Good morning!

News feed - update 1045: apologies for the timing delay with the news feed this morning. This has now been fixed.

Wrapping it up for today (2pm) - thanks for all your comments, today's report is now complete.

Companies Reporting

| Name (Mkt Cap) | RNS | Summary | Our view (Author) |

Petershill Partners (LON:PHLL) (£2.6bn) | Full Year Results | Adj PBT +8% to $216m. NAVps +9% to 471 cents. Special divi of 14.0 cents. Outlook: mixed. | |

Pennon (LON:PNN) (£2.1bn) | Trading Update | Y/E 31 March in line with exps. EBITDA “broadly flat” vs H1 and capex “comparable” to H1. | |

Pets at Home (LON:PETS) (£1.1bn) | FY25 Trading Update | Y/E 27 March in line with adj PBT of £133m. FY26: adj PBT exp lower, in range £115m-£125m. | BLACK (PW) / AMBER/RED (Roland) Today’s update includes a profit warning for FY26 and news of a delay to the expected findings from the CMA investigation into UK vet chains. While I think this is a relatively decent business, I’ve downgraded our view to reflect tough conditions for retailers and heightened uncertainty on regulatory conditions for the vet business, which generates more than half PETS’ profits. |

| Conduit Holdings (LON:CRE) (£584m) | CEO Retirement & Trading Update | Founder/CEO Trevor Carvey to retire on 11 Apr 25 so that he can return to the UK for personal reasons. FY ROE guidance is cut to between “high single digits and low single digits” due to additional reinsurance costs. Broker PanLib has cut FY25 earnings forecasts by 30% to 52.1p but left FY26 unchanged at 108.8p. | BLACK (PW) / AMBER/RED (Roland) [no section below] |

Hunting (LON:HTG) (£517m) | Contract Wins | Subsea Tech order book now c.$85m vs $72.5m Dec 24. North Sea (c.$23m) and GoM (c.$15m) | |

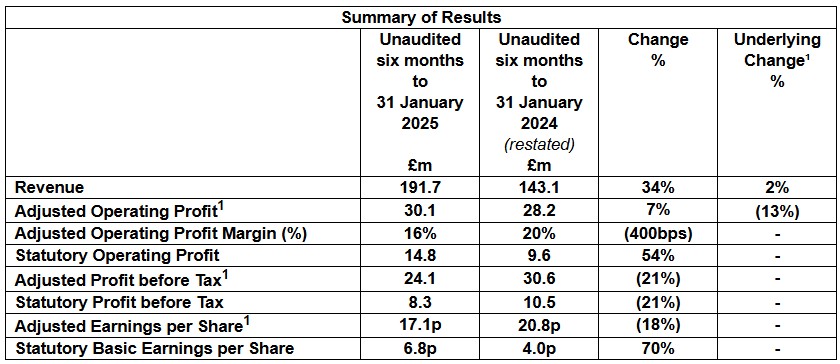

YouGov (LON:YOU) (£362m) | Interim Results | Revenue +34% to £191.7m (+2% underlying). Adj PBT -21% to £24.1m. FY25 outlook in line. | AMBER/RED (Mark) |

John Wood (LON:WG.) (£276m) | Business Update | Audit review has found multiple issues requiring “material” adjustments to FY22-FY24 accounts. Results exp delayed beyond 30 April, which may lead to the shares being suspended at this time. Takeover talks w/ Sidara continue. | RED (Roland) [no section below] Warren Buffett once said “there’s seldom just one cockroach in the kitchen”. This appears to be true here, as Wood Group reports a wide range of issues with past accounts, current projects and some financial controls. Takeover talks appear the main hope for shareholders. I don’t think it’s realistic for external shareholders to ascertain fair value here, so I see this as a situation to avoid. |

Idox (LON:IDOX) (£268m) | AGM statement | FY25 YTD trading in line with exps for higher revenue & adj EBITDA. Recent contract wins. | |

Reach (LON:RCH) | Directorate change (CEO) | CEO Jim Mullen is stepping down with immediate effect. He is replaced by former journalist and digital strategy exec Piers North. | AMBER/GREEN (Roland) [no section below] Mullen is being treated as a good leaver and starts a new role on 1 June. However, a CEO departure with immediate effect always raises an element of doubt in my mind. Graham went GREEN on Reach after reviewing its recent results, but Mark has also flagged up an apparent dispute with the pension regulator. I’ve opted to take a slightly more cautious view until we get an update on trading from the new CEO. |

