Good morning! We've finished the Agenda now

1pm: all done for today! Thank you.

| Name (Mkt Cap) | RNS | Summary | Our view (Author) |

|---|---|---|---|

Assura (LON:AGR) (£1.3bn) | Possible Offer | KKR says it made four proposals to buy AGR, latest at 48p. All were rejected by AGR board (SP: 39p). | AMBER/GREEN (Graham) |

MONY (LON:MONY) (£1.0bn) | Final Results | 2024 rev +2% to £439m, adj EPS +5% to 17.1p. 2025 adj EBITDA to be “broadly within” consensus. | GREEN (Graham) Top-line growth is limited and the company has a big exposure to rising advertising costs. But almost everything else about MONY looks perfect to me, so I maintain my positive stance. Also please see my 12 Stocks of Christmas article. |

Oxford BioMedica (LON:OXB) (£414m) | Full Year TU | 2024 was in line. Organic revenue growth 78-81%. EBITDA profitability in H2. Outlook in line. | |

Frp Advisory (LON:FRP) (£344m) | TU & Dividend | FY April 2025 will be ahead of expectations. All service pillars ahead. Q3 divi 0.95p (LY: 0.9p). | GREEN (Roland - I hold) |

Wilmington (LON:WIL) (£336m) | Half-year Report | Trading is in line. Net cash £31m. Organic revenue +3%, total revenue +16% (acquisitions). | AMBER/GREEN (Graham) This group of training businesses doesn't strike me as particularly cheap and there is some complexity to be digested, so I'm downgrading it from GREEN. |

hVIVO (LON:HVO) | £2m contract win | New client has signed contract for a hMPV trial following hVIVO/s successful recent hMPV pilot. | AMBER (Roland) [no section below] |

Springfield Properties (LON:SPR) (£117m) | Interim Results & Land Sale Agreement | £64m land sale to Barratt. H1 adj PBT up 90% to £3.8m. FY25 profit to be sig. ahead of exps. | AMBER/GREEN (Roland) |

Creo Medical (LON:CREO) (£78m) | FY24 TU | 2024 revenue exp £30.4m, flat YoY. 2025 trading “positive” and in line with mgt expectations. | |

Ebiquity (LON:EBQ) (£30m) | Appointment of NOMAD and TU | Appoints Cavendish. TU: 2024 was in line. | AMBER (Graham) [no section below] I’m leaving our neutral stance unchanged after an in-line trading update. The company trumpets 2024 year-end net debt of c. £15m being better than expectations, as it previously announced in December, while glossing over the fact that the trading update in December was a profit warning. In that sense, this is a very unhelpful update. |

Tekcapital (LON:TEK) (£20m) | 2024 TU | Net assets $65.1m at year end, +36% YoY. NAVps of 25p. | AMBER (Graham) [no section below] This investment group says that its portfolio is valued at $64.2m, equivalent to £51m. Four of its five portfolio companies are publicly listed and the fifth is preparing for a NASDAQ float this year. The unlisted company was valued at $18m as of June 2024. TEK's investments are too early-stage for me but maybe it is trading cheaply at this level, especially as all of its holdings will be publicly-listed soon. Could there be a way to arbitrage this? |

Touchstar (LON:TST) (£7m) | TU & Conclusion of Strategic Review | 2024 better than management expected. Positive outlook. Will remain as stand-alone listed co. |

Graham's Section

MONY (LON:MONY)

Up 5% to 199.1p (£1.06bn) - Preliminary Results - Graham - GREEN

I last looked at this one at its Q3 update last October.

Then it said that full-year adj. EBITDA was heading for £135.8 - 142.1m, in line with expectations, with an average estimate of £140m.

The actual result is at the top end of this range: £141.8m, up 7%.

Conversion from adj. EBITDA into actual profits is excellent: there is £80m of after-tax profits, up 11%.

The most impressive aspect of this profit growth is that it came from revenue growth of only 2%.

The company points to “robust cost management” to explain the growth in the adj. EBITDA margin.

Balance sheet: the company moves from net debt of £20m last year up to net cash of £8m, and announced a share buyback for £30m. There is also a small increase in total dividends for the year.

