Good morning! We have another mammoth set of updates to digest.

Spreadsheet accompanying this report (updated to 17/1/2025)

Companies Reporting

| Name (Mkt Cap) | RNS | Summary | Our view (Author) |

|---|---|---|---|

Associated British Foods (LON:ABF) (£14.1bn) | TU | Revenue warning: Primark now targeting low-single digit growth in 2025 (prev: mid-single digit). | AMBER/GREEN (Graham) Profit forecasts are unchanged and Primark is growing internationally. Interesting at PER below 10x. |

| IG group (LON:IGG) (£3.8bn) | Interim Results | Adj. PBT +30% to £267m. Extends buyback. Confident of meeting consensus rev & PBT for FY25.. | GREEN (Graham holds) Very impressive numbers even if only in line. New management team are interesting. |

Spectris (LON:SXS) (£2.7bn) | TU | Adj. op profit above consensus (£197m) at upper end of the range (£183.3 - 201m). | |

MITIE (LON:MTO) (£1.4bn) | Q3 TU | Good Q3 performance “underpins confidence” in FY adj, op profit of £225m, FCF at least £100m. | |

CMC Markets (LON:CMCX) (£746m) | TU | NOI in line with previous guidance, costs in line. | AMBER/GREEN (Mark) |

THG (LON:THG) (£582m) | Q4 TU | FY 2024 in-line with expectations, Gross Debt £550m | |

Boku (LON:BOKU) (£566m) | TU | Rev +20%, adj. EBITDA +22% | |

Ashtead Technology Holdings (LON:AT.) (£444m) | TU | Full-year revenues c. £168m, adj. EBITDA ahead of consensus. Growth to continue in 2025 in line. | |

Gulf Keystone Petroleum (LON:GKP) (£352m) | Ops Update | 2025 YTD gross production 47.9kbopd, 40-45kbopd guidance for 2025. Cash $102m. | AMBER (Mark) |

Team17 (LON:TM17) (£350m) | TU & Change of Name | Rev & adj. EBITDA slightly ahead of exps. New name “everyplay”, new ticker EVPL. | |

Mortgage Advice Bureau (Holdings) (LON:MAB1) (£368m) | TU | Rev +11%, adj. PBT +31% to £30.3m, ahead of consensus (£29.2m). Pent-up demand. | GREEN (Graham) Profits have beaten consensus with adj. PBT of £30.5m in a bad year. Mortgage applications are now rising at a solid rate (+15%) and I'm excited to see how MAB1 can perform in better market conditions. |

Forterra (LON:FORT) (£344m) | TU | Adj. EBITDA £50m, in line. Net debt lower than expected at £85m. Outlook: uncertain recovery. | |

Fonix (LON:FNX) (£202m) | TU | H1 adj. EBITDA in line. 3p special divi. O/look: stronger H2 weighting, confident in meeting exps. | |

Luceco (LON:LUCE) (£201m) | TU | Ahead of expectations. Rev +15%, Adj. Op Profit +20%. | GREEN (Mark - I hold) This beat highlights that this is a great business at a very reasonable price. |

Animalcare (LON:ANCR) (£165m) | TU | Rev +4.9%, underlying EBITDA in line with market expectations & prior year | |

Netcall (LON:NET) (£164m) | TU | Rev +22%, Adj. EBITDA +18%, in line with expecations | |

Zotefoams (LON:ZTF) (£143m) | TU | Rev. slightly ahead of current market expectations, Adj. PBT £15.6m ahead of expectations. | |

Iqe (LON:IQE) (£120m) | TU | Rev & Adj. EBITDA ahead of expectations. | |

Pharos Energy (LON:PHAR) (£107m) | TU & Ops Update | 2024 prodn 5,801 boepd, in line with guidance. 2025 guidance 5,000 - 6,200 boepd. | (Mark) |

Chapel Down (LON:CDGP) (£63m) | TU | Net sales -5%, in line with guidance, net debt £9.2m | |

Kooth (LON:KOO) (£63m) | TU | 2024 Rev in line, Adj. EBITDA ahead of expectations. | AMBER (Mark) |

| Watkin Jones (LON:WJG) (£51m) | Full Year Results | Revenue falls but adj. op profit improves to £10.6m. Medium term outlook remains strong. | AMBER/GREEN (Graham) Still no estimates for 2025. I leave my stance unchanged purely on the basis of balance sheet equity. Provisions might stabilise from here? |

