Good morning! The FTSE finished up 2% yesterday and got back within the range where it spent most of last year:

The Aim All-Share Index remains in a state of total depression:

I've reached a point now in my own thinking where I don't know if the Aim Index is useful as a benchmark for anything - its performance has been that poor over the long-term! I'd rather use one of the FTSE Indexes instead.

1.10pm: we've run out of time for now - a remarkably busy day for announcements! Cheers.

Companies Reporting

| Name (Mkt Cap) | RNS | Summary | Our view (Author) |

|---|---|---|---|

Wise (LON:WISE) (£12.1bn) | FY25 vol +23% to £145bn, active cust +21% to 15.6m. Adj income +16% to £1.36bn. 20% PBT mgn. | ||

B&M European Value Retail SA (LON:BME) (£3.0bn) |

SP +3.5% | AMBER/RED (Roland) [no section below] I’m pleased to see there are no further downgrades after February’s profit warning. But I remain concerned by apparent weakness in the core UK business, where LFL sales fell by 3.1% last year. With operating costs up by 6% over the same period, margins must surely be under pressure? In this context, the group’s plans to maintain a high rate of store openings looks a little risky to me. With the CEO departing on 30 April, I’m going to leave my mildly negative view unchanged ahead of June’s FY results. | |

Frasers (LON:FRAS) (£2.8bn) | 25yr agreement to launch Sports Direct in Aus/NZ. Frasers will fund with £29m Accent (ASX:AX1) share purchase. | ||

Tate & Lyle (LON:TATE) (£2.4bn) | Integration of CP Kelco “on-track”, improved EBITDA margin. FY25 results exp in line with guidance. | ||

| Greatland Gold (LON:GGP) (£1.8bn) | Telfer Ore Reserve, Outlook and Havieron expansion | Telfer dual train extended through FY27 before Havieron in FY28. Exp avg 280-320koz/yr in 26/27. | |

Integrafin Holdings (LON:IHP) (£1.0bn) | Q2 25 net inflows of £1.2bn, 7.3% of opening FUD. Total FUD +8% YoY to £65.9bn. H1 group revenue is expected to rise by 9% to c.£77m. | AMBER/GREEN (Roland) [no section below] This investment platform for IFAs is a good quality business, in my view. Today’s update doesn’t change this, with evidence of further inflows and continued growth in its client base. The accounts are somewhat complex, but my previous analysis has found this to be a high-margin, cash-generative operation. Long-term margin pressure could be a key risk, but continued founder ownership is an attraction for me. The shares aren’t cheap, but I think a moderately positive view can be justified. | |

Firstgroup (LON:FGP) (£932m) | FY25 adj op profit & EPS to be ahead of previous expectations. Strong rail perf, bus in line. | ||

PRS Reit (LON:PRSR) (£609m) | Completed homes 5,443, 35 left. ERV +1.5% to £69.6m. LFL rent +10% YoY. Sale process ongoing. | PINK (formal sale process) | |

Atalaya Mining Copper SA (LON:ATYM) (£469m) | Q1 copper prod 14,291 tonnes, +18% QoQ due to higher grades. FY25 guidance unchanged. | ||

Tatton Asset Management (LON:TAM) (£352m) | FY25 net inflows £3.7bn, AUM +24% to £21.8bn. IFAs +135 to 1,100. FY25 results to be in line. | ||

Porvair (LON:PRV) (£325m) | YTD trading in line with exps. New CEO starts today. Re. macro, no change to long-term outlook. | ||

Halfords (LON:HFD) (£272m) | Strong year end, FY25 LFL sales +2.3%. Exp FY25 adj PBT at upper end of £32-37m guidance. | AMBER/GREEN (Roland) [no section below] This is the second positive update on profit this year, following January’s update. It’s good news. But Halfords still needs to mitigate a £23m increase in direct labour costs in FY26, against a difficult trading backdrop. Management expects to be able to “mitigate the entirety” of the Budget impact, but with a new CEO starting this week I will be interested to see what his views are when Halfords reports in June. However, given the seemingly improved momentum, I’ve upgraded my view by one notch today. | |

