Good morning and welcome back!

Megan published The Week Ahead, the preview for this week's set of announcements, on Friday. Here's the link.

Today's Agenda is complete (we think!).

12.55pm: all done for today's report, thanks!

Companies Reporting

| Name (Mkt Cap) | RNS | Summary | Our view (Author) |

|---|---|---|---|

Phoenix group (LON:PHNX) (£5.3bn) | Full Year Results | Op cash generation +22% to £1.4bn, in line with targets. CSM +14% to £3.3bn. Div +2.5% to 54p. | |

Qinetiq (LON:QQ.) (£2.9bn) | TU | Delays in UK/US contract awards. FY25 rev exp +2% at 10% margin, vs 11% prev. FY26 downgraded. | BLACK (PW) / RED (Roland) |

Sigmaroc (LON:SRC) (£1.1bn) | Full Year Results | Adj EPS +2.8% to 8.35p, “modestly ahead of consensus”. Outlook: 2025 “started positively”. | AMBER (Graham) [no section below] |

| Bakkavor (LON:BAKK) (£1.0bn) (14 Mar pm) | Possible offer | SP +17% on Friday Greencore (LON:GNC) made two offers for Bakkavor that were both rejected. Second offer: 85p in cash plus 0.523 Greencore shares plus final dividend, total value 189p, 25% premium. Bakkavor shareholders would own 40% of the combined group. | PINK (Graham) [no section below] A 25% premium can sometimes be enough but in reality it might be the bare minimum to get the attention of a company board. And that's when we're talking about all-cash offers. Where it's a mix of cash and shares, it's reasonable to expect more. In the case of Bakkavor, the two founders still own nearly 50% of the company. Perhaps they might be tempted at a better price? I can see the rationale to combine two giants in convenience food and create an entity with even more powerful economies of scale. However, I note that Greencore does not have a net cash position, and neither does Bakkavor. So the cash element of any deal would have to be borrowed. |

Marshalls (LON:MSLH) (£616m) | Full Year Results | Rev -8%, adj PBT -2% to £52m. Net debt reduced. Outlook: market recovery expected later in 2025. | |

Science (LON:SAG) (£188m) | Response to Ricardo | Science Group criticises Ricardo’s board and provides further detail on its analysis/proposed changes. | AMBER/GREEN (Graham) |

Beeks Financial Cloud (LON:BKS) (£171m) | Interim Results | Rev +22% to £15.8m. Adj. EBITDA +25% to £5.7m. Outlook: “within the range” of market exps. | AMBER (Roland) A solid set of H1 results are marred slightly by news of a one-off increase in customer churn and a shift to a new revenue-sharing model for EC contracts. Beeks will no longer receive payment for hardware on handover, but will retain ownership and be paid a higher monthly fee. Forecasts for FY26 have been trimmed. I can’t get higher than neutral on a P/E of >20. |

Harmony Energy Income Trust (LON:HEIT) (£148m) | Possible cash offer by Foresight | SP +20% to 78p | PINK (Graham) [no section below] HEIT invests in energy storage and renewable energy generation. It was already seeking to sell its entire portfolio to a third party. Since it's in wind-down it makes sense that it would be willing to accept a discount. NAV at Jan 2025 was 92.4p per share. This could be a great bit of business for Foresight's funds to get a collection of assets at a discount, and for HEIT to accelerate their wind-down |

Eagle Eye Solutions (LON:EYE) (£107m) | Half Year Results | Rev, adj. EBITDA flat. Confident FY2025 will be in line and confident in med-term milestones. | |

Batm Advanced Communications (LON:BVC) (£64m) | Full Year Results | Trading in the new year is in line. Momentum in Networking division. Diagnostics & Cyber to grow. | |