Revolution Beauty (LON:REVB) (£46m) | TU | FY25 sales to decline 25%, high single digit £m underlying adj. EBITDA, net debt £26m | |

Iofina (LON:IOF) (£42m) | Corp Update | Prodn +13.4% within forecast range, strong spot prices, shipment delays mean adj. EBITDA $7.5m, below expectations. | (Mark) |

Angle (LON:AGL) (£42m) | TU | “Strong progress”. Rev +3%, ARR +6%. Net cash £1.1m, “sufficiently funded to execute its strategy”. | |

Getbusy (LON:GETB) (£27m) | TU | “Strong progress”. Rev +3%, ARR +6%. Net cash £1.1m, “sufficiently funded to execute its strategy”. | AMBER/RED (Mark) |

Skillcast (LON:SKL) (£37m) | TU | Rev +18%, ARR +25%, EBITDA in line at £0.5m, net cash £9.1m. | |

Robinson (LON:RBN) (£18m) | TU | Rev +14%, op. profit moderately ahead of current market expectations | AMBER (Mark) |

Smarttech247 (LON:S247) (£11m) | Final Results | Rev +8.2%, Adj. EBITDA -50%, Cash €3.34m down from €6.06m |

Graham's Section

IG group (LON:IGG)

Unch. at £10.71 (£3.8bn) - Interim Results - Graham holds - GREEN

At the time of publication, Graham has a long position in IGG.

We covered IG’s acquisition of FreeTrade last week. Today we have interim results with an in line outlook statement.

The headlines:

Revenue up 11% to £522.5m

Net trading revenue up 12% to £452m thanks to higher revenue per client. The number of active clients was down fractionally on the prior year.

Net interest income flat at £71m: higher client money balances, lower rates.

The result: adj. PBT up 30% to £267m. IG is less operationally geared than CMC Markets (LON:CMCX) but even IG in this case has enjoyed a very nice increase in profitability against a relatively modest increase in revenues.

In simple terms, IG’s trading revenue increased by nearly £50m, its operating costs fell by a few million, and there was a clean conversion into £60m+ of higher PBT.

And the accounts are fairly clean, with fewer adjustments than we saw in H1 last year. £266.8m of adjusted PBT becomes £249.3m of actual PBT.

H1 earnings per share, boosted by the above factors and by share buybacks, have risen by a remarkable 55% year-on-year (from 33p to nearly 52p).

Shareholder returns: the interim dividend gets a small increase to 13.86p (total value £49m) and the current buyback programme is extended by £50m to £200m.

CEO comment:

First half performance reflected more supportive market conditions, but we have work to do to grow active customers which will be necessary to deliver sustainably stronger growth…

Current trading has been satisfactory, and we remain confident of meeting consensus revenue and profit before tax expectations in FY25.

The new CFO gets a pleasant introduction to his new job, reporting positive news to shareholders. He says:

It is clear to me that IG has many strengths, including solid positions in large and growing addressable markets, geographically well diversified revenue, high margins and strong capital generation. However, we are competing against many new and highly capable players and there are many things we must improve to take market share.

Explaining the high revenue levels, he notes that "volatility normalised to long-term averages from unusually low levels in the prior year”.

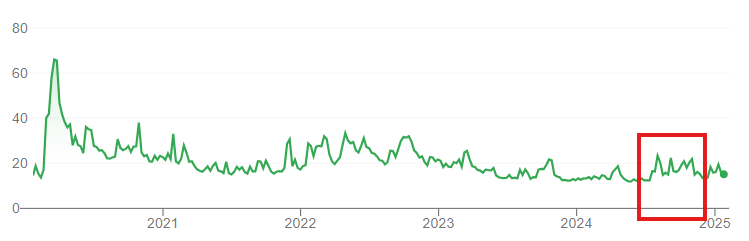

Here is the 1-year chart for the VIX Index, and I’ve put a red box over IG’s H1 period to help to demonstrate that yes, this was a period of much volatility:

Looking at this, you might think that H1 was an outlier with exceptionally high volatility. While its true that the spike in the VIX on 5th August was exceptional, I don’t think that the six-month period as a whole was particularly volatile. Here’s a 5-year chart for context:

Even so, there is a little bit of caution that volatility could revert back to lower levels, with an implication that IG would like to have a smoother revenue profile where it does not need supportive market conditions to do well:

Performance in the period was a good demonstration of IG's ability to capture cyclical upside, but our focus is on delivering sustainably stronger growth from more diverse revenue streams.