Caledonia Mining (LON:CMCL) (£172m) | Full Year Results | Rev +25% to $183m, net profit $17.9m. 2025: 73.5k-77.5koz, AISC $1,690-$1,790/oz. | |

Team Internet (LON:TIG) (£153m) | Full Year Results | Rev -4.1% to $802.8m, adj EPS -5.5% to 21.2c. $36m impairment on Shinez. 2025 outlook unch. | AMBER/RED (Mark) [no section below] Another complex company to analyse so I turn straight to the cash flow statement and calculate £13.6m of FCF for the year. This makes the market cap around 10xFCF which seems not too bad until a quick look at the balance sheet reveals around £100m of net debt. An EV/FCF of around 18 just doesn’t seem cheap enough to overcome the weak balance sheet and that they seem to have to run hard each year simply to stand still. |

Bioventix (LON:BVXP) (£144m) | Interim Results | Rev +1% to £6.7m, PBT -4% to £5.1m. Increased Tau antibody sales for Alzheimer’s research. | AMBER (Roland - I hold) Today’s results appear to be slightly below previous expectations, but I think the bigger picture here for investors to consider is the likely (binary) outcome of BVXP’s Alzheimer’s efforts and the underlying value of the company’s core antibody portfolio. High quality without value or momentum make this a Falling Star – and a difficult situation to judge, so investors need to form their own view. My potentially-biased position as a shareholder is that a neutral view makes sense at current levels. |

Duke Capital (LON:DUKE) (£143m) | Trading & Ops Update | Exp Q4 FY25 recurring cash revenue +12% YoY to £6.5m (unch. vs Q3 FY25). | |

Jadestone Energy (LON:JSE) (£130m) | Drilling Update | Rig arrives for Skua-11 well side-track. $62m cost paid back in 16m with 65% expected IRR. YTD production slightly ahead of expectations. | AMBER (Mark - I hold - no section below) |

Spectra System (LON:SPSY) (£107m) | Full Year Results | Rev +142.5% to $49.2m, Adj. PBT +46.6% to $12.0m. Cash $13.4m. Flat dividend, “on track to achieve record earnings in 2025” | AMBER/GREEN (Mark) A 5% cut to FY26 EPS on pull-forward revenue concerns is doing the damage here today. However, they have been cautious on guiding brokers in the past, and I appreciate their conservative treatment of expenses in the accounts. There are enough near-term opportunities for contract wins that would have a material impact on FY26, for me to not be too concerned by today’s forecast revisions. |

Gaming Realms (LON:GMR) (£104m) | Full Year Results | Rev +22% to £28.5m, PBT +61% to £8.3m. Cash up to £13.5m, £6m buyback announced. Strong start to FY25, confident in strategy & expectations for the year. Canaccord Genuity leaves FY25 EPS estimates unchanged at 3.0p per share at this point - lower than consensus of 3.45p. CG expects stronger growth in FY26. | AMBER/GREEN (Roland) [no section below] Graham took a positive view on this stock in February after GMR’s FY update. Today’s results confirm these strong numbers, but Canaccord’s unchanged growth estimates for FY25 seem slightly disappointing. However, strong quality metrics and a P/E of 12 suggest to me this stock could still justify a higher rating, especially if the outlook improves as the year unfolds. The only caveat I’d add is that capitalised development costs flatter GMR’s earnings a little. My sums suggest free cash flow of £5.9m versus net profit of £8.7m. That implies a P/FCF of 17. On balance, I think the High Flyer styling is fair but have moderated my view a notch to reflect slower growth expectations than consensus estimates previously suggested. |

Quartix Technologies (LON:QTX) (£103m) | AGM statement | First two months of FY25 in line, outlook encouraging. | |

Inspired (LON:INSE) (£90m) | Full Year Results | Rev -5% to £93.8m, Adj. PBT down 24.7% to £11.9m, Net debt up 216% to £59.2m. | |

Anpario (LON:ANP) (£78m) | Full Year Results | Rev +23% to £38.2m, PBT +88% to £5.2m. Strong start to current year. | |

Mobile Streams (LON:MOS) (£58m) | Interim Results | Rev £415k, Op Loss £841k. First month of operating profitability in Dec 24. | |

Dialight (LON:DIA) (£46m) | Litigation agreement & TU | First $4m of $12m litigation settlement payment to Sanmina made. U/L Op Profit for FY25 ahead of expectations. US tariff impact on FY26 unknown. | |

| Invinity Energy Systems (LON:IES) | Q1 Trading Update | FY24 & FY25 in line with expectations. | |

