LON:PEBB) (£68m) | Full Year Results | FY24 results in line with exps. Rev +1% to £125m, PBT +9.5% to £8.1m. Possible tariff concerns. | |

OptiBiotix Health (LON:OPTI) (£17m) | Commercial Update | £1m orders in 2024 (+56%). Stock overhang cleared in Aus. Gross margin and revenue exp to improve in 2025. | |

Light Science Technologies Holdings (LON:LST) (£9m) | Full Year Results | Rev +29.5% to £12m, net profit in H2. FY trading close to breakeven with net loss of £30k. | |

Newmark Security (LON:NWT) (£7m) | TU | Revenue higher in H2 25, on track to exceed last year’s FY revenue. Sales activity in N Am “exciting”. |

Graham's Section

H & T (LON:HAT)

Up 5% to 396.8p (£175m) - Preliminary Results - Graham - GREEN

We already looked at the full-year trading update from H&T in January.

Today’s results confirm that trading in the current financial year is in line with management expectations.

I like this simple summary provided near the top of today’s announcement:

H&T is the largest pawnbroker in the UK and continues to grow its market share. There are limited alternatives for individuals who need to borrow small sums of money for a short term, and the pawnbroking service offered by H&T is a simple and transparent way to do so. In addition, the Company is seeing more business owners using its service for working capital purposes, which is reflected in an increase in the number of larger loans granted.

Some of the main highlights that stand out to me for 2024 are:

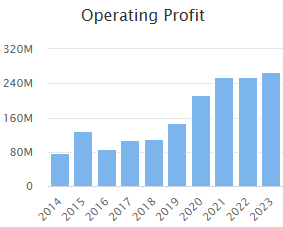

PBT +10% to £29.1m

Pawnbroking pledge book +26% to £127m which is not yet reflected in revenue.

Retail sales of jewellery and watches +27% year-on-year, and gross profit from this +34% to £19.3m.

Net debt rises from £32m to £54m. I tend to think of it as a very good thing when H&T borrows to fund its pawnbroking activities, as this means profits will rise in future years.

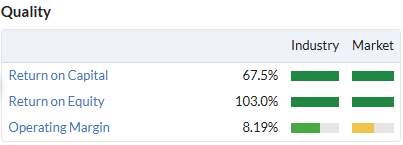

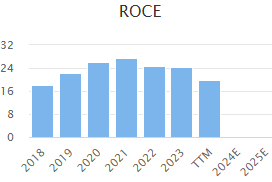

Post tax return on equity is calculated by the company at 12.2%, down slightly year-on-year. I’m not convinced that H&T qualifies as a “quality compounder” but it’s great that they have maintained attractive returns for another year. They work on the basis of a target ROE in the mid-teens.

Dividend increases to 18p for the year, for a trailing yield of 4.5% (forecast yield is 5%).

Outlook: demand to remain strong given macro conditions, and another 50 stores to be refreshed this year out of a total network of 285 stores. The overall size of the estate is growing at a reassuringly slow pace.

CEO comment:

Demand for our core pawnbroking product continues to grow, with particularly strong lending demand in the final ten weeks of the year, providing a sound base for future growth.

This is a stock I held for many years previously as a top holding, and I’m open to the possibility of owning it again some day.

The right thing to do would have been to pick it up at 340p a few months ago. It’s already approaching 400p again:

This stock offers a nice mix of diversification (between pawnbroking, retail, FX and gold purchasing) but also the comfort of knowing that it’s a market leader when it comes to the main event, which is pawnbroking.

I slept soundly owning this one. Pawnbroking is an ancient activity and one that offers many benefits to customers - the main benefits being that no credit check is required to use it, and also that “defaulting” on this type of loan has no repercussions for a person’s credit score.

It doesn’t trap people in debt long-term, as the pawned item can simply be sold off by H&T to clear it.

Regulators understand this and have left pawnbrokers alone even as alternative products such as payday loans have been crushed by regulations.

As H&T itself says, “there are limited alternatives” for those wishing to borrow small amounts for a short period.

So in summary, I see H&T as the undisputed market leader (ten times bigger than Ramsdens Holdings (LON:RFX) when it comes to pawnbroking), in a financial sub-sector where competition has been stifled by regulations, and with the ongoing macro tailwind of high consumer demand for short-term credit.