It doesn’t particularly concern me in this case but I should mention, as I do for many companies, that MONY has negative net tangible assets. The deficit isn’t huge, but it is there - tangible assets are £150m, and you might also want to subtract a few million pounds for the “non-controlling interest” in some subsidiaries, and then you are left with £145m. Against that figure, there are total liabilities of £157m, for a deficit of £12m.

I don’t think it matters because:

a) MONY has net cash. The liabilities creating the deficit items such as deferred tax liabilities - which can be paid out of future profits.

b) in the nature of the business, it shouldn’t need very many tangible assets. That’s one of its attractive features!

c) cash generation is fabulous: there was £115.6m of net cash flow from operating activities, and only £14m of net cash was used in investing activities. This enabled £65m of dividends, the reduction of debt, and an increase in the company’s cash balance.

Note the attractive yield, fully paid for from cash flow (at least historically - hopefully 2025 is just as good). And with a buyback coming on top of this yield:

Strategic highlights - they now have 1 million members on SuperSave Club and 35 B2B partners including Auto Trader (LON:AUTO) and Rightmove (LON:RMV) (I hold RMV).

On the customer side, MONY’s plan is to convert customers from “transactional users” into long-term members who voluntarily come back to them without the need to see an ad. Pay-per click costs have risen by an extraordinary 19% in H2 vs. H1.

The Board’s KPIs are all moving in the right direction, except for active users - due to a decline in energy enquiries:

CEO comment:

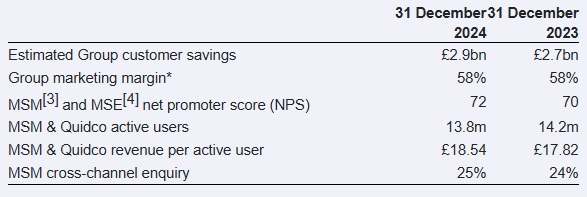

"We are proud to have helped customers save a record £2.9 billion - the more customers save, the more the Group grows. We've done this by delivering strong performance both operationally and financially in 2024 as we continue to execute on our strategy. This includes encouraging customers to join our member-based propositions like the SuperSaveClub which, in turn, reduces our reliance on increasingly expensive pay-per-click (PPC) marketing….”

Outlook is not the strongest, with 2025 adj. EBITDA to be “broadly” within consensus.

The current 2025 consensus is for adj. EBITDA of £143.1m - £151.7m.

It’s a wide range but we are still very early in the year.

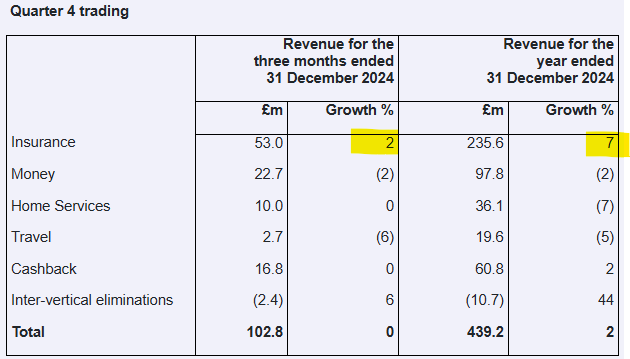

Trends by category: Travel (excluding travel insurance) remains quite weak in the short-term. Thankfully this is the smallest category. The key Insurance segment continues to do ok. It was up 1% year-on-year in Q3, and now it’s up 2% in Q4:

2% growth in Insurance came “despite premium inflation in car and home returning to more normal levels, with travel and life performing particularly well”.

Graham’s view

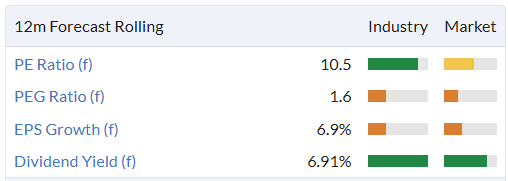

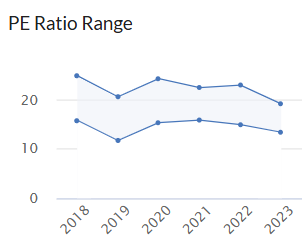

I remain a big fan of this one.