Mind Gym (LON:MIND) (£23.6m) | FY Trading Update | Expects FY Rev. £38.6m, positive adj. EBITDA, FY25 in line with market expectations. PW for FY26. “remain profitable in FY26, albeit at a lower level than previously anticipated.” | |

Artisanal Spirits (LON:ART) (£23m) | Full Year Results | Rev & GP flat. EBITDA £1.1m vs -£1.0m. LBT £3.1m. Net debt £25.5m. | |

Cirata (LON:CRTA) (£23m) | Full Year Results | Rev +14% to $7.1m. Operating loss $13.5m. Cash $9.7m. Management thinks they don’t need a fundraise. | RED (Mark - no section below) |

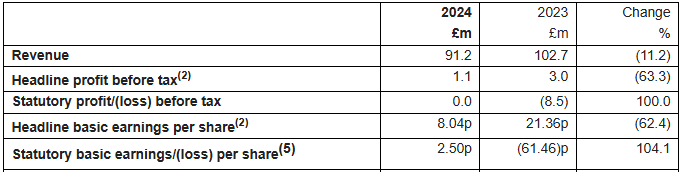

Portmeirion (LON:PMP) (£22m) | Full Year Results | Rev -11% to £91.2m, Adj. PBT down 63% to £1.1m, net debt up to £12.1m. Dividend cancelled. “2025 has started positively” | AMBER/RED (Mark) |

Altitude (LON:ALT) (£17m) | Trading Update & Contract Awards | FY25 rev £27-29m (FY24 £24m), Adj PBT £1.2-1.4m (FY24 £1.2m). Contracts with $6.5m annualised revenue won. | |

Itaconix (LON:ITX) (£15m) | Full Year Results | Rev -17% to £6.5m. GPM 34.7%, OCF -£2.75m, Net Cash £6.7m. | RED (Mark - no section below) |

Catalyst Media (LON:CMX) (£11m) | Interim Results | SIS rev. down 25% to £100.0m, Op. Loss reduced to £2.2m. CMG share = loss £0.41m. Cash £1.1m. | AMBER/RED (Mark - no section below) |

Roland's section

Pets at Home (LON:PETS)

Down 13% to 206p (£951m) - FY25 pre-close statement - Roland - BLACK (AMBER/RED)

Pets at Home Group plc, the UK's leading pet care business, today provides a pre-close update in respect to the 52-week period to 27 March 2025.

Today’s full-year update from the pet supplies and vet services group presents a rather mixed picture and includes a profit warning for the year ahead. That’s the second downgrade in six months for this FTSE 250 group:

FY25 update: PETS’ FY25 financial year ended on 31 March. Adjusted pre-tax profit for the year expected to be £133m, in line with November’s revised guidance.

Management says that fourth-quarter trading was “broadly as we planned” across both the Retail and Vet business, reflecting “a challenging and volatile UK consumer backdrop”.

However, the company is able to flag up some positives from the year just ended:

Record number of Pets Club loyalty scheme members

Completed transition to single distribution centre for store and online sales

New digital platform “also now functioning well”, with “strong growth in subscriptions”

Expect to finish FY25 in a net cash position (excl. leases), having returned £85m to shareholders during the year

FY26 outlook & profit warning: PETS says its network optimisation and digital platform investment have positioned the group for a return to retail growth. However, management flags up a somewhat mixed outlook for both Vet and Retail in the year ahead:

Vet: this division now provides more than half the group’s adjusted pre-tax profit, thanks to its superior margins versus retail. The outlook for FY26 seems fine, except for the continued overhang of the ongoing CMA investigation into large vet groups:

Tough comparatives for vet business against “exceptional” growth in FY24 and FY25;

Expect to add 10 new practices in FY26, with 15 extensions;

CMA investigation: provisional findings expected “over Summer 2025” rather than in May 25, as previously expected;

Insurance: PETS will invest £3m in a capital-light insurance offer to leverage its customer base, data and brand.

Retail: today’s profit warning is being driven by the tough conditions in this sector.

“Uncertain economic backdrop for both demand and inflation” – PETS expects UK pet retail market growth to be “subdued”;

£33m of cost increases: minimum wage/National Insurance increases will add c.£18m. Other increases include packaging regulations (£2m), “rebuild of variable pay” (£10m) and additional marketing costs to drive sales (£3m);

Planning “significant” cost savings to limit operating cost increase to 5% in FY26, however, any further cost mitigation will depend on sales growth and inflation;

Overall, “we expect retail underlying PBT to decline year on year”.