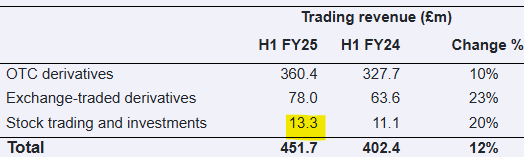

Revenue streams: I’m pleased to see continued growth from the “Stock trading and investments” segment, but it remains a minnow in comparison to the others:

Revenue per client in “Stock trading and investments” was only £157 in H1, vs. £2,523 in OTC derivatives (i.e. spread betting). It is far, far more lucrative to sign up a new spread betting client than it is to sign up a simple buyer and seller of stocks.

But it was a particularly busy six months for OTC derivatives clients, who had generated only £3,800 of revenue each during the previous financial year. And now they have generated more than £2,500 each in just six months.

Graham’s view

I’m GREEN on this again, for reasons mentioned before.

IG’s new CEO is the former high-profile CEO of Paddy Power Betfair which I think provides a useful background.

The new CFO has been hired directly from Virgin Money and has many years of experience as CFO at financial organisations.

I am pleased that they aren’t resting on their laurels on the back of this strong H1 performance, and are thinking about how to grow active clients.

On a broader point, I’m reassured by the company’s exposure to different risk factors. IG can benefit if any of the following things are true: interest rates are higher (the company benefits from higher interest on client balances), volatility is higher (so there is more trading activity), or markets are performing strongly (so that clients have more cash available to put on deposit). It seems to me that it’s a pleasant combination of factors where there should always be at least one positive driver of performance.

For a big company’s also a market leader, its progress in recent years has been staggered but very good:

Overall, I remain very happy to have this in my portfolio as it trades on a P/E ratio of about 10x.

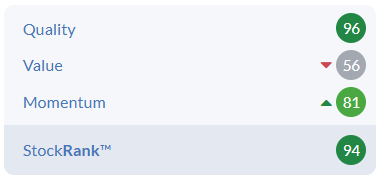

The StockRanks share my positive assessment:

Watkin Jones (LON:WJG)

Up 21% to 24p (£62m) - Graham - AMBER/GREEN

Thanks to JASVFS for requesting this one.

I was AMBER/GREEN (at 36p) on the day of the profit warning last August.

The company builds homes for rental, with a particular focus on affordable and student accommodation.

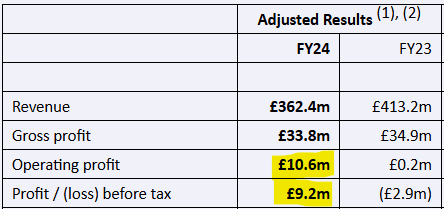

Today’s adjusted full-year results show an improvement on last year:

Watch out though - there are important exceptional charges. £7m of remedial costs for building safety, and £2.5m to reflect the passing of time as the building safety provision is measured at its present value rather than at the actual value that the company expects to pay.

The improved profitability (before exceptional charges) reflects the sale of two schemes and the successful completion of six schemes.

Estimates: the profit result has beaten the £7m estimate at Progressive, although revenue is a huge miss. There are still no estimates for 2025.

Dividend: there has been no dividend since 2023, as the Board prioritises financial flexibility.

This is necessary because of…

Provision for building safety works: there is now a net provision of £48m, down by nearly £7m year-on-year.

£16m was paid out in remediation works, in line with expectations.

However, £7m was added to cover new properties and to change the scope on properties that had already been provided for.

Outlook: they seem more confident in the medium-term than they are in the short-term.

Investment market gradually showing signs of recovery, though pace is likely linked to further reductions in gilt and interest rates.

Medium term outlook remains strong with excellent sector fundamentals continuing to drive investor sentiment and allocations.

Along similar lines, the CEO says that the investment market “has continued to be challenging”.

They want to do more forward sales, but it seems that it is difficult to get deals over the line in this interest rate environment, forcing WJG to develop “new approaches” and considering “differing types of transaction”.

The CEO continues:

We will continue to keep an open mind when exploring the funding options available to us, in order to provide a robust business in the long-term interests of our stakeholders.