MHA Plc (MHA) (£271m) | MHA is "a leading professional services provider of audit and assurance, tax, accountancy & advisory services". It begins trading on AIM. Has raised £98m at 100p. SP up 2% so far. | AMBER (Graham) [no section below] It's nice to see any IPO these days and the fundraising amount is significant. A helpful bit of business for Nomad and broker Cavendish (LON:CAV). MHA is the 13th largest UK accountancy firm by revenue and wants to be a top 10 firm in the medium-term. This looks set to be an active M&A player in the professional services sector. Partners in the company still own 54%. | |

VP (LON:VP.). (£215m) | FY25 results to be in line with market exps. Infrastructure outlook +ve, construction mixed. | ||

Liontrust Asset Management (LON:LIO) (£213m) | Q1 net outflows £1.3bn, AUMA -8% to £22.6bn. Cost savings of £6m, intern’l expansion ongoing. | AMBER/GREEN (Graham) Although I have a strong preference for other fund manager shares, I can't downgrade this to neutral as the stock remains extremely cheap against AUM and earnings. It is expected to remain profitable even after years of heavy outflows. | |

MaxCyte (LON:MXCT) (£210m) | “Vast majority” of trading now on NASDAQ. Last day of UK trading expected to be 25 June 2025. | PINK (delisting) (Graham) [no section below] This cell engineering company has been dual-listed since July 2021 and no longer sees value in its AIM listing. As it's a US-based company and the fundraising environment on AIM is unlikely to be helpful, this makes good sense. I note that the company has been consistently very heavily loss-making for years. | |

Harmony Energy Income Trust (LON:HEIT) (£198m) | Recommended acquisition by Drax (LON:DRX) | Scheme docs for 25 March 25 cash offer of 88p per share. Vote 7 May, last day of dealing 12 June. | PINK (under offer) |

S&U (LON:SUS) (£172m) | Revenue stable, PBT down 29% (£24m). Legal & regulatory challenges “almost all resolved”. In motor finance, the company says "evolving regulatory interpretations at times gave precedence to often subjective feelings of customer well-being over their contractual obligation". | AMBER/GREEN (Graham) [no section below] There is an exciting possibility that S&U could leave its legal/regulatory difficulties behind it. I continue to believe that S&U itself was not specifically at fault for any of these problems, and that instead they are to do with the FCA's priorities and with the opinions of the courts on various matters to do with motor finance. Today's results show unusually large arrears and impairments in this division, which is not a surprise as repossessions were curtailed. The "skilled person review" (S166) has recently concluded and S&U has no exposure to the controversy over discretionary commissions. So things are looking brighter here than they have for some time. | |

accesso Technology (LON:ACSO) (£172m) | Rev in line, profit ahead. Slight reduction in revenue outlook. Growth unlikely to exceed 5.3%. | ||

Robert Walters (LON:RWA) (£164m) | Markets remained challenging. Limited visibility. Q1 net fee income down 16% at constant FX, down 17% at actual FX. Europe worst (down 24%), UK best (down 4%). Permanent recruitment, which is the majority of RWA's business, underperformed temporary recruitment. Headcount down 16% year-on-year. company is "highly selective in the replacement of fee earner natural attrition", i.e. not replacing all leavers. Net cash £42m. | AMBER (Graham) [no section below] My concern for the recruitment sector is growing as net fee income has been under pressure for what feels like ages - in the case of Robert Walters, it has been heavily declining for over two years, and their profit margins have collapsed. Is the decline purely to do with economic uncertainty and risk aversion on the part of candidates and corporates? Perhaps. But I find it strange that it persists in an environment of full employment in most major economies, when employees in theory have plenty of options to choose from and should be willing to move. Maybe it is a combination of economic risk aversion and other factors that are cutting out the middleman. Mark was neutral on this in March and once again I'm happy to leave the existing stance unchanged. | |