Outlook: Pets at Home now expects FY26 group underlying pre-tax profit to be within a range £115m to £125m.

Taking this mid-point of this range implies a reduction of 10% from the FY25 figure of £133m reported today.

Consensus forecasts on Stockopedia previously suggested earnings growth of c.8% in FY26, so this is effectively quite a material downgrade.

After this morning’s share price fall, I estimate FY26 adjusted earnings could be c.19p, versus previous consensus of 22.2p. That gives a possible FY26 forecast P/E of 11 at 205p.

Roland’s view

My general view on Pets at Home is that it’s a reasonably decent business. The group reports a 24% share of the UK pet care market and its horizontal integration of retail, vet and online makes sense to me.

Unfortunately, this is the second profit warning in six months, while the delayed CMA investigation continues to represent a further overhanging risk.

In my view, today's update highlights the main risks for investors here: a lack of pricing power in retail and a dependency on a high-margin service business whose pricing model could be disrupted by regulatory intervention.

Graham took a neutral view on PETS in February and I would previously have shared this view, given the stock’s Contrarian styling and strong value/quality metrics.

However, I think today’s warning and the delay to the CMA investigation justify a more cautious view. I’m going to downgrade our view to AMBER/RED until greater clarity emerges on the trading outlook.

Bioventix (LON:BVXP)

Down 8% to 2,550p (£133m) - Interim Results - Roland - AMBER

(At the time of publication, Roland has a long position in BVXP.)

Bioventix plc (BVXP) ("Bioventix" or "the Company"), a UK company specialising in the development and commercial supply of high-affinity monoclonal antibodies for applications in clinical diagnostics, announces its unaudited interim results for the six-month period ended 31 December 2024.

Today’s half-year results from Bioventix present a mixed picture. Sales of the Troponin antibody fell short of expectations once again, but there is continued positive commentary on progress with new ‘Tau’ antibodies that may eventually be used to create blood tests for Alzheimer’s Disease – potentially a huge new market:

Increased sales of Tau antibodies for Alzheimer's disease have been a highlight and we continue to remain excited about the future for these antibodies as the scientific output of our collaboration with University of Gothenburg increasingly translates into commercial success.

H1 results summary: Bioventix publishes wonderfully clean and concise accounts. R&D costs are all expensed as incurred (rather than being capitalised) and cash conversion is superb. There are no exceptional or adjusting items:

H1 revenue up 1% to £6.73m

Pre-tax profit down 4% to £5.05m due to higher R&D expenses

Net cash of £5.1m (H1 24: £5.5m)

Diluted earnings down 6% to 72.3p per share

Interim dividend up 3% to 70p (H1 24: 68p)

Bioventix generates revenue from physical sales of antibodies and royalty payments when tests incorporating its antibodies are used in customer machines (customers include big groups such as Roche and Siemens who sell blood-testing machines and associated reagent packs to hospitals).

Profit margins are eye–watering. Today’s H1 results show a 73% operating margin, which his at the lower end of the range seen in recent years:

Cash generation is also impeccable. Bioventix has no debt or significant lease liabilities. My sums indicate that today’s H1 net profit of £3.8m (H1 24: £4.0m) was converted into free cash flow of £3.7m (H1 24: £4.5m).

Trading commentary: this is a story of two halves – and in my view, understanding current trading and the possible medium-term outlook is essential for anyone considering the stock.

Core portfolio: Bioventix has a core portfolio of antibodies that are established, mature products used in a number of tests and are (probably) unlikely to be replaced due to the regulatory burden of gaining approval for new tests. The largest revenue contributor by far is the group’s Vitamin D antibody.

Collectively, sales from this core portfolio were largely as expected in H1:

Sales of our vitamin D antibody and other core antibodies were all more or less in line with last year's sales reflecting the mature nature of the diagnostic products that our antibodies support.

Troponin: this antibody is being produced under a licence that expires in 2032. Its main use is to help detect heart attacks, but sales have been lower than expected over the last year. A new usage application was approved in November, but it’s too soon to know if this will boost sales.

Alzheimer’s Disease (Tau antibodies): at present, testing for Alzheimer’s is a complex procedure, not suitable for widespread screening. A reliable blood test could change this.