Graham’s view: I’m afraid that higher rates have, for now, broken the business model as forward funding liquidity is not available in the amounts needed.

I don’t expect this situation to last forever, and so it makes sense to me that the company would be more confident in the medium-term than it is in the short-term.

A big worry for the short-term is building safety provisions currently standing at £48m (after £55.6m of total provisions are netted against agreed customer contributions to the works of £7.6m).

The company has a net cash position at year-end of £42.6m, and it acknowledges that this is a seasonal high as cash peaks around year-end.

That cash position will be needed to fund the remedial works. An important point is that the works are being carried out gradually, with an expected cash outflow of £10.6m to fund them in FY25.

That being the case, WJG should be able to use its generally strong balance sheet (and perhaps some future profits) to help pay for works over time.

Balance sheet equity is £133m of which its tangible value is £122m.

An important question is around the reliability of the provision for remedial works.

Here’s an excerpt from the footnotes:

The amount provided for these works has been estimated by reference to recent industry experience and external quotes for similar work identified. The investigation of the works required at many of the buildings is at an early stage and therefore it is possible that these estimates may change over time or if government legislation and regulation further evolves. If further buildings are identified this could also increase the required provision, but the potential quantity of this change cannot be readily determined in the absence of such identification through further claims or investigative work.

Unfortunately this reads in a very open-ended way, in terms of the potential cost.

Later in the footnote, WJG says that if an additional property is identified which requires remedial works for which they are liable, a reasonable estimate of the cost would be £0.9m. That at least puts some kind of limit on possible increases in the provision.

Despite the difficulties with the business model and the potential for rising provisions, I’d like to keep this at AMBER/GREEN, the same stance I had when the shares were at 36p.

The biggest risk is that the company’s cash position starts to get tight. WJG has a £50m borrowing facility which is only supposed to be used for land acquisitions and development, which I guess excludes remediation. At least they aren’t paying any dividends for now - almost certainly the correct call.

I keep coming back to that £122m tangible value on the balance sheet. Perhaps WJG should start to think about crystallising some of that value? Even if they don’t particularly want to, it could ward off any concerns that investors may have around financial stress.

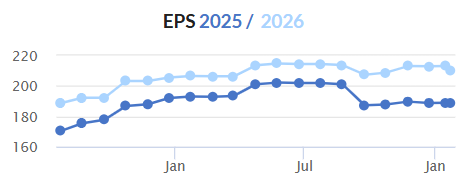

Associated British Foods (LON:ABF)

Down 3% to £18.77 (£13.7bn) - Trading Update - Graham - AMBER/GREEN

There is a tempering of expectations at Primark with only 2% sales growth over the 16 weeks to early Jan, including a 6% decline in like-for-like sales in the UK/Ireland.

The main disappointment was in womenswear which saw weaker sales in cold-weather and seasonal clothing.

All other regions - Spain, Portugal, France, Italy, Northern Europe, Central & Eastern Europe and the United States - all saw varying levels of growth.

Central & Eastern Europe and the United States, the two smallest regions, are currently being boosted by new store openings.

Grocery - revenue up 1%. Twinings and Ovaltine saw good growth, weakness in other brands.

Ingredients - revenue up 4%.

Sugar, Agriculture - small declines in both of these.

Outlook - Primark is now only targeting low-single digit sales growth in 2025, where it previously targeted mid-single digit sales growth.

Growth will come from store rollouts in international growth markets, offset by the weaker like-for-likes seen in the UK/Ireland in Autumn.

Fortunately the profit position shouldn’t change too much:

We continue to expect Primark's adjusted operating profit margin to remain broadly in line with last year's level, as gross margins have continued to improve and good cost management offsets inflation and the step-up in investment.

Graham’s view

I don’t have a strong view on this one but I’m happy to leave the AMBER/GREEN expressed by Megan in November unchanged.

The shares have been very weak in recent months:

But EPS forecasts have been holding up:

With the PER nudging just below 10x, I think this FTSE-100 member is not a bad candidate for investment.

Worth noting that it has official net debt of £2.0 billion, but this includes £3.1 billion of leases.

Mortgage Advice Bureau (Holdings) (LON:MAB1)

Up 9% to 688p (£399m) - Trading Update - Graham - GREEN

I left this network of mortgage advisers on my watchlist for 2025 and am pleased to see a brief but positive full-year update today.