MTI Wireless Edge (LON:MWE) (£59m) | Final Results | SP -10% | AMBER (Graham) [no section below] These results are a miss against existing 2024 forecasts from broker Shore Capital, e.g. revenue misses by 5%. The RNS does not acknowledge any miss, only observing “extremely difficult conditions in Israel”. The Antennas division is providing all the growth right now and the stock could be considered a winner in the defence theme. However, I am going to downgrade this to AMBER as I have lost some faith in the reliability of forecasts after today’s RNS and share price reaction. It also doesn’t strike me as cheap with a PER in the neighbourhood of 20x. |

Hercules Site Services (LON:HERC) (£40m) | AGM Statement | Successful start to FY25. Expect strong growth to continue. | |

RC Fornax (LON:RCFX) (£11m) | Half Year Trading Update | Revenue +30% to £3.8m, in line. Outlook: confident on track to meet market expectations. |

Graham's Section

Science (LON:SAG)

Unch. at 420.2p (£188m) - Response to Ricardo plc - Graham - AMBER/GREEN

We’ve had a little back-and-forth between these two companies now, after Science started buying up Ricardo shares in a hostile manner. See our coverage on Friday.

On Friday afternoon, after 3pm, Ricardo went public with a written proposal it had previously received from Science group. Unsurprisingly, given what Science has been saying about the alleged failures of Ricardo’s directors, the proposal involved a variety of board changes:

The Chairman to be replaced by an Exec Chairman nominated by Science

Chair of Audit Committee to be replaced by a Science NED

Resignation of another unspecified NED

Ricardo aren’t too impressed by the actions of Science Group. But then, people don’t respond well to public criticism:

Science Group has acquired its shareholding in Ricardo over the last four weeks at a time when the share price has been at around a 15 year low. The Board believes that Science Group is opportunistically seeking to take advantage of the Company's currently low valuation and that its demands to replace identified Board directors is an attempt to gain control of the Company without paying a takeover premium.

They go on to defend their existing work on the transformation of Ricardo into a simplified environmental/energy consultancy, saying that the intervention by Science “will inevitably provide an unnecessary distraction from their efforts”.

They point out some possible issues with Ricardo’s proposal when it comes to the UK Corporate Governance Code and the requirement for independent directors (directors nominated by Ricardo would not be independent).

Finally, they note previous activity by Science:

The Board also notes that Science Group adopted similarly aggressive tactics in connection with its takeover of TP Group plc which completed in 2023. In that case, Science Group built an initial stake in the target company's shares, requisitioned a hostile general meeting to replace two directors and, having taken control, then oversaw a collapse in the company's share price prior to pursuing a takeover at a price which was approximately 40% lower than the prevailing share price had been when Science Group announced the acquisition of its initial stake. In 2019, Science Group also employed similar tactics at Frontier Smart Technologies Group Limited when it replaced a number of board directors with its own nominees prior to its subsequent takeover of the company.

In the archives, you’ll see that I was writing about Science Group’s acquisition of TP Group back in 2022. My impression of this deal is that it worked out reasonably well for Science. So in spite of Ricardo’s attempt to paint it in a bad light, I’m not sure if Science did anything terribly wrong in this case.

Today's RNS

Anyway, the war of words has now begun in earnest with Science publishing a response first thing this morning.

The Ricardo Board continues to seek to deflect from the fundamental issue, namely the poor performance of the company and the ineffective governance of the Ricardo Board which have resulted in the destruction of shareholder value.

I won’t go through all of the points raised by Science today. Suffice to say that they think the Ricardo board aren’t up to it, and they consider their demands for change to be reasonable.

There is an important point re: the Corporate Governance Code (one which I had already thought of!), which is relevant to this story and is important to bear in mind generally. The point is that it’s not mandatory for listed companies to follow all provisions of the code. What they are required to do is to explain themselves when they don’t follow the code.

So for example, it is possible to have a non-independent Chair. The company just needs to explain why it thinks the appointment is in the interests of all shareholders.

Science describes in detail the likely failure of Ricardo to achieve its 5 year objectives that were set out in 2022, concluding that the position of Ricardo’s current Chair is “untenable”.

They note that Ricardo’s board of directors collectively own 0.2% of their company, vs. Science’s directors owning 21% of their company (nearly all of this being owned by Science’s chair, Martyn Ratcliffe).