The increase in national insurance contributions will hit everyone but H&T will be well-equipped to face this challenge. The additional £2m of costs will be mitigated where possible but at the end of the day it is less than 10% of PBT.

One important thing to watch out for, and it’s something we have mentioned before, is that the financial year-end is changing to September. I never like to see this but I accept the company’s statement that it will help from the point of view of increased seasonality in the business.

To demonstrate the increased seasonality, I calculate that only 45.5% of H&T’s revenue was generated in H1 in these results, vs. 48.5% in H1 the previous year.

Estimates: thanks to Canaccord for publishing a note this morning. They’ve brought in adj. PBT estimates for FY Sep 2025 and FY Sep 2026 that match their previous forecasts for FY Dec 2025 and FY Dec 2026.

Graham’s view

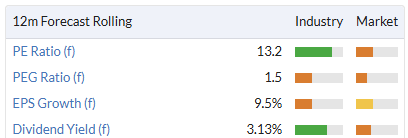

At a PER of 7x, I can stay positive on this.

The StockRanks consider it be a Super Stock:

One risk to bear in mind is the gold price, as it underpins the security of many of H&T's loans. Gold has been making new all-time highs for months; a sharp reversal could test H&T's risk management policies.

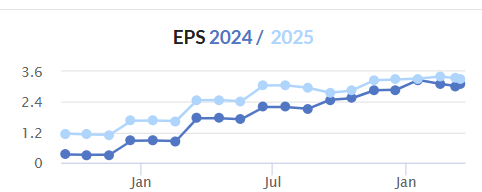

Trustpilot (LON:TRST)

Up 11% to 307.5p (£1.27bn / $1.65 billion) - Full Year Results - Graham - AMBER/GREEN

If you like earnings momentum, then look no further:

In January, we learned that 2024 results would beat expectations.

Today, we learn that the company now expects 2025 adj. EBITDA to be slightly ahead of market expectations.

They also provide us a nice succinct explanation of what they are and the investment thesis:

Trustpilot is an open, trusted customer feedback platform. We monetise as a high margin SaaS business with network effects and have a significant market opportunity

In 2024 they generated 18% underlying revenue growth, achieved an increase in the adj. EBITDA margin, and they turned the corner to positive PBT:

CEO comment:

Our strategy is clear: we operate an open, trusted platform for consumers to help each other make the right choices, and for businesses to build trust, grow, and improve. We maximise the platform’s inherent network effects by concentrating on depth in focus markets and verticals; and we drive a SaaS model with positive net dollar retention, underpinned by product innovation.

Geographically, I note that North America is the fastest growing market with 26% bookings growth and with over a fifth of the company’s total bookings in 2024. If they can "win" in the United States, surely that must augur well for winning on a global scale!

Some other key metrics:

Annual recurring revenue +21% to $231m (it is typical to value SaaS businesses using ARR multiples)

Net dollar retention rate improves to 103% (anything over 100% means that existing customers are spending more).

Number of active reviews +23%

On profitability, we are still at a very early stage in the company’s development, but we do now have positive profitability on a statutory basis (this was achieved in the prior year only through tax credits).

Buyback: the company continues to plough its adj. EBITDA and surplus cash into buybacks with a further $20m announced today. It can afford to do this as it maintains a cash-rich balance sheet with $69m as of Dec 2024.

CEO comment:

We delivered a strong performance in 2024, with upgrades to adjusted EBITDA* expectations across the year, demonstrating operating leverage. Following a year of record bookings growth, we expect high teens percent constant currency revenue growth in 2025, with adjusted EBITDA* slightly ahead of market expectations and a 2ppt improvement in adjusted EBITDA margin*. We remain confident in delivering sustainable growth and operating leverage over the long term given the significant market opportunity.

Graham’s view

This is one of the stocks I’m most excited about in terms of its competitive position: it’s not clear to me that it has any meaningful competition. This leaves it free to build up its network effects (the more people who use it, the more valuable it becomes) and its brand recognition, with the potential to create an extremely valuable business.

If that’s true, then maybe this is one of those rare cases when I need to put valuation concerns to one side.

In January, I looked at the price to sales multiple (trailing). This is 7.8x.