Key points:

Revenues in 2024 rose 11% to £266m, much faster than the 4% growth in overall UK gross lending.

Adj. PBT is up 31% to £30.5m, better than the consensus estimate of £29.2m.

The number of advisors across the MAB1 network grew very modestly, but their productivity improved by 12%.

Outlook:

Clear signs of pent-up demand were evidenced by the increase in mortgage applications in Q4 2024 (+15% compared to Q4 2023) and we expect this positive momentum to be maintained. UK Finance forecasts gross new lending to rise 11% in 2025 in £235bn, which we believe is a realistic estimate.

In addition, the delivery of new technology enhancements and lead generation initiatives are expected to drive further growth this year, with many AR firms expecting to see adviser numbers increase, alongside a continued focus on increasing profitability through rising productivity.

Graham’s view

I’ve had this one on my watchlist because I’ve been so impressed with the company’s financial performance during a period (c. two years) in which mortgage volumes have been depressed or lethargic.

If the company is able to perform like this in stagnant conditions, I’m excited to see what it might do when conditions are more favourable.

We might get to see that this year, with new lending forecast to rise at an impressive rate.

I don’t see the shares as expensive here, given its underlying quality as a successful franchising business:

Mark's Section

Getbusy (LON:GETB)

Up 2% to 55p - Trading Update - Mark - AMBER/RED

The irony of calling this provider of productivity software for professional and financial services Getbusy is that they haven’t been very busy, nor productive:

Annualised Recurring Revenue (ARR) grew by 6% at constant currency to £21.6m with reported recurring revenue up 4% at constant currency to £20.8m. Total revenue was up 3% for the Year, at constant currency, to £21.4m.

This is barely in line with inflation. The good news is that they managed to increase adjusted EBITDA by 40% and now say that this was…

…the first year that the Group has broadly broken even at the Adjusted Profit level.

With the lack of top line growth, this presumably means that they have been cost-cutting. On one level, this means they have a good grasp of where they find themselves but this hardly reinforces the case for future growth. The other problem is that EBITDA is a poor metric for a company such as this that capitalises more internal development costs than it amortises. We need to focus on cash flow. Here they say:

Net cash at 31 December 2024 was £1.1m with available cash funds of £3.1m.

This has improved since the half year, where net cash was just £178k. However, it is still down on the previous year’s value of £1.9m. It is also a function of timing on how they get paid upfront for their software. Current liabilities exceeded current assets by £6.7m. While growing software companies can maintain this position almost indefinitely, any slip-up here will start to consume cash. So, while it is good that the company say:

The board considers the Group to be sufficiently funded to execute its strategy.

That they have to say this at all means that it isn’t necessarily a given. Despite these worries, the market cap remains a heady £27m. It looks like the StockRanks have got the measure of the investment opportunity here:

Mark’s view

It can be hard to value growth stocks that are just breaking into profitability. The problem here is that this company isn’t growing anywhere near rapidly enough to justify its current rating. It's an AMBER/RED for me.

Robinson (LON:RBN)

Up 11% to 119p - Trading Statement - Mark - AMBER

A return to growth for this plastic packaging manufacturer comes as some relief, as the trends towards avoiding plastics continue. This is driven mainly by volume, which is good news:

Revenue for 2024 is anticipated to be £56.5m, which is 14% ahead of the prior year. After adjusting for price changes and foreign exchange, sales volumes are also 14% higher than in 2023.

There is even better news on the profitability front:

The Company is pleased to report that 2024 operating profit before exceptional items and amortisation of intangible assets is expected to be significantly ahead of 2023, and moderately ahead of current market expectations.

House Broker Cavendish provide the details; upgrading Adj. EPS from 9.3p to 10.9p, a 17% uplift. This is a larger increase than the EBITDA increase, suggesting that progress on net debt is leading to lower interest costs too:

Net debt at 31 December 2024 is expected to be £5.9m (31/12/2023: £6.3m) following substantial capital expenditure in the year.

Cavendish say this is some £2.4m better than their previous expectations of £8.3m, driven by the uplift in profitability and better working capital management. Perhaps equally importantly, Cavendish upgraded FY25 EPS by a similar amount to 11.5p. This makes the forward P/E a very reasonable 10.3, even after today’s rise. Dividends are expected to be maintained at 5.5p for a 4.6% yield at today’s share price.