With treatments now emerging for early-stage Alzheimer’s, demand for accurate and early-stage testing is also expected to grow very rapidly over the coming years.

This is cutting edge research where Bioventix appears to have some early momentum, but also faces a lot of competition. Over the next year or two, it should become clear if Bioventix is likely to be a winner in this market.

The outcome here will obviously have a very significant impact on the value and growth potential of the business – new antibodies take a long time to develop and certify for commercial use. Founder/CEO Peter Harrison admits that there is nothing else of comparable scale in the hopper at Bioventix.

Bioventix’s efforts are concentrated on ‘Tau’ in various formats (see the company’s website for more background). Some of these are now being sold commercially for research use only. This appears to be a positive sign, not only because they are generating revenue but because of the heightened level of interest implied from potential customers.

Today’s results include several positive statements:

The level of research interest at our in vitro diagnostic customers in the field of neurology, initially focusing on Alzheimer's disease testing continues to increase. Three of the Tau antibodies that Bioventix has created have already moved into full scale manufacture.

Increased sales of Tau antibodies for Alzheimer's disease have been a highlight and we continue to remain excited about the future for these antibodies as the scientific output of our collaboration with University of Gothenburg increasingly translates into commercial success.

Commercial approval for clinical use remains distant and uncertain. But recent progress definitely appears positive, in my view.

Outlook & Updated Estimates: Broker Cavendish has trimmed its FY25 estimates (y/e 30 June) today and commentary from the company suggests we might interpret these figures as a profit warning.

[we] anticipate a return to growth in 2026 and beyond as troponin and Tau revenues become more significant.

Today’s H1 results translate into earnings of 72.3p per share – only 42% of previous full-year forecasts of 171p per share. This deficit is not now expected to be made up in H2.

Cavendish has now cut its FY25 estimates from 171p to 151.5p per share, suggesting H2 earnings will be broadly flat on H1.

These numbers leave Bioventix trading on a forward P/E of 17 with a prospective dividend yield of 6.1%.

Roland’s view

I’ve written quite a lot about Falling Stars recently, here and here. Bioventix is another case study of a falling star where selling sooner would have avoided a painful drawdown over the last year:

As a shareholder I am obviously biased. But I believe today’s results from this niche antibody specialist highlight both reasons for optimism and reasons for further caution.

If Bioventix’s Tau antibodies end up forming part of a commercially successful test for Alzheimer’s, then I think it’s reasonable to assume the shares could be worth much more in the future.

However, I think it’s necessary to consider what might happen if the company doesn’t succeed in this new market.

The reality is that Bioventix is something of an outlier – it’s a very small business in a sector dominated by much larger groups. CEO Peter Harrison remains invested, but is perhaps nearing retirement age and certainly carries some key person risk.

Meanwhile, the company’s recent commentary has emphasised growing competition from Chinese firms and heavyweight western rivals. Its IP is possibly not as distinctive as it was 10-15 years ago.

If the company fails to develop a successful Alzheimer’s test, then I think the core portfolio of antibodies would still have significant run-off value. These sales generate high-margin royalties with very little investment or overhead required.

The regulatory burden of approving new tests mean that existing antibodies tend to remain in use indefinitely unless a markedly superior new antibody becomes available.

High levels of cash generation mean Bioventix shares could still provide a reliable income for the foreseeable future, even without any new product growth.

Using the current level of profits as a benchmark for sustainable (broadly flat) earnings, I estimate that a fair price for the business without any Alzheimer’s earnings might be £20 or perhaps a little more – still slightly below current levels.

Ultimately, the binary nature of this situation won’t appeal to everyone. My perception of the balance between risk and reward may also be skewed by my bias as a shareholder.

Bioventix scores highly for quality but lacks obvious value or momentum – this is a classic falling star scenario and a situation where DYOR applies even more than usual.

I think the group’s profitability and financial strength offset the disappointing performance implied by today’s results, so I’m going to take a neutral view. AMBER.