Calculating a multiple of recurring revenue, I get c. 7x.

Adjusting for the cash balance doesn’t make much of a difference.

Perhaps it is worth an upgrade back to GREEN but at this multiple I’m more comfortable with AMBER/GREEN.

We have just seen it produce high teens revenue growth for 2024, and it predicts that it will do the same again in the current year.

That’s not bad at all, but it’s not such a rapid pace of growth that I have to drop my valuation concerns entirely.

Therefore, I’ll keep a cool head and a moderately positive stance on Trustpilot.

Expect more volatility in both directions as the market struggles to put a sensible value on this:

Roland's Section

Zotefoams (LON:ZTF)

Up 3% to 270p (£132m) - Preliminary Results - Roland - GREEN

"Record revenue and profitability form a firm foundation for our next growth phase"

Today’s results from this “world leader in supercritical foams” have received a positive reception from the market – and with some justification, in my view, given Zotefoams’ depressed share price:

2024 results summary: Zotefoams’ financial performance last year isn’t the whole story here, but it’s a reassuring starting point.

The company saw sales of its high-performance product (e.g. foam used in consumer goods) outperform those of its Polyolefin Foams (industrial markets) for the first time. This is said to reflect an improvement in mix.

More objectively, I think it’s fair to say that last year’s results reflect a surge in demand for sports footwear during an Olympic year, paired with weaker industrial demand.

The headline numbers are certainly quite strong:

Revenue up 16% to £147.8m

Adjusted pre-tax profit up 19% to £15.3m

Reported pre-tax profit down 99% to £0.2m

Earnings before exceptionals up 37% to 25.95p

Dividend up 4% to 5.1p per share

Net debt excluding leases down 20% to £24.1m

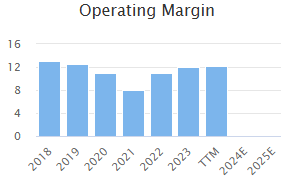

Strategy update: Exceptional costs were significant, but I’m more sympathetic towards these than I usually would be as they are demonstrably a one off.

A £15.2m charge reflects the impairment and closure of the MEL (ReZorce) business, which has now been paused. This decision will result in a £4.9m reduction in operating costs that should boost future profit margins (I discussed this in more detail recently here).

Today’s results and broker commentary confirm estimate that the removal of the MEL costs gives Zotefoams a pro forma operating margin of c.15%, significantly above the 12% adjusted margin generated in 2024 and prior years:

Instead of pursuing an expensive and uncertain commercialisation of ReZorce, CEO Ronan Cox is doubling down on the group’s core business and investing in new facilities to capture growth and enable the company to offer more valued-added solutions to its customers.

Through increased focus on the customer, continued commitment to innovation, expanding capability to move up the value chain and enhanced organisational execution, the Group is targeting ambitious progress in the medium term

Part of this process involves a £26m investment in new facilities in Asia, which Graham covered here earlier in the month.

As a result, the company is targeting a significant further improvement in scale and profitability by 2029:

Organic revenue growth of 7% CAGR to >£200m

Operating margin of over 18%

ROCE of over 20%

Cash conversion of >95%

An operating margin of 18% on £200m revenue would give an operating profit of £36m – twice last year’s adjusted figure of £18m. I think it’s reasonable to assume this business could be worth a lot more in four years, if Cox can hit these targets.

Outlook & Estimates: management report “a positive start to 2025”, especially in its Consumer & Lifestyle (footwear) and Transport & Smart Technology verticals. Industrial demand remains more subdued but is expected to improve later this year.

The company warns of macro uncertainty, but says its manufacturing footprint across the UK, USA, Poland and (soon) Vietnam should help it to navigate and adapt to changing trade patterns.

Sales growth is expected to be more modest in 2025, with revenue up just 1.5% to c.£150m. However, the improvement in margins mentioned above is expected to drive a more significant increase in earnings.

Broker Shore Capital has provided an updated note today confirming that its forecasts for 2025 and 2026 are unchanged:

2025E EPS: 30.6p

2026E EPS: 34.4p

Shore’s 2025 EPS estimate is equivalent to a 20% rise in adjusted earnings this year – highlighting the benefits of the margin boost from shutting down ReZorce.