There is a chance that debt may be reduced further by excess property sales. However, these have always been pretty lumpy and plagued by delays over the years, so it may be too soon to count this chicken. The debt remains a significant part of the capital structure, and when I adjust for this, the forward P/E comes out closer to 14.

Mark’s view

The new CEO appointed in August is clearly doing things well here, with volumes up, costs controlled and good working capital management. However, the backdrop remains difficult, with plastic packaging increasingly being replaced with cardboard where possible. There will always be the need for some single-use plastics, but environmental pressures will constrain growth. As such, a debt-adjusted P/E of around 14 seems to be up with events, and I am neutral on the prospects here. AMBER

Gulf Keystone Petroleum (LON:GKP)

Down 1% to 160p - Ops Update - Mark -AMBER

Good news on the production front, as the company manages to produce and sell significant quantities of oil into the local market at the moment:

2025 year to 21 January gross average production of c.47,900 bopd

Guidance for the full year is a little below this level, but perhaps up a bit on 2024

2024 gross average production of 40,689 bopd, an 86% increase versus the prior year (2023: 21,891 bopd)....

Should local market demand persist at current levels, 2025 gross average production is expected to be in the range of 40,000 to 45,000 bopd

Being a rather simple business, we can work out what this would mean for future financials, taking the midpoint of the production guidance and 24H2 oil price received, and their net entitlement is 36%:

42,500 x $27.5 x 36% x 365 = $154m net revenue.

The other key figures are also given as:

Estimated 2025 net capex of $25-$30 million, reflecting disciplined and flexible work programme focused on safety, reliability and maintaining the capacity of existing wells…

Stable low costs, with expected operating costs of $50-$55 million and other G&A below $10 million in 2025

This works out to be around $90-95m of free cash flow. The current market cap is around $430m and EV around $330m. So the EV/FCF is just 3.6. This makes the company look very cheap, with a potential upside if their export pipeline ever gets approval to start again. The downside is that they operate in an extremely unstable part of the world, and that local demand for their oil can be very variable. Thier reserves should support production for many years. However, at some point, they may need to invest more into capex to maintain their infrastructure rather than just returning capital to shareholders.

Mark’s view

I think a strong argument can be made that the company is currently undervalued even on the current local production for which they receive low prices. However, the payment terms are very good here, with them receiving cash on delivery for every barrel. This has enabled them to pay good dividends and buyback shares. However, this remains incredibly risky, given the region in which the company operates and will only be suitable for the most risk-tolerant investors. As such, an AMBER rating feels like the right balance.

Luceco (LON:LUCE)

Up 9% to 136p - Full Year Trading Update - Mark (I hold) - GREEN

Good news at this supplier of electrical products:

The Group expects to report a full year 2024 performance ahead of market expectations*, with revenue in the region of £240m (2023: £209m) and Adjusted Operating Profit in the region of £28.5m - £29.0m (2023: £24.0m).

Helpfully, they provide the consensus:

Company compiled analyst consensus as at 22 January 2025 is for full year 2024 revenue of £234.2m (Analyst Range of £232.8m - £234.6m) and Adjusted Operating Profit of £26.5m (Analyst Range £26.0m - £27.2m)

This works out to be a 2.5% revenue beat, and an 8.5% Operating Profit beat underlying the operational levergae that this business has. The only updated research I can see is from Longspur, who don’t appear to have updated their block model to reflect the revenue figures the company has given today, so I am ignoring that. In the absence of better information, I would assume that EPS rises by a similar amount to the operating profit beat, which would be around 12.3p based on the previous consensus.

It seems that the trends that have seen many building products suppliers have a good 2024 are also having an effect here:

The strong order book from Q3, combined with increased trade and retail orders, led to impressive sales growth at the end of the year in the Group's Residential RMI divisions.

Plus, their move into EV charging is proving to be a good one:

Our Residential EV Charger division also continued to outperform, with quarterly year-on-year growth of c.50%, reflecting both a strengthening market and successful new product launches.

Not all of their 15% sales growth is organic, though. They delivered 5% organic growth. However, they continue to describe their markets as challenging so this can be expected to improve as market conditions do.

The market occasionally gets worried about the debt levels here, as the company are happy to make acquisitions via debt. They say:

The Group's balance sheet remains robust with Bank Net Debt at 1.7x EBITDA (within our target range of 1.0 - 2.0x) despite increased working capital requirements commensurate to the strong trading in Q4.