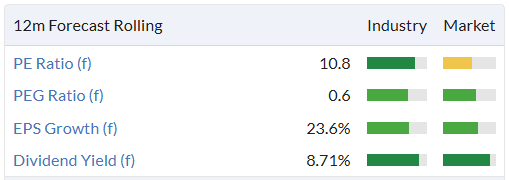

In December, I picked MONY as one of my 12 Stocks of Christmas. Looking at valuations for Gocompare and Comparethemarket, I concluded that a PER of 15-18x was about right.

MONY has traded at and above that level in the past.

However, it now only trades at 10x.

I think this is just too low.

Top-line growth is admittedly quite pedestrian right now, and the recent surge in advertising costs are a threat. These are the two main detractors to the investment thesis, in my view.

Against that you have a fantastic track record of real profitability, prodigious cash flow, and sizeable market share in a space that is controlled by only a few operators (Comparethemarket being by far the largest of these).

MONY appears to acknowledge the challenges it faces and the strategy of converting users into dependable long-term members makes perfect sense to me.

For me, the positives continue to strongly outweigh the negatives and I can’t consider changing my positive stance on it for now.

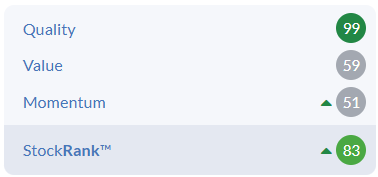

Note the perfect QualityRank of 99:

Assura (LON:AGR)

Up 16% to 45.1p (£1.5bn) - Possible offer for Assura plc - Graham - AMBER/GREEN

At 5.10pm on Friday, this healthcare REIT announced that it had been approached by two parties: the private equity giant KKR, and the investment managers for the UK’s Universities Superannuation Scheme.

It said it was reviewing the proposal.

This morning, we have had announcements from the two parties.

Firstly, the Universities Superannuation Scheme said it did not intend to make an offer for Assura, either as part of a consortium with KKR or otherwise.

KKR has had more to say.

It has explained that it made four proposals to Assura.

The fourth and most recent one (made last week) was a cash offer at 48p per share, which was at a 28% premium to the share price at the time.

However, it was still a small (2.8%) discount to Assura’s Net Tangible Asset value as of Sep 2024 (49.4p). And of course the NTAV may be higher than that now.

KKR reveals that on Saturday, the Board of Assura rejected the 48p bid.

So what next?

KKR is considering whether there is any merit in continuing to try and engage with the Board. There can be no certainty that any firm offer for the Company will be made. A further announcement will be made as and when appropriate.

With the Universities Superannuation Scheme out of the picture, perhaps KKR will not want to go it alone?

Trading update

There’s a company-specific situation, but there’s also a broader point about value in REITs at the moment.

Looking at Assura itself, the first thing I’d say is that if I was on the board of a REIT, I would never sell out for less than TNAV - unless the alternative was bankruptcy.

Secondly, the company had a trading update last month that was very positive. They do have a stretched balance sheet (49% as of the interims), but said they were “on track” to get this below 45% over the next 12-months.

Net debt to EBITDA was 9.7x which in a REIT context I don’t have a big problem with. Valuation against TNAV is what matters to me, and interest cover if the company is indebted.

But Assura is working on its net debt/EBITDA multiple and similarly said that it was on track to get it below 9x over 12-18 months.

There was “positive progress on rent reviews” with a £0.6m uplift, another £35m of rent (20% of rent roll) due to be reviewed in Q1 2025, and a pipeline of projects and opportunities to work on.

On the debt front, the company enjoys an A- rating from Fitch. Net debt was £1.5bn and the weighted interest rate being paid was less than 3%.

Graham’s view

On the basis of that January update, and also the interim results, I don’t see why Assura would be in a rush to sell out at a discount to TNAV.

We have already lost so many UK-listed companies to opportunistic bids. Perhaps REITs will be the next to go. But selling at a discount can’t be right. Perhaps we’ll see a nice gain in TNAV on the March 2025 balance sheet, along with deleveraging progress. So why sell out at a discounted price?

I’ll take an AMBER/GREEN stance on Assura as a gain in its share price from its current level to TNAV would return c. 9.5%. On top of that it offers a yield of nearly 9%:

Assura’s customers - GP surgeries, diagnostic and treatment centres - are, I presume, highly reliable paying tenants who relocate very rarely.