De La Rue (LON:DLAR) (£112m) | Recommended cash offer of 130p per share (£263m) from Atlas Holdings (ACR Bidco). | PINK (under offer) (Roland) [no section below]. | |

Renold (LON:RNO) (£99m) |

FY25 ahead of expectations. Positive momentum in the final quarter. | AMBER/GREEN (Roland) [no section below] | |

Billington Holdings (LON:BILN) (£60m) | Profit warning: reducing 2025 expectations to revenues slightly ahead of 2024 and FY25 PBT of £7.25m (versus £8.3m in 2024). | AMBER/RED (Roland) [no section below] | |

Kooth (LON:KOO) (£47m) | £15.8m adjusted EBITDA. £21.8m net cash. Outlook: continued US growth. UK remains complex. | AMBER/GREEN (Roland) [no section below] Results from this youth digital mental health specialist look promising, with revenue up 100% to £66.7m, all of which is classified as recurring. The group’s maiden operating profit gives a respectable 13.8% margin, suggesting profitability could be attractive as the business scales. In its core California market, the product now reaches 75,000 users. However, I would argue the political environment in the US makes the outlook for major new contracts hard to predict. Today’s results price the shares on a P/E of 7. Strong fundamentals mean I’m happy to upgrade our view from neutral to moderately positive. | |

Everyman Media (LON:EMAN) (£34m) | Operating loss £3.3m includes c. £3m of impairment charges. Trading in line. 6% fall in admissions would be needed to trip debt covenants. | RED (Graham) [no section below] The company continues to emphasise adj. EBITDA in its highlights, ignoring ongoing losses. It says it is "soundly financially structured". Checking the cash flow statement for a realistic picture, I see a £15m cash inflow from operating activities before changes in working capital. The company also benefited from £5.7m of landlord contributions to venue fit out costs and from stretching its payables. Against these positives, there was a capex bill for over £15m, and £8m of lease-related payments which appear separately on the cash flow statement. I'm still not convinced that this company is making meaningful profits and I agree with the weak StockRank it receives, categorising it as a "Value Trap". | |

Futura Medical (LON:FUM) (£27m) | Ahead of exps. Rev £13.9m, profit after tax £1.3m. On track to launch Eroxon in 20 countries. | ||

tinyBuild (LON:TBLD) (£22m) | Rev -22%, adj. EBITDA loss £3.7m. Operating loss of $20m including $14m of impairments. Outlook: in line. Net cash was £3.1m at the end of 2024 and is expected to trough in summer 2025 prior to the launch of new games. As of March, cash is in “the low single digit millions”. Strong pipeline for 2025 includes some higher-budget, high-potential games. Going concern note sounds shaky. | RED (Graham) [no section below] Please see my comments in February where I outlined this company’s history of cash mismanagement. I bring readers’ attention to the following sentence in the “Liquidity” section of today’s report: there can be no assurance that the Company will succeed in generating sufficient revenues from product sales to continue its operations as a going concern. The company has form for burning through cash and then coming back to investors for more. I think there’s a high risk that they will need another cash injection, unless they have some very successful game launches. | |

Nanoco (LON:NANO) (£14m) | Rev for FY July 2025 to be ahead of exps as result of settlement agreement with customer. | ||

Pod Point group (LON:PODP) (£10m) | PW. Adj EBITDA below market guidance of £14m by £8m, mostly due to a bad debt provision. |

Graham's Section

Liontrust Asset Management (LON:LIO)

Up 1% to 338.6p (£216m) - Trading Statement - Graham - AMBER/GREEN

Another day, another statement from a fund manager about their net outflows.

At least in the case of Liontrust, I’ve not been fully positive on it for some time - I’ve been AMBER/GREEN here due to some extra concerns I have around the company’s positioning and strategy vis-à-vis other fund managers.

More of the same from Liontrust today:

Net outflows £1.3 billion in the quarter ending March (Q4)

AuMA, assets under management and advice, falls 8.1% in the quarter.