Mark's Section

Portmeirion (LON:PMP)

Down 2% to 152p - Preliminary Results - Mark - AMBER/RED

Like many producers and retailers, Portmeirion is highly sensitive to changes in revenue. So an 11% drop in revenue here has seen adjusted EPS drop 62%:

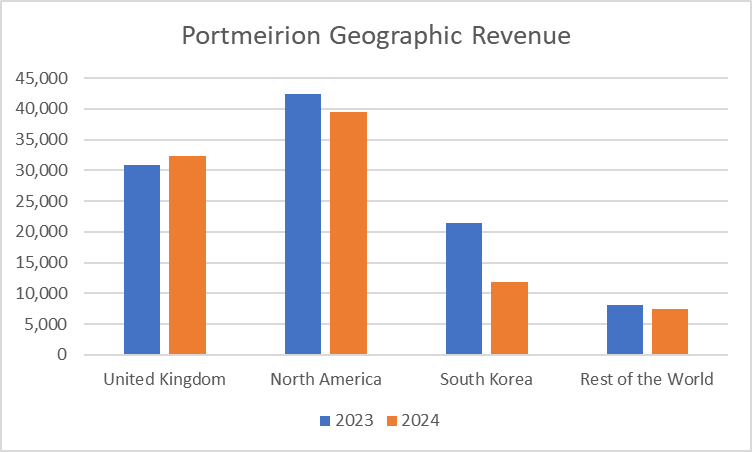

It is South Korea that has had the major impact, sales in the UK are actually up:

These are the reasons for what they describe as a “perfect storm” in South Korea:

…a level of overstocking in the market which was in the process of being sold through, just as new stock was arriving. At the same time our end customers were being hit by high inflation and weaker currency, driving much higher living costs and lower discretionary incomes.

No segmental breakdown of operating profits is given, but most of the volume is the same products sold in different regions, so it doesn’t really matter. The impact is that sales barely cover admin costs plus an increasing finance cost.

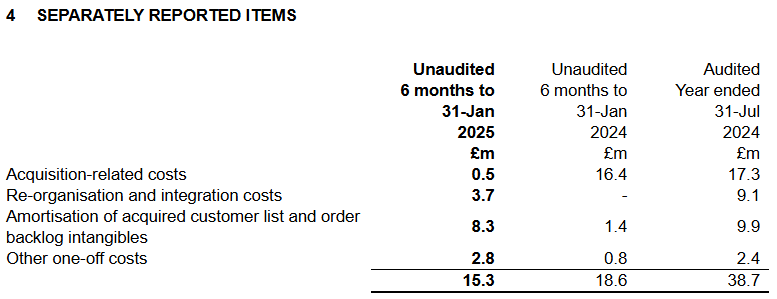

This is another company with a big gap between adjusted and statutory EPS, so looking at the details is always my first port of call:

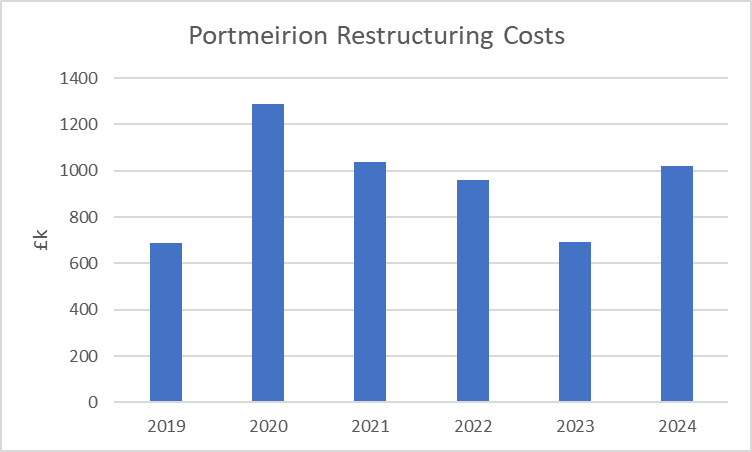

The problem is that there is absolutely no sign that restructuring costs are exceptional, or one-off for this business:

Realistically, this is a break-even result for the business.

The other ongoing cost has been the pension deficit recovery payments. The cash flow statement shows that they didn’t make any payments in 2024. However, this may not be the good news it first appears. There is no 2024 AR available yet, but the 2023 AR said “For the defined benefit scheme, the most recent triennial valuation was at 5 April 2020”. In the absence of any other news, this suggests that the 2023 triennial valuation hasn’t yet been agreed. This normally means that there is a disagreement over recovery payments with the trustee, with the trustee usually wanting increased payments. As Reach has shown recently, the trustee normally gets their own way, and if a dispute carries on, then the Pension Regulator may get involved.