Roland’s view

These forecasts leave Zotefoams trading on a 2025 forward P/E of 9, with a useful c.3% dividend yield.

Said differently, the shares are trading close to their net asset value:

That looks cheap to me for a business with double-digit ROCE, valuable intellectual property and improving margins.

One caveat to this is that the business is still heavily dependent on demand from its largest customer, Nike. Customer concentration isn’t mentioned in today’s results, but Nike represented 36% of group sales in 2023.

This risk probably merits some valuation discount, in my view. Even so, I’m very comfortable maintaining our GREEN view based on today’s results.

Yu (LON:YU.).

Up 0.7% to 1,460p (£245m) - Final Results - Roland - GREEN

At the time of publication, Roland holds a long position in YU.

This business energy supplier is a member of both Ed’s 2025 NAPS portfolio and my Stock in Focus portfolio. So we have a strong interest in the progress of this founder-led business here at Stocko!

Fortunately, the narrative seems to remain positive today:

The Group reports another year of increased revenue, Adjusted EBITDA, earnings per share, cash generation and forward contracted customer book. The Board reiterates its commitment to continued organic growth delivering sustainable profitability growth as it takes advantage of the significant market opportunity available.

Let’s take a look at the numbers.

2024 results summary: Yu’s revenue is heavily influenced by energy prices, so I think profit is a more useful measure of growth than the top line gain here:

Revenue up 40% to £645.5m

Pre-tax profit up 12% to £44.5m

Operating margin of 6.4% (2023: 8.3%)

Earnings per share up 8.1% to 200p

Dividend up 50% to 60p per share

Net cash of £80.2m (2023: £32.1m)

Overdue customer receivable: 3 days’ sales (2023: 4 days’ sales)

The decrease in operating margin last year reflects a couple of factors:

An 29% increase in operating costs to “drive growth and/or margin improvement”

A reduction in gross margin to 14.5% (2023: 18.1%). The company says this was due to a higher proportion of non-contracted customers in 2023 – presumably these pay higher prices but provide less visibility than contracted customers.

It’s also worth pointing out that the c.£50m increase in net cash last year was primarily the result of a one-off return of collateral previously required for hedging. My sums suggest free cash flow was just £11.4m last year, due to adverse working capital movements and capex.

I don’t see a problem with the balance sheet but I do think it’s worth remembering that working capital movements can be large and frequent during the year. I tend to view the group’s cash position as an important source of liquidity, rather than as surplus to requirements.

Trading commentary: Yu provides some useful operating metrics to illustrate the progress of its business. In my view, growth in meter points and energy supplied highlight strong underlying growth here:

Meter points supplied up 65% to 88k

Equivalent volume of energy supplied up 78% to 2.21 TWh

Market share up 1.3% to 2.7% - almost double vs 2023

Average monthly bookings down 23% to 42.6

Many customers are on fixed-rate contracts, which Yu is able to secure through its commodity trading agreement with Shell. These provide good visibility on future revenue:

Contracted revenue for FY25 up 9% to £566m

Total contracted revenue up 25% to £1,034m

The company’s smart meter rollout is also gathering pace and is being funded with a secured debt facility, to preserve the group’s cash. Smart meters remain a small component of revenue, but can hopefully be scaled up:

2024 installations up 14.4% to 22.9k

Index-linked annualised recurring revenue up £1.1m to £1.3m

Outlook: Yu’s CEO Bobby Kalar strikes a positive tone and says trading has started well this year:

Strong start to 2025, with new record monthly revenue, cash collection and cash balance metrics achieved in January.

Guidance: Revenue for the year is expected to be £730m to £760m. Earnings and closing net cash are expected to be in line with current market expectations.

Estimates: Broker Panmure Liberum has provided updated forecasts today - many thanks. Their numbers are indeed almost unchanged:

2025E EPS: 213.6p (previously 213.1p)

2026E EPS: 228.1p (previously 231.8p)

Roland’s view

Yu’s falling profit margins are a negative trend I hope to see stabilise in 2025. But the group’s profitability remains impressive at a balance sheet level.

My sums suggest a return on equity of 48% and return on capital employed of 52%.

Both are lower than previously, but perhaps this is to be expected as the group expands:

On balance, I don’t see anything in today’s result to alter the positive narrative here. With Yu shares trading on a forward P/E of 7 and offering a useful 4% dividend yield, I think the valuation remains attractive too.