AuMA has fallen another 4% since the end of quarter, to £21.6bn as at 10th April.

CEO comment:

It feels that over the past few years, the only certainty has been uncertainty. The current day-to-day unpredictability and fluctuations in markets reinforces our belief in active management and the long-term power of robust and repeatable investment processes.

Our focus remains on what is within our control. We continue to develop the business and are confident we have been making the right changes to ensure it is in the best possible shape for the future.

The statement argues that “The extreme volatility and dislocations we have seen in markets over the past couple of weeks are demonstrating the importance of, and opportunities for, active management and stock picking.”

But is that really true? I’ll be very curious to see whether active fund managers have proven their worth during this period, when the dust settles.

Liontrust provides good transparency in terms of the quartile ranking of their funds - note that this is not performance against benchmark, only performance against other funds. Beating other funds is typically much easier than beating a benchmark index!

I count that 23 out 53 Liontrust funds listed in today’s tables are in the bottom quartile in terms of their performance over the past year.

Or if we look at the 5-year column instead, I count that 26 out of 44 funds are in the bottom two quartiles, i.e. in the bottom half of funds.

And that may be a generous measurement. 5-year statistics tend to be subject to survivorship bias - in the fund management industry, underperforming funds often get closed down or merged with other funds, which removes them from the statistics.

I previously reviewed some of Liontrust’s funds and found they were heavily invested in shares with poor StockRanks. The performance tables suggest that many of their portfolios haven’t been holding up particularly well recently, or over the long-term.

I also note the following sentence under “Brand and Client Service”:

The Liontrust brand is very strong and we are continually engaging with our clients. We receive great feedback on our service and communications directly and through market research and these are more important than ever at times like this in helping clients to navigate volatile markets.

What’s bothering me here is the disconnect between the tone of the commentary and the reality of persistent net outflows for the past three years.

Graham's View

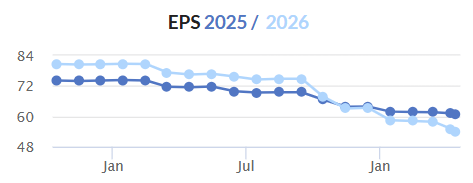

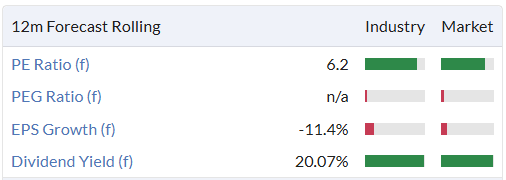

Despite my concerns, I think I can leave my AMBER/GREEN stance unchanged as the stock remains extraordinarily cheap with £100 of AUM for every £1 invested in the stock at the current price. The PER is only 6x although do bear in mind that earnings forecasts have trended lower:

The company has simplified by outsourcing various middle office functions and has cut costs with annualised savings of £6m achieved at a cost of £4.5m. One of my major issues with Liontrust has been management’s willingness to add complexity through acquisitions, when instead I thought they should be slimming down. It’s good to see that when push came to shove, they have simplified its operations.

I still prefer the other fund manager stocks by a wide margin. At the same time I don’t think I can justify a move down to a neutral stance here. It’s priced almost like a cigar butt stock, down nearly 90% from its peak in 2021. The current valuation says to me that outflows are expected to continue permanently, until it withers to nothing:

I think the best outcome for shareholders would be for Liontrust to simplify even further and then get merged into a larger fund manager who would remove even more costs and plug its AUM (and its brand) into an existing, highly profitable operating model. I’d have a strong suspicion that such a fund manager would be willing to pay more than the current market for over £20bn of AUMA.

See what our investor community has to say

Enjoying the free article? Unlock access to all subscriber comments and dive deeper into discussions from our experienced community of private investors. Don't miss out on valuable insights. Start your free trial today!

Start your free trialWe require a payment card to verify your account, but you can cancel anytime with a single click and won’t be charged.