Overall, free cash flow is negative, which means net debt has increased:

It is a bit misleading quoting the total dividend (although it is at least consistent with how they presented results last year) because the reality is that the final dividend has been cancelled:

The Board does not recommend payment of a final dividend

This isn’t surprising (at least to me). They have about £7m headroom to the £30m RCF they signed with Barclays last Summer. However, this isn’t huge compared to their working capital position. Speaking of which, the good news is that they still trade on around 0.5xTBV (even excluding the unrealistic “pension fund surplus”). This level of discount is not out of place for a break-even producer/retailer in the current markets. The bulk of the assets are inventories and receivables:

Portmeirion doesn’t reveal its gross margins, presumably scared about revealing to customers exactly how high their high mark-up is! They say:

Approximately 26% of our branded tableware products are made in our Stoke-on-Trent factory and we intend to increase this over the next 24 months. This may have an initial impact on our gross margins due to the cost of manufacturing in the United Kingdom, but it is a necessary margin investment in our brands. I am confident that we will recover the margin investment and reap substantial benefits over the medium term.

I think they are right in flagging that they have high margins overall due to their link to the pottery industry in the UK and keeping that holds up gross margins across the group. It is just a shame that the UK has pretty much the highest industrial energy prices in the world.

This means that the inventory should be able to be sold for much more than the book value, although it is hardly fast-moving at 153 Days Sales Inventories. The big question is, can those assets be made productive?

Outlook

Here they say:

· 2025 has started positively with actions currently underway on our strategic priorities to strengthen operations and position the business for sustainable future growth.

· The Board remains mindful of the challenges ahead in what continues to be an uncertain economic environment and with a significant Q4 weighting for the business.

With the US & Canada 43% of sales, this is a key market. One of the issues with 2024 appears to be the supply chain in this region. Where they say:

In addition, supply chain disruption, including East Coast port strikes in the run up to the election, delayed arrival of key Christmas stock resulting in cancelled and lost replenishment orders. However, despite supply chain costs, the gross margins in the US remained flat and overall net profitability increased 18%.

We are already advanced in bringing forward production of our key Christmas lines for 2025, creating additional contingency for unforeseen supply chain disruption.

While mitigating this is clearly the right thing to do, it means that they are not going to be able to make significant inroads into their inventory position in the near term, with the knock-on effect on debt and ongoing interest costs. They don’t mention the impact of US tariffs either, which would presumably be significant.

Shore’s note on the company is not viewable on Research Tree, and Singer say “Given several initiatives will be implemented to revive growth and improve the balance sheet over 2025/26, we opt to await to see progress before issuing FY25-27 forecast.” So we are a little blind here. Of course, when these arrive, they will be adjusted figures, so investors will need to take off the ongoing c£1m of restructuring costs each year, plus perhaps a renewed pension recovery payment.

Mark’s View

The 0.5xTBV is initially attractive, especially as the bulk of the assets are working capital. However, the route to making these productive again looks long and tortuous. The signs from the key market of the US are for increased working capital, and perhaps lower sales due to tariffs. With the dividend cut and the risk of increased pension recovery payments on the horizon, I can’t see any reason to change the previous AMBER/RED rating anytime soon.

Spectra Systems (LON:SPSY)

Down 6% to 206p - Audited Results - Mark - AMBER/GREEN

Revenue up 142% is a phenomenal result, but it gets less impressive as you go down the income statement:

· Adjusted EBITDA1 up 77.9% at $14,929k (2023: $8,394k)

· Adjusted PBTA1 up 46.6% to $12,064k (2023: $8,231k)

· Adjusted earnings per share2 up 36% to US 18.9 cents (2023: US 13.9 cents)

One of the reasons is that the gross margin has dropped from 67% to 48%. While there isn’t a full segmental breakdown of the business, looking at the EBITDA margins tells the story. Physical and Software Authentication EBITDA margins only dropped 1% to 43% on revenue up 70%. The difference is that the company bought Cartor at the end of last year, which is in the results as Security Printing. This added $16.3m of revenue but just $1.6m of EBITDA, i.e. much lower 10% margins.

The other reason for the lack of operational gearing is that operating expenses have increased:

However, it is refreshing to see a technology-led company expensing its R&D rather than capitalising it (especially when those same companies like to quote an EBITDA figure excluding amortisation.) There are no such games here.

Comparing these results to forecasts, their broker Zeus say that Revenue beat by 7%, however gross margins that were 6% lower than they expected means that adj. PBT come in in-line. Net cash is a little higher at $8.5m versus their $6m expectation. However, in light of this, it is a bit disappointing to see the dividend only held rather than increased as Zeus expected.