The broader point is that there are opportunities in REITs which, along with many other sectors, appear to offer good value in the current environment. There are dozens of choices in the sector but a quick review of some of the bigger ones gives me SGRO at a P/TNAV of 0.82x, LAND at 0.68x, SHC at 0.7x, HMSO at 0.75x, and GPE at 0.62x.

I haven’t reviewed these individually for debt levels or quality, I’m just pointing out that the sector is in general available at a meaningful discount to TNAV.

Returns from REITS are in theory less exciting than the returns from other equities, but perhaps the risk:reward currently available in the sector might be attractive to some readers. I do think that it’s hard to go far wrong if you find a low-risk REIT at a good discount to TNAV. It won’t offer the upside potential of an operating business, but it will be harder to lose money on it!

Wilmington (LON:WIL)

Down 11% to 328.4p (£296m) - Half-Year Report - Graham - AMBER/GREEN

There have already been some excellent comments in the thread below re: Wilmington. Let’s see if I can add anything.

The company provides “data, information, education and training services in the global Governance, Risk and Compliance (GRC) markets”.

I count 12 subsidiaries - as indicated by readers already, this is a company with many moving parts.

Organic revenue growth is 3%; growth is 16% if you use “ongoing” results - I’m not a huge fan of this word. It sounds like it’s supposed to mean “underlying” but it’s certainly not underlying.

Checking the definition, I see that “ongoing” is defined as:

Ongoing - eliminating the effects of the impact of disposals, closures and businesses held for sale

Whereas organic is defined as:

Organic - Ongoing, eliminating acquisitions and exchange rate fluctuations

So “ongoing” eliminates the effects of disposals, but it doesn’t eliminate the effects of acquisitions. I’d certainly want to avoid the growth rates thrown up by such calculations.

“Ongoing adjusted PBT” is £11.4m, while actual unadjusted PBT is £5.2m. This strikes me as rather a large gap.

There are £5.8m of adjusting items:

Acquisition earn-outs £2m (I guess these must have been categorised by the accountants as a form of remuneration, being tied to the continued employment of the sellers of the acquired businesses?)

Transaction costs £1.3m

Office lease termination due to business disposals £1.4m

Amortisation of intangibles £1.1m

You can make what you will of this. Personally I would not allow all of these adjusting items, or I would at least mark the company down for suffering so many of them.

During the previous financial year, there were over £7m of adjusting items (mostly impairments). So my initial impression is that WIL’s accounts are not very clean.

CEO 's comment says that trading in the current financial year (FY June 2025) is in line with expectations.

"We have delivered another strong financial performance, particularly profitability and earnings. Our margin also continued to improve.

"We have also continued to execute on our strategy of replacing low growth and low margin businesses with scalable high growth, high margin businesses, which are enhancing the quality of the Group.

"We have a notably strong balance sheet which leaves us well placed to continue to invest across the business, in both organic and inorganic opportunities.

Net cash excluding leases is £31m. The balance sheet is mostly goodwill/intangibles but does still have a positive value when you exclude them.

Graham’s view

I’ll downgrade this to AMBER/GREEN as the complexity and the manner in which the company has presented these complex results make me nervous.

On the positive side, the balance sheet is fine and there is organic growth in recurring revenue of 6%, with most of WIL’s total revenues being recurring in nature.

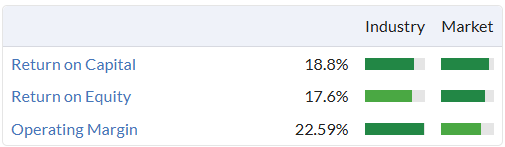

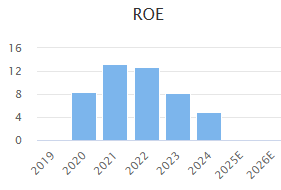

Quantitatively, it earns excellent returns for shareholders:

So I can see that there are some attractions. However, there are many subsidiaries to consider, and it’s rare to find businesses in the training/events space that turned out to be fabulous investments. So I think a moderately positive stance is fair.

At 15x earnings it’s not particularly cheap, and that is likely to be before the adjustments are accounted for. Actual reported earnings per share were only 2.88p in H1. I may need to downgrade this further to AMBER, the next time I look at it.