This may well be why the shares here have been weak recently. While debt levels may worry some, they have a history of paying down acquisition debt rapidly from internal cash flow. The leverage also gives the company great returns on equity:

The downside is that the multiples that look pretty cheap on the surface, are not as impressive if you adjust them for the net debt:

Mark’s view

This update highlights what we already know - that this is an incredibly well-run business with the ability to grow faster than its end markets via acquisition. Its operational leverage, combined with strong returns on equity, means that this strategy generates strong EPS growth over the long term. I don’t see why the company won’t be able to compound EPS at reasonable rates well into the future. While the rating isn’t incredibly cheap once you adjust for the debt, it is not expensive either. This is a great business at a very reasonable price, so I retain the GREEN rating.

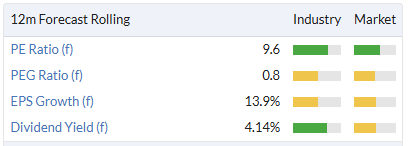

CMC Markets (LON:CMCX)

Down 14% to 227p - Trading Update - Mark - AMBER/GREEN

As commenters have pointed out this is very short statement here, which is in line with the guidance they had previously given:

The Group remains on track to achieve annual net operating income in line with previous guidance.

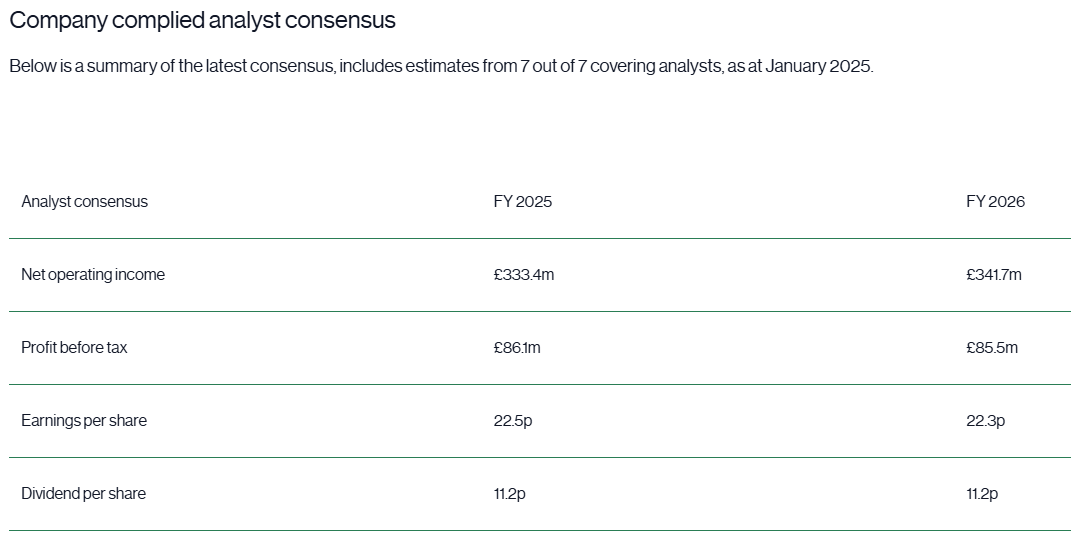

In their interim results, they said they were in line with market consensus, which they gave as:

External market consensus for year ending 31 March 2025 is net operating income of £332.9 million.

They also publish a consensus on their website that can be useful:

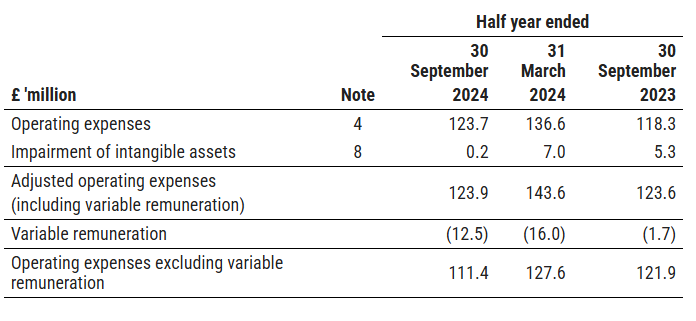

The other side of the equation is costs, where they say:

Management also remains confident in meeting its cost guidance of approximately £225 million, excluding variable remuneration and non-recurring charges.