The downside is that Zeus see the revenue beat as sales pulled forward rather than a fundamental shift in outlook. The net result is that they have actually cut their revenue forecasts by 5% in FY25 and 7% in FY26. EPS is held in 2025 but cut by 5% in 2026.

The company don’t give any real outlook apart from being “on track to achieve record earnings in 2025.” This doesn’t really say anything, as we already know that 2025 will benefit from significant one-off sensor sales. It is the outlook and the cut to expectations for FY26 that actually make a difference to the forward valuation. Investors should be using the 22.7c of 2026. My calculations show that this is, therefore, on a forward P/E of around 10, adjusting for cash. It would appear that this downgrade, combined with a 2026 figure that isn’t immediately great value in a weak UK market, is causing the sell-off today.

Balancing this, they list many possible upcoming prospects. These are just the short-term ones:

· Execution of a new maintenance agreement for sensors currently being manufactured

· Delivery of all sensors to our customer to increase cash to the highest levels in company history

· Full qualification of our Fusion polymer substrate with a major central bank

· Sales of Fusion polymer substrate to a central bank and an invitation to tender for another

· Provide laminate printing including Spectra optical materials for a major Asian passport authority

· Swiss Post postage stamp contract

· Adoption of our smartphone technology and sale of our materials for several billion tax stamps per annum with a corporate partner

· Adoption of our covert technology in an EU passport

Given the timescales, it would seem that many of these will already be under consideration by potential clients, and in some cases, they have no real competitor. Therefore, there may be scope for today’s downgrades to be written back quite soon.

Mark’s View

While there is a risk that the forecast downgrades today may be the start of a negative trend, I am heartened by the tendency of the company to be conservative in both forecasting and accounting. The FY26 P/E doesn’t scream value but is very reasonable for a technology-led company with an in-demand product set. There are multiple near-term opportunities that may turn the tide and make the company look cheap on FY26 earnings. AMBER/GREEN

YouGov (LON:YOU)

Down 10% to 279p - Interim Results - Mark - AMBER/RED

Flat revenue, and increased costs sees Adj. EPS down 18%:

With the big gap to statutory EPS, I turn straight to the adjustments. Here is note 4 from the accounts:

While these are lower than the year before, they are still significant. Excluding acquired intangibles is common these days. However, I have to question that here. For many years, they have capitalised the costs of acquiring their “panels” of people who give their opinions. This is presumably the cost of advertising plus some vetting. It is unclear to me how valuable these actually are. There is surely no compulsion to be part of future panels unless they are paid, a cost which is then expensed. In the past, this flattered their results, but now appears to be costing them with their £19.6m of intangibles amortisation less than the £7.5m capitalised spend on intangibles. To my mind, there is no difference between a panel list or customer list that is acquired rather than generated internally via advertising, which means adjusting these out may not represent the underlying economics for this company.

In such complex scenarios, I turn to the cash flow statement. This shows £16.7m of net cash from operating activities, £10m of net investing, and £1.8m of lease principle payments. FCF for the half year is, therefore, £4.9m. Annualising this to around £10m and comparing it to the £330m market cap is not particularly favourable.

Part of this is an outflow of £14.6m from reduced payables, but looking at the balance sheet, this seems to be more a normalisation of this figure. Adding this back in means that the 3% or so dividend is covered, but it doesn’t leave a lot for incremental investment. Indeed, the balance sheet itself still looks a little weak, with a current ratio of 0.58. The net debt is £153m. There is also around £25m of short-term provisions and £13.5m of tax owed. While this situation looks worse than before, negative working capital is normal here and the banks seem sanguine about the risks.

Outlook:

This is in line for similar revenue trends to H1:

- The Group expects modest revenue growth for the rest of the financial year as trading conditions remain challenging reflecting the current macro-economic backdrop.

- We expect the Group to meet current market expectations for FY25, with operating profit delivery being more equally balanced between H1 and H2 due to phasing.

Mark’s View

Given the accounting treatment of intangibles, it can be a difficult company to assess. It doesn’t look cheap, at least on a free cash flow basis. While there don’t appear to be any immediate concerns, the balance sheet isn’t strong either, adding to the risk. In light of these factors, the outlook for a similar H2 to H1 makes this unattractive. AMBER/RED

See what our investor community has to say

Enjoying the free article? Unlock access to all subscriber comments and dive deeper into discussions from our experienced community of private investors. Don't miss out on valuable insights. Start your free trial today!

Start your free trialWe require a payment card to verify your account, but you can cancel anytime with a single click and won’t be charged.