Graham’s view

A requisition for a general meeting seems inevitable with Science lobbying their fellow shareholders to shake up the board at Ricardo.

These shareholders include Gresham House (the biggest), Aberforth Partners and Royal London.

I welcome today’s RNS as we now know where everyone stands.

We know Science’s main arguments for change, and what they want to see happen at Ricardo. We also know Ricardo's position since Friday.

I’m inclined to leave my AMBER/GREEN stance on Science unchanged today, having downgraded it from GREEN last week.

I’m still a little concerned that attempting to control and improve Ricardo - a £150m market company - might be a very difficult and time-consuming task. For context, Science’s own market cap is comparable to Ricardo’s at £190m, and as I said last week, Science must have spent a very large portion of their last-reported net funds on this “strategic investment”.

Fixing bad or underperforming companies is a strategy that Science might be very good at, but this is different to what they’ve done before.

Their takeover of TP Group in 2022 valued that company’s equity at only £17.5m. So they could afford to buy it up and have total control.

With Ricardo, it’s hard to see how they can achieve anything like that level of control. They will need buy-in from other large Ricardo shareholders to achieve their goals - this is why I wondered aloud last week if they had been in touch with the other shareholders already.

Without the support of other shareholders, they will have about as much influence on Ricardo’s board as you or I would.

This is why I’m staying AMBER/GREEN on Science, rather than going straight back to GREEN: the outcome of this episode strikes me as highly uncertain, and it is already very expensive in terms of the cash spent on Ricardo shares..

Whatever happens, I think we can count on this war of words to continue for at least a little while longer yet.

Science’s shares continue to trade at above-average earnings multiples for companies in the professional services sector:

I also maintain the AMBER/RED on Ricardo.

Roland's Section

Qinetiq (LON:QQ.)

Down 17% to 436p (£2.4bn) - Trading Update - Roland - BLACK (RED)

QinetiQ Group plc ("QinetiQ" or the "Group") today issues a trading update covering the fourth quarter, updated year end expectations and an extension to our share buyback programme of up to £200m over the next two years.

QinetiQ has been a general beneficiary from the bull market in defence shares, but unfortunately that has not prevented this FTSE 250 firm from issuing a profit warning this morning:

What’s gone wrong? When I covered QinetiQ in January I noted the company reporting a weak order intake, albeit full-year guidance was left unchanged.

It looks the board was keeping its collective fingers crossed for a recovery ahead of the 31 March year end. Today’s update suggests this failed to materialise:

However, tough near-term trading conditions that we referred to in our third quarter trading update have persisted.

The company highlights weakness in areas where order book visibility is limited. These parts of the business each represent c.25% of group revenue, or c.50% in total:

This has affected short cycle work in our UK Intelligence and US Sectors resulting in further delays to a number of contract awards.

Management also makes an interesting comment about US demand:

In addition, recent geopolitical uncertainty has impacted our usual fourth quarter weighting to higher margin product sales from the US.

I’m not completely sure how to interpret this. With many to choose from, which geopolitical factors is QinetiQ referring to?

One possible interpretation I can see is that UK defence contractors relying heavily on US revenues could be finding it tougher to secure contracts from the new administration in Washington. I think this could be an area to watch.

More positively, the company says its FY25 book-to-bill ratio is expected to be “more than 1”, suggesting its order book should be similar to or higher than last year. Net debt is also expected to be in line with last year’s figure of £151m, which looks like it should be manageable to me.

Share buyback: QinetiQ’s management have also announced an extension of up to £200m to its current buyback programme, to be delivered from June ‘25 to June ‘27.

Management says this “will maintain leverage at around the current level over the next two years”.

Updated guidance: we don’t have access to broker notes for QinetiQ, so I’ve done my best to estimate the potential impact on profits using today’s updated guidance.

Organic revenue growth for FY25 to be c.2% at an underlying margin of c.10%, including c.£25-30m of one-off in year charges;

Checking back to January’s third-quarter update, the company was still maintaining its guidance for “high single digit organic revenue growth at stable underlying margin”.