The StockRanks were very positive ahead of today and I think the outlook remains strong. GREEN.

Computacenter (LON:CCC)

Up 12% to 2,616p (£2.8bn) - 2024 Final Results - Roland - AMBER/GREEN

At the time of publication, Roland holds a long position in CCC.

This IT value-added reseller specialises in large enterprise and public sector clients. It’s a long-term holding of mine.

Today’s results do not contain many surprises, following January’s reassuring trading update, but the numbers appear to have pleased the market all the same:

2024 results summary: last year’s numbers are somewhat mixed and not especially good, by CCC’s standards.

Revenue up 2.9% to £6,965m in constant currency

Operating profit down 11.5% to £237.9m

Adjusted earnings down 8.5% to 159.9p

Dividend up 1% to 70.7p

Adjusted net cash up 5.1% to £482.2m

Last year’s operating margin of 3.4% was slightly lower than the 3.8% reported in 2023. By nature this is a low margin business, but strong financial management (and supplier credit) support very attractive returns on capital. My sums suggest a ROCE figure of 24.8% for 2024, in line with recent years:

Unfortunately, last year’s drop in operating profit does break a long run of growth:

However, these full-year numbers mask a tale of two halves – a weak H1 followed by a much stronger H2:

Encouragingly, the second half was the most profitable in our history and was derived from our highest number of major customers

This progress is expected to continue in 2025, supported by a strong year-end order book:

We exited 2024 in a robust position with a committed product order backlog which is significantly ahead of our position in December 2023, as well as at the end of June 2024, with all regions ahead. The size of the projects we are currently delivering gives us good momentum at the start of 2025.

Outlook: Despite macro uncertainty, the US – where CCC serves hyperscalers and some other large customers – continues to offer growth potential:

Looking to 2025 as a whole, we remain mindful of the uncertain macroeconomic and political environment. In North America, following a strong performance in 2024, we continue to be excited by the growth opportunities we see ahead.

However, earnings guidance is limited to a statement that “we expect to make progress in FY 2025”.

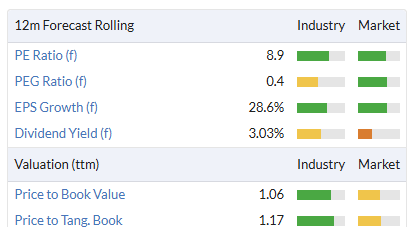

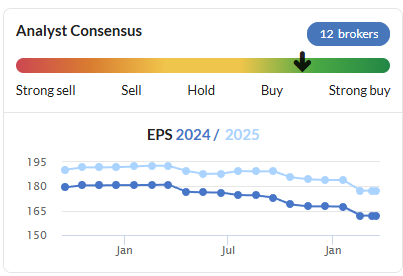

Unfortunately, I don’t have access to broker notes for Computacenter. Consensus forecasts on Stockopedia prior to today suggest earnings could rise by c.10% to 177p per share for 2025, putting the stock on a P/E of 13.

Roland’s view

While I continue to believe the shares offer good value and positive long-term prospects, the reality is that profits fell sharply in 2024 and the earnings outlook for 2025 has deteriorated over the last year. There have been several broker downgrades, most recently last month:

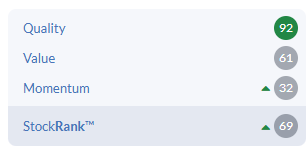

This trajectory is reflected in the stock’s contrarian styling, with strong quality and value but weak momentum:

Without access to broker forecasts, it’s not clear to me whether 2025 and 2026 forecasts will be maintained or changed following today’s results.

In the meantime, it’s worth noting that the share price has risen by c.20% since January. Depending on forward expectations, the shares may not be as compellingly cheap as they were in January (in my opinion).

As a result of these factors, I’m going to moderate my view from GREEN to AMBER/GREEN, while acknowledging this may be too cautious.

See what our investor community has to say

Enjoying the free article? Unlock access to all subscriber comments and dive deeper into discussions from our experienced community of private investors. Don't miss out on valuable insights. Start your free trial today!

Start your free trialWe require a payment card to verify your account, but you can cancel anytime with a single click and won’t be charged.