Roland's Section

Springfield Properties (LON:SPR)

Up 9.6% to 108p (£128m) - Interim Results & Land Sale - Roland - AMBER/GREEN

Springfield Properties is an AIM-listed small-cap housebuilder that operates in Scotland.

Today’s half-year results highlight a useful improvement in profitability, but are likely to be overshadowed by news of a £64m land sale to FTSE 100 peer Barratt Redrow.

This four-year deal will deliver a significant bump to current year profits and is expected to allow Springfield to eliminate its debt position while tightening its strategic focus on the North of Scotland.

Land sale agreement: Springfield has agreed to sell 2,480 plots of undeveloped land on six sites in Central Scotland to Barratt Redrow (whose results we reviewed last week).

Barratt will pay £64.2m for the land in stages over the next four years. As a result, Springfield expects its results for the current year (y/e 31 May) to be significantly ahead of market expectations.

The £64.2m price agreed with Barratt is uncannily similar to the £62.9m net debt figure reported in Springfield’s half-year results today. The company now says it expects to reach a cash position during its 26/27 financial year.

I’m not sure if it’s cause or consequence, but this land sale will drive a strategic shift that will see Springfield focus more heavily on the North of Scotland:

Following the Land Sale, the Group's strategic growth focus will be on opportunities in the North of Scotland where the Group is uniquely placed to capitalise on the substantial need for new housing to cater for the high population and economic growth expectations in the region. This is being driven by the UK Government-financed green infrastructure development in the North of Scotland.

Springfield specifically mentions power network upgrades and the Inverness and Cromarty Firth Green Freeport as drivers for new housing in the region.

Today’s half-year results indicate that the company had a land bank of 5,797 plots at the end of November, with a further 6,305 under contract.

This land sale was agreed after the half-year period ended, so it appears to represent a 43% reduction in Springfield’s owned land bank and a 20% reduction in its total land pipeline.

As a result, Springfield will become a smaller but more geographically-focused builder. Updated broker notes this morning suggest significant alterations to profit expectations for the next 2-3 years as a result.

Let’s take a look at the interim results for some broader context.

Half-year summary: during the six months to 30 November 2024, Springfield’s new home completions fell by 16% to 361. Management describes this as in line with expectations and reflecting market conditions.

Unsurprisingly, revenue was 13% lower at £105.6m, but the company’s gross margin improved by 3% to 17.7% and operating profit for the period rose by 27% to £6.1m. This was due to several factors:

Completion of legacy affordable housing contracts at the end of the prior yea;r

“Profitable” land sales;

“Sustained focus on cost control”.

However, the company’s normal working capital cycle saw net debt rise from £33.9m at May 24 to £62.9m at the end of November 24. This largely reflects adverse working capital movements of £23m.

This seasonal shift may not be an issue in itself, but one point worth noting is that Springfield’s debt is all contained in an overdraft facility that was originally due to expire in January 2025, before being extended to January 2026.

My feeling is that today’s land sale may have been driven as much by the need to reduce debt as by any strategic considerations. Perhaps refinancing was looking difficult?

Current Trading: the company says that the private housing reservation rate reduced from mid-December but is now improving “following interest rate cuts”.

The outlook is also improving for affordable housing:

Since the Scottish Budget in December 2024, affordable housing providers' confidence has improved and two new contracts have been signed that will commence in the current year

In addition to the Barratt deal announced today, the company is also having “non-binding discussions” regarding further potential sales to Barratt.

Estimates: the outlook in today’s results commentary is limited to an upgrade to current year guidance:

The Group expects to report profit for FY 2025 significantly ahead of market expectations

However, broker notes issued today make it clear that the corollary to today’s news is that profit expectations for future years have fallen.

With thanks to house broker Singer, we have the following updated earnings estimates. I’ve included the last two years’ actual results to provide some context:

FY23A: 10.4p per share

FY24A: 6.8p per share

FY25E: 12.7p per share (previously 8.0p)

FY26E: 8.6p per share (previously 10.0p)

FY27E: 9.1p per share (previously 11.0p)

Singer says these revised 26/27 estimates reflect “reduced scale, combined with a more cautious approach to the pace of recovery”.

Progressive and Equity Development (both paid research) have also both issued similar updated forecasts today. All of these notes are available on Research Tree, but investors without access might not immediately guess at the reduced expectations for FY26 and FY27.