I’m assuming the stable underlying margin referred to is the 11.3% margin achieved in H1 25.

Here are my before and after estimates, using FY24 results and Stockopedia’s consensus estimates:

Previously: FY25 revenue of £2,040m, underlying op profit £230m

New guidance: FY25 revenue of £1,950m, underlying op profit £195m

If I’m in the right ballpark, this suggests operating profit for the year ending on 31 March could be c.15% lower than previously expected. That’s in line with this morning’s share price fall, too.

In addition, the company highlights a number of one-off charges that will be added to this year’s (non-underlying) results:

£140m goodwill impairment relating to US operations

“Exceptional, largely non-cash charges” of £35-40m, mainly relating to “inventory and cost recovery” in legacy US operations

FY26 guidance also appears to have been cut:

FY26 revenue growth to be c.3-5% at margins of 11-12%

Previous consensus estimates appear to have been for FY26 revenue growth of 7%, although I think this margin guidance is broadly in line with previous expectations.

Roland’s view

The company says its long-term outlook remains positive and I probably wouldn’t argue with this:

Longer term, the underlying strength of the Group coupled with the relevance of our mission critical capabilities to the national security needs of our customers in the UK, US and Australia as well as NATO allies, positions us well for long term future growth.

However, I don’t have a great feeling about today’s update or QinetiQ’s near-term prospects.

Reading between the lines, I wonder if QinetiQ’s US business might be suffering from problems that are only just starting to become clear.

I also fail to see the logic in a company with net debt spending cash on buybacks at the same time as profits it’s cutting earnings forecasts. I am not sure QinetiQ’s shares are cheap enough to justify this, from a ROI perspective.

I estimate that the stock could still be trading on a low-teens P/E multiple after today’s drop. Given that our research has shown that a company’s first profit warning often marks the start of a period of underperformance, I don’t see any need to jump in just yet.

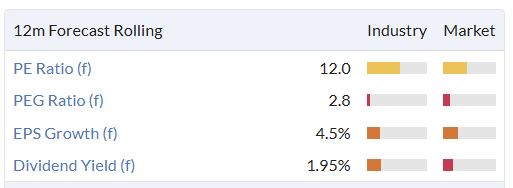

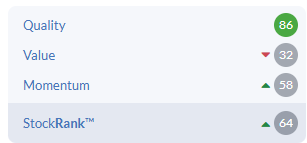

The StockRanks showed a high Quality score prior to today, but weak value and average momentum. I’d expect the momentum score to drop when today’s profit warning is reflected in updated consensus forecasts.

I was neutral in January, but am going to go RED after today’s update, pending clarification on trading and outlook when the company’s full-year accounts are published in May.

Beeks Financial Cloud (LON:BKS)

Down 18% to 202p (£138m) - Interim Results & First Cryptocurrency Exchange Win - Roland - AMBER

Today’s half-year results from this “cloud computing and connectivity provider for financial markets” have been overshadowed by news of higher churn in H1, and the company’s decision to shift to a revenue-sharing model for some of its Exchange Cloud contracts.

As a result of these factors, broker Canaccord Genuity has cut its FY26 earnings forecasts by 4% to 9.1p per share.

Let’s take a closer look at today’s results.

H1 results summary: today’s numbers cover the six months to 31 December ‘24 and show continued progress at this AIM-listed business:

Revenue up 22% to £15.8m

Annualised Committed Monthly Recurring Revenue (ACMRR) up 7% to £28.5m

Underlying pre-tax profit up 37% to £1.9m

Underlying PBT margin: 12.0% (H1 24: 10.6%)

Reported pre-tax profit up 188% to £0.5m

Underlying EPS up 47% to 2.6p

Net cash of £6.6m (30 June 24: £6.6m)

Trading commentary is mostly positive:

Approval and launch of “the multi-year contract with one of the largest exchanges globally” (presumably this is the NASDAQ contract), with first customers now on-boarded and progressing to plan.