It’s a shame to get no guidance on the variable remuneration, but perhaps they simply don’t know this until year end close. Here’s how the variable remuneration stacked up in H1:

So, backing out the analysts' consensus, this means £22.3m for variable costs for the full year, or £9.8m for H2.

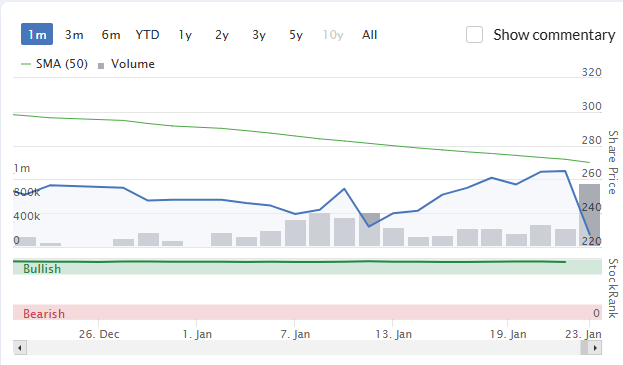

The share price has fallen 14% today. This may be the market doubting that the variable remuneration will be this low, or it may be that the market was expecting them to beat expectations. The share price was strong in the run-up to this trading statement:

After all, forecast valuation metrics prior to today’s fall had them at a premium to the sector:

Things look better when net cash is taken into account, though:

Balancing this, investors who enjoy being entertained should read the Glassdoor reviews on the company and CEO:

This hasn’t stopped them making money for shareholders in the past, of whom Cruddas is the largest, but perhaps means the risk here is higher than the sector.

Mark’s view

While there was nothing wrong with today’s in line update, the market was clearly expecting better. A relatively terse statement probably doesn’t build confidence. However, with the shares now trading at a similar P/E to peers, and cheaper on an EV/EBITDA basis, this is starting to look good value again. The share price is highly volatile, which means there will be a time to buy this again, I’m just not convinced that time is now. AMBER/GREEN for me.

Kooth (LON:KOO)

Down 2% to 170p - Trading Update - Mark - AMBER

Revenue is in line, showing some phenomenal growth rates here:

2024 revenues are anticipated to be in line with consensus market expectations of £65.8m (2023: £33.3m).

EBITDA growth is even better, and beats expectations:

Adjusted EBITDA is expected to be at or ahead of the top of the range of analyst forecasts of £12.7m (2023: £2.3m), helped by certain items which are not expected to recur in the current year.

However, it's this last line, which shows that the beat is likely a one-off, which is why the shares are actually down today in response.

I’m not sure I trust the broker consensus here, so doing some simple maths, at the half year, they said:

● Adjusted EBITDA to £7.8m (2023: £0.0m)

● Profit after tax of £3.9m (2023: £0.5m loss)

This gives H2 EBITDA of £4.9m. D&A in H1 was £2.6m, giving PBT of £2.3m and £1.7m PAT on a standard tax charge. That’s £5.6m PAT for the FY or 15.4p EPS. The P/E of 11, then, is potentially not that expensive for a company with their growth track record.

The problem is that their product, which is a mental health platform for teens, has faced some significant pushback in the US. The perceived issue is that parents do not have sight of the support given. My own view is that without something in place, there will be an increasing crisis in teen mental health, and the benefits outweigh the risks in this regard. However, logic rarely wins out in such emotive issues. The good news is that they keep winning pilot projects, although these won’t move the needle unless they become more than a pilot:

As announced in December 2024, Kooth has agreed terms for a new pilot contract with the State of New Jersey valued at $1.45m. Under the terms of the Contract, Kooth is providing mental health support via its Soluna platform to school districts within New Jersey, reaching 50,000 students aged 13 to 18. This pilot went live on 7 January. The Company continues to hold negotiations, which are expected to be concluded in Q1, regarding a second pilot contract in the US.

Mark’s view

This is a potentially interesting growth company, having a positive social impact and on a relatively modest valuation if my maths is correct. The problem is that the political risk in their key market of the US is almost impossible to quantify or mitigate. So it's an AMBER for me.

See what our investor community has to say

Enjoying the free article? Unlock access to all subscriber comments and dive deeper into discussions from our experienced community of private investors. Don't miss out on valuable insights. Start your free trial today!

Start your free trialWe require a payment card to verify your account, but you can cancel anytime with a single click and won’t be charged.