Roland’s view

When we last covered Springfield in July 2024, Paul thought the business looked “attractive value” and went GREEN on the shares.

Is that still true after today’s news? The elimination of net debt is clearly positive, but it seems to be coming at a cost. Springfield is selling over 40% of its current owned land bank. This suggests to me that the company’s management may not have been confident that it could refinance and organically reduce debt to more sustainable levels.

Today’s balance sheet suggests a tangible net asset value of 129p per share. Even after this morning’s gains, the shares are still trading slightly below this level.

However, Springfield’s profitability has been relatively average in recent years, not necessarily justifying a significant premium to book value:

I think Springfield’s position looks more secure following today’s news, but this deleveraging seems to have come at a cost to medium-term earnings prospects.

The remaining discount to book value isn’t large enough to be a significant attraction, in my view, but I do think that broader market conditions are probably starting to improve.

On balance, I’m going to moderate our view to AMBER/GREEN.

Frp Advisory (LON:FRP)

Up 3% to 138.15p (£355m) - Q3 Trading Update - Roland (I hold) - GREEN

At the time of publication, Roland has a long position in FRP.

FRP Advisory Group plc, a leading national specialist business advisory firm, is pleased to announce a trading update for the nine months ended 31 January 2025 and declares its Q3 dividend.

FRP is a member of my rules-based SIF model portfolio here at Stockopedia. Today’s update is short, but makes for pleasant reading, with an upgrade to full-year guidance following a strong third quarter:

FRP is pleased with its performance in the year to date, with trading across each of the five service pillars currently ahead of the Board's expectations.

Management says that this demonstrates the company’s ability to support clients at different stages of the corporate cycle.

To put the strong Q3 in context, FRP reported organic revenue growth of 23% for the first half of its current financial year – Graham reviewed those results here, in December.

At the time, he noted that “Expectations for H2 are very modest so hopefully there is still a good chance of an earnings beat by year-end.” – that’s exactly what’s happened (my bold):

The Group's pipeline and activity levels remain strong, and as such the Board is confident that the Group will deliver results for the year ending 30 April 2025 ("FY 2025") ahead of current market expectations.

Dividend: An interim dividend of 0.95p per share has been declared (Q3 2024: 0.9p). FRP is unusual among UK stocks as it pays a quarterly dividend.

My sums suggest the shares offer a forecast yield of around 3.8%.

Estimates: the company’s broker, Cavendish, has provided updated forecasts today:

FY25E: EPS +2% to 10.8p (prev. 10.6p)

FY26E: EPS +5% to 11.8p (prev. 11.2p)

These numbers price FRP on FY25 forecast P/E of 13, falling to a P/E of 12 in FY26.

Roland’s view

This restructuring specialist has been a good news story for the AIM market since its flotation in March 2020:

The shares have benefited from a number of broker upgrades over the last 18 months, perhaps providing a good example of the trends Ed has highlighted in his recent articles on earnings upgrades:

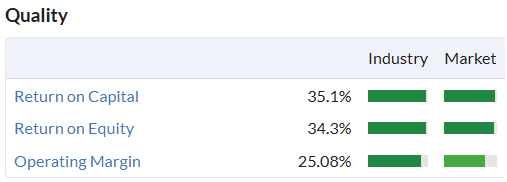

Today’s upgrade appears to provide further support for the growth story. Given the excellent quality metrics and net cash position of this business, the shares still don’t look expensive to me:

The main risk I can see is that this is an acquisitive, professional services business, where the main assets walk out the door every evening. History tells us that this kind of growth model sometimes comes unravelled, for example if financial discipline weakens, or if external conditions change unexpectedly.

I can’t rule out risks such as these in the future. But there doesn’t seem to be any cause for concern at the moment. Market conditions for restructuring specialists are also expected to remain favourable, due to the pressure on many businesses from higher costs.

I’m going to maintain our GREEN view on this stock, given the undemanding valuation and positive growth outlook.

See what our investor community has to say

Enjoying the free article? Unlock access to all subscriber comments and dive deeper into discussions from our experienced community of private investors. Don't miss out on valuable insights. Start your free trial today!

Start your free trialWe require a payment card to verify your account, but you can cancel anytime with a single click and won’t be charged.