Post-period win with Grupo Bolsa Mexicana de Valores, the second-largest exchange in Latin America

Expansion with existing customers including the JSE

ACMRR “further increased to £29.2m as at the end of February 2025”

However, one item sounds less positive to me, although the company says it should be a one off:

during the period we had some higher than historic customer virtual private server churn following the transition of our server licence estate from VMWare to OpenNebula, as clients cleared out some legacy infrastructure. These reductions have now stabilised and are not expected to recur.

There’s also news that Beeks is venturing into the crypto space with well-respected crypto exchange Kraken:

First Exchange Cloud win in crypto space under new revenue share model, further increasing the TAM for Exchange Cloud as we enter new asset classes. Kracken [sic] is one of the longest-standing, most liquid and secure cryptocurrency exchanges

I have no idea what the potential addressable market value of crypto exchanges could be relative to conventional financial exchanges.

However, this deal also highlights a more mixed item of news from today’s results:

Transition to a revenue-sharing model for Exchange Cloud contracts to enhance profitability and drive long-term value

Frustratingly, the company does not provide any detail on this new revenue-sharing model in today’s results. This means investors without access to broker notes are left in the dark on its potential implications.

According to today’s Canaccord note, the implications could be quite significant:

Existing Exchange Cloud (EC) customers pay 40-50% of the total contract value upfront when hardware is handed over to the exchange

Under the new arrangement, Beeks will retain hardware ownership and receive (higher) monthly recurring fees

This is expected to result in an increase of “>30%” in total contract values and better long-term visibility

However, it creates “a temporary headwind in FY26” with a return to double-digit growth “highly likely in FY27”

This kind of pricing is common in Software as a Service scenarios, where the incremental cost of adding new customers is low.

However, Beeks’ model includes expensive hardware which will presumably now take longer to earn back its cost. I would imagine we could see the company’s working capital requirements expand, at least temporarily. Fortunately, Beeks has a net cash position at present, but this is something I’d watch over the next year.

The scale of the impact of this changed pricing mode is likely to depend on the rate and type of new customer wins (not all are Exchange Cloud).

Outlook: CEO Gordon McArthur’s guidance for the second half of the year appears to be in line:

Outlook for FY25 remains positive and within the range of market expectations

Canaccord has upgraded FY25 forecasts marginally today, but as I mentioned earlier, FY26 estimates have been cut.

Here’s a summary of the latest numbers from Canaccord Genuity, with thanks for making this coverage available:

FY25 EPS 7.8p (previously 7.7p)

FY26 EPS 9.1p (previously 9.5p)

Roland’s view

I understand that Beeks can potentially address a large market with its services and may still have a long runway for growth. But I’ve always been a little worried about the extent of the upfront investment that’s required before any meaningful profits are earned.

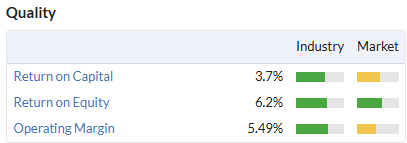

Quality metrics have improved somewhat in recent years, but remain below the level I’d see as attractive:

Today’s shift to a revenue-sharing model for EC contracts could potentially make this problem worse, in my view, at least in the short term. I wonder if it also signifies competitive pressures.

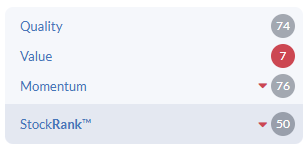

My feeling is that Beeks’ previously high MomentumRank and its High Flyer styling could come under pressure following today’s updated forecasts:

With the stock still trading on a FY26 P/E of 22 and some uncertainty about the outlook for the next 18 months, I think it makes sense to take a neutral view at this point. AMBER.

See what our investor community has to say

Enjoying the free article? Unlock access to all subscriber comments and dive deeper into discussions from our experienced community of private investors. Don't miss out on valuable insights. Start your free trial today!

Start your free trialWe require a payment card to verify your account, but you can cancel anytime with a single click and won’